Investors may finally get their wish: interest rate cuts are on the horizon. Amid declining inflation and a softening labor market, the Federal Reserve(Fed) is prepared to lower its benchmark rate.

This marks a significant shift, as interest rates have a ripple effect across financial markets, impacting everything from bonds and stocks to currencies. We have examined the rating cutting cycles from the 1980s.While each cycle has its nuances, these historical examples offer valuable insights into potential market reactions as the Fed embarks on its latest easing path.

What’s on the market’s radar now?

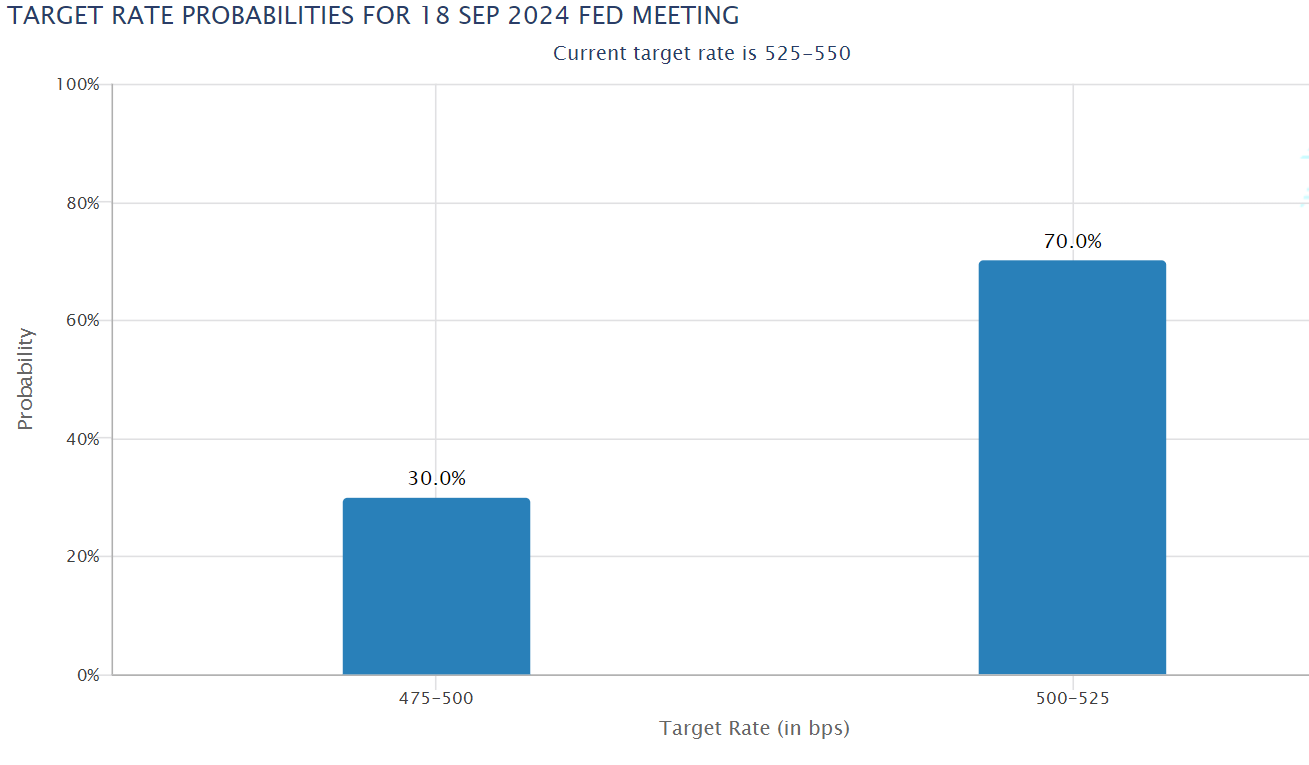

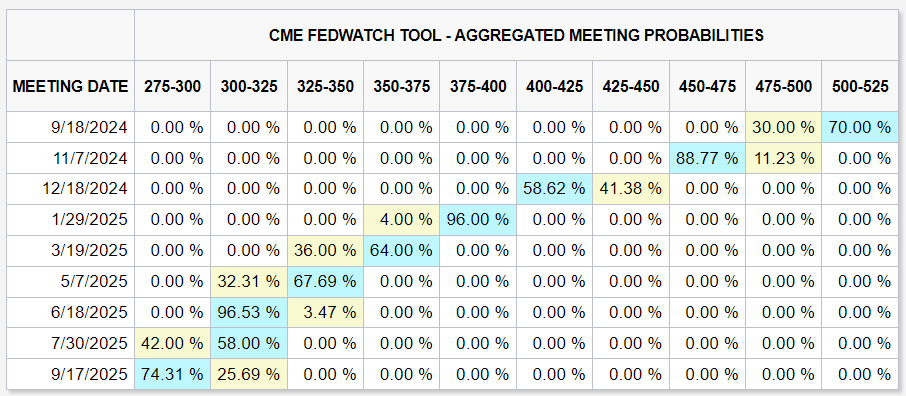

All eyes are on the Fed’s September meeting, where the rate cuts are expected to kick off. It’s no longer a question of when the Fed will cut rates, but rather how much.

According to the CME FedWatch tool, a 25 basis point cut seems to be the base case with a 70% probability, while there’s a 30% chance of a bolder 50 basis point cut in September.

While we can’t predict the exact move for September, the overall Fed rate trajectory is likely downward. Market expectations point to substantial cuts in the coming 12 months. By year-end 2024, the Fed funds rate is projected to reach 4.00% to 4.25%, a 125 bps(1.25%) decrease. By September 2025, it’s expected to fall even further to 2.75% to 3.00%, a 250 bps(2.5%) cuts from current levels.

What we learnt from past rate cutting cycles?

Studying the past rate cutting cycles, these are three key observations we have:

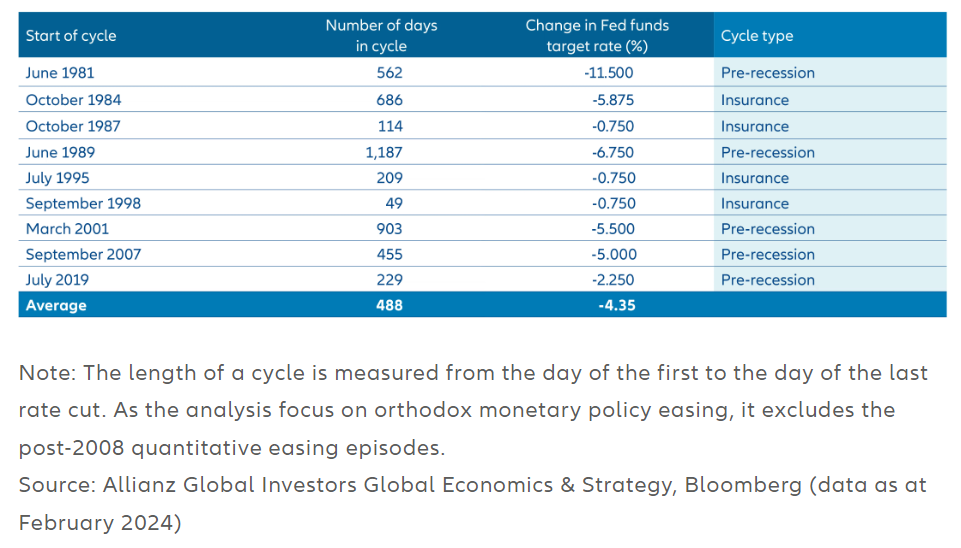

Past Fed rate cuts tended to be significant and last over a year

Looking back to 1981, we can identify nine distinct rate-cutting cycles. On average, these cycles spanned 16 months, with the Fed reducing rates by an average of 435 basis points (4.35%) over that duration.

Lessons for today: The Fed’s history of rate cuts highlights their dedication to economic stability. They’ve proven adaptable and data-driven in their approach. Past cycles also demonstrated the Fed’s readiness to act decisively, especially during crises. With ample room to cut rates now to support the economy, a prolonged recession seems less likely.

Furthermore, the Fed’s track record suggests they’ll maintain support until the economy is firmly on track. This may imply that rate cuts, once initiated, could continue for some time.

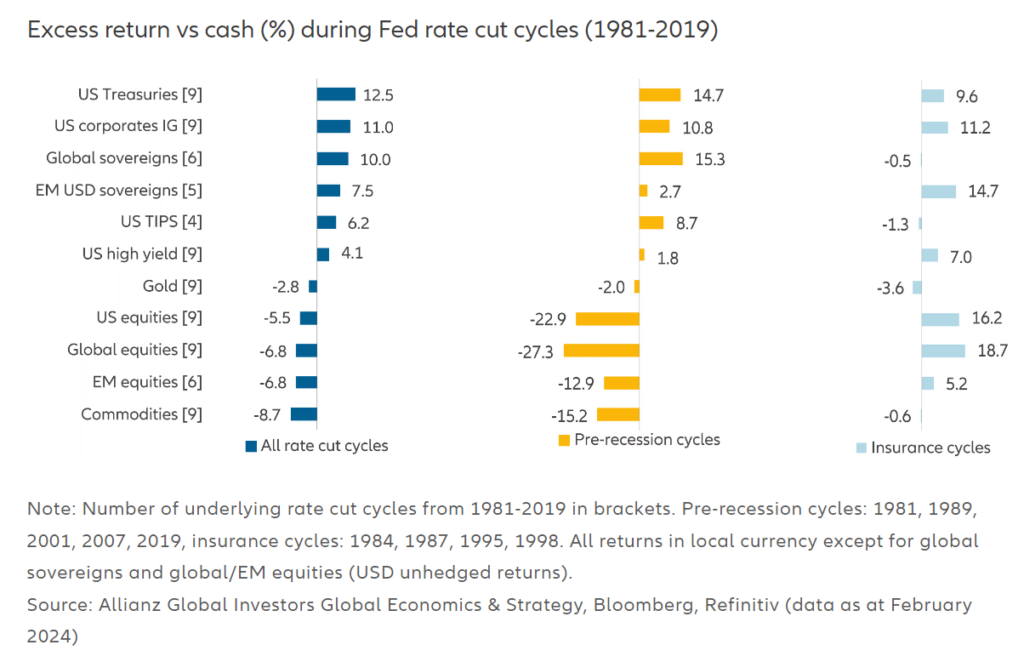

Equities delivered diverging performances

Historically, US equities performance has been mixed during rate-cutting cycles. The key factor determining overall success has been the Fed’s ability to prevent a recession. When a recession was avoided, US stocks gained an average of +16.2% excess return compared to cash during these cycles. However, if a recession did occur, US stocks experienced an average negative excess return of -22.9%.

Lessons for today: As discussed in the article “How to Prepare for a Recession”, predicting the exact timing and extent of rate cuts, or whether a recession will occur, is extremely challenging. Instead of trying to time the market, focus on building a diversified portfolio that can withstand different economic scenarios. For added buffer to your investment portfolio, consider diversifying some of your stock holdings into bonds or investments with lower volatility and downside protection.

High-grade bonds performed well across the rate cutting cycles

High-grade bonds, particularly US Treasuries and US investment-grade corporate bonds, have historically demonstrated strong performance during periods of rate cuts. For example, US investment-grade corporate bonds delivered an average return of +10.8% over cash during rate-cutting cycles that coincided with a recession, and +11.2% in cycles without a recession.

Lessons for today: In our H2 2024 Market Outlook, we highlighted the importance of locking in attractive bond yields before rates drop. The era of high yields on cash savings is nearing its end. Over $6 trillion remains parked in US money market funds. As the Fed begins cutting rates, we anticipate nearly 50% of these funds will be reallocated, primarily into bonds.

In summary

Past performance doesn’t guarantee future results, but understanding historical trends can guide us in making more informed investment decisions. Equity markets may still have room to perform in the months ahead if the Fed successfully engineers a soft landing. That said, any softer-than-expected economic data may lead to higher volatility in equities. Additionally, investors may want to build a diversified portfolio by investing in bonds. The time has come for investors to capture attractive yields in bonds while they are still available.

Read more

How to Prepare for a Recession?

Syfe H2 2024 Market Outlook: When Monetary Inflection Meets Election