The word “recession” has been everywhere lately. Headlines warn of an impending US recession, social media is abuzz with predictions of a market crash, and it’s hard not to feel a sense of unease.

But what does a recession really mean, and how can we prepare? After studying recessions in the US since the 1950s, here’s what we’ve learned.

What is recession?

While there is no official definition, recession generally refers to a period of decline in economic activity. Brief declines in the economy, however, are not necessarily considered a recession. Most analysts use two consecutive quarters of negative real GDP growth as a benchmark for a “technical recession”.

In fact, the July 2024 World Economic Outlook by the IMF projects that the US economy will grow by 2.6% in 2024, then moderate to 1.9% in 2025. In its June economic projections, the Fed forecasts US economic growth of 2.1% in 2024 and 2.0% in 2025. So according to some of the top economists in the world, the US’ economic growth is expected to moderate rather than going into a recession.

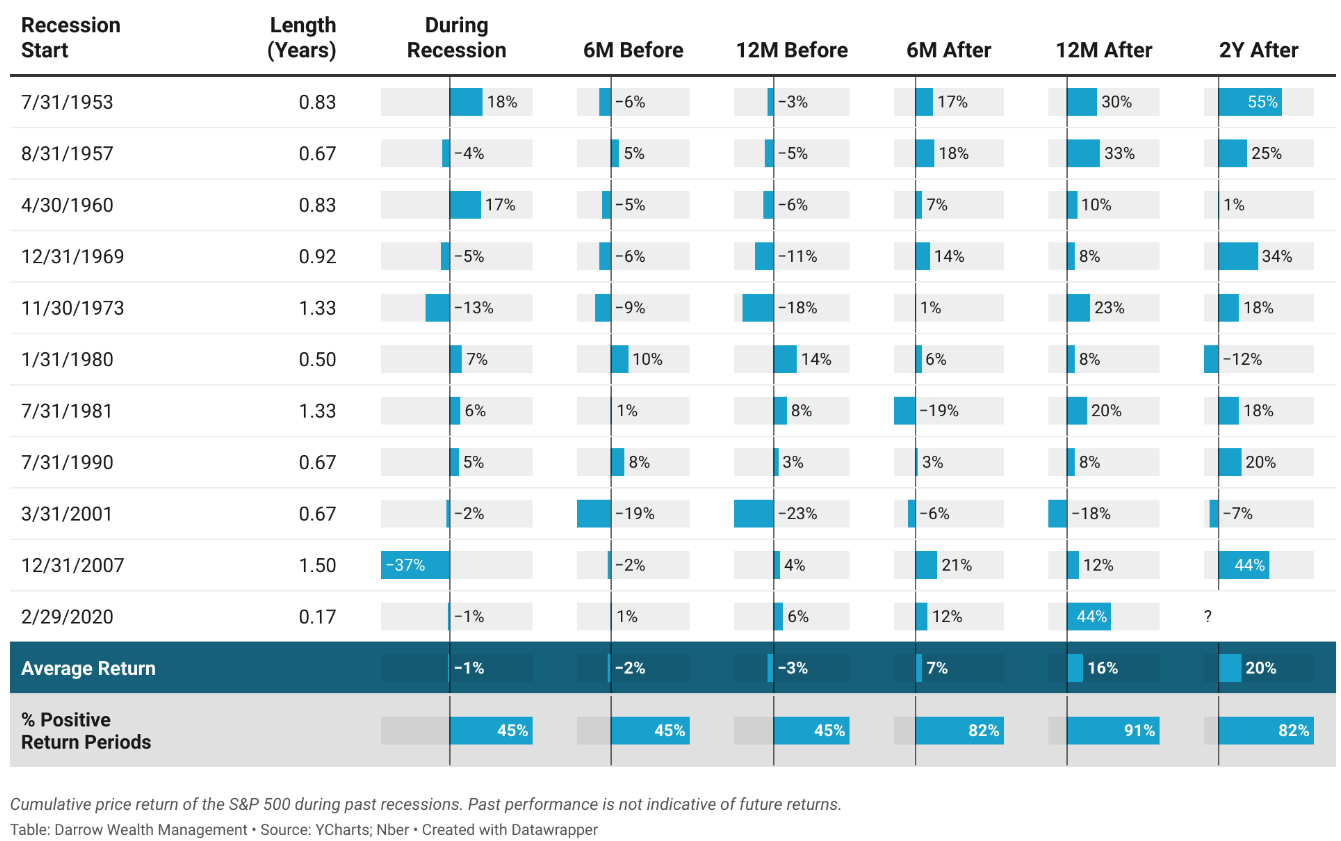

How the US stock market performed during economic recessions?

Source: Forbes, last updated 14 Apr 2022.

What if the economists are wrong about the US economy, and a recession does hit in the near term? Here are three key lessons we’ve learned from studying S&P 500 returns around recessions since the 1950s.

- Recessions tend to be short-lived. Based on the 11 recessions since the 1950s, the average duration is 10.3 months. The longest was the global financial crisis of 2007-2008, lasting 18 months. The shortest was the COVID-19 induced recession in 2020, lasting only 2 months

- It is difficult to predict market reactions to recessions. It’s hard to predict the exact timing of the next recession, and it’s even harder to forecast how the markets will respond. While you might assume that the S&P 500 would decline during recessions, that’s not always the case. In the last 11 recessions, the S&P 500 delivered positive returns in five instances and negative returns in the other six. It’s almost an even split. The average return during these 11 recessions was only -1%.

- Recessions often present buying opportunities. Counterintuitively, recessions have historically rewarded long-term investors and can create strong near-term buying opportunities. Based on the past 11 recessions since the 1950s, markets tend to stage a strong rally after, or even before, the recession officially ends. The average return of the S&P 500 six months, one year, and two years after a recession is +7%, +16%, and +20% respectively.

So how to prepare your investments for a recession?

While a near-term recession isn’t our base case scenario, and as we discussed earlier, it’s never wise to center your investment strategy solely around timing recessions, there are some good personal finance practices to enhance the resilience for your investment portfolio.

- Have enough emergency funds. It’s crucial to have enough emergency funds in place. Never invest all your savings in the stock market, even if it historically trends upward. Aim to keep at least 3-6 months’ worth of living expenses in a high-yield savings account. This serves as a safety net for unexpected events like job loss or medical emergencies.

- Review your goals and risk tolerance. If the idea of potential recession keeps you awake at night, probably it is time to review your goals and risk tolerance. Here’s a simple guideline:

Short-Term Goals: Prioritise stability. Allocate more to bonds and less to equities. This cushions your investments from short-term market volatility.

Long-Term Goals: Embrace growth potential. Allocate more to equities and less to bonds. Historically, equities have delivered higher returns over the long run, despite short-term fluctuations.

The key is to ensure your portfolio aligns with your needs. You don’t want to be forced to sell investments at a loss when you need the funds most.

- Stay invested, but diversify. Trying to time the market perfectly is nearly impossible. A more effective approach is to build a diversified portfolio and stay invested. Think about it: to beat a simple buy-and-hold strategy over the long run, you’d need to time your exits and re-entries to near perfection, and not just once, but multiple times. What are the odds of that?

Of course, nobody enjoys major market downturns. To protect yourself, consider diversifying a portion of your equity holdings into bonds. Bonds tend to perform well during economic downturns, as central banks typically cut interest rates.

Read More: