What Happened?

In its final FOMC meeting of 2024, the Fed delivered a widely expected 25 basis point cut to its benchmark interest rate. This brings the total interest rate cuts to 100 basis points for the year.

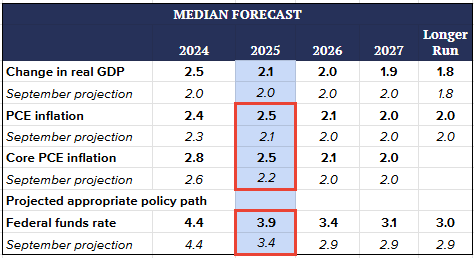

However, what stood out to us was the committee’s acknowledgment of the economy’s surprising resilience and the potential impact of policies from the Trump administration, such as tax cuts and tariffs. In response, they raised their inflation forecast for 2025 from 2.1% to 2.5%.

What’s also notable is the adjustment to their rate-cut guidance. The Fed now expects the federal funds rate to end 2025 at 3.9%, up 50 basis points from their September projection of 3.4%. This means the Fed scaled back the number of rate cuts planned for 2025 to two, down from four initially projected.

The Immediate Market Reaction

Markets interpreted this move as a “hawkish cut”, leading to a broad-based negative reaction. A sell-off swept across asset classes, including equities, bonds, gold, and Bitcoin. The S&P 500 declined by -3.0%, while the Nasdaq 100 fell by -3.6% overnight. Treasury yields also moved higher across the curve, with the US 10-year yield surpassing 4.5%.

S&P 500 Index

US 10-Year Treasury Yield

What’s Our Take?

- The Fed put is still in place

While the Fed may slow the pace of rate cuts, it remains unlikely to reverse course and raise interest rates. In fact, Fed Chair Powell’s speech struck us as less hawkish than the market seemed to interpret.

Addressing inflation, Powell reiterated during the press conference that he still views the disinflationary trend as intact, citing cooling housing inflation and a gradually softening labor market. The projection of slower rate cuts appears to reflect caution around potential policy uncertainties under the incoming administration.

A key takeaway from 2024 is that the Fed has demonstrated its ability to react boldly and quickly to changing economic conditions, as evidenced by its actions in Q4 2024. For this reason, we don’t interpret this development as a pivot in the Fed’s overall policy direction.

- The equity dip seems more attributable to technical selling pressure

Putting the overnight selloff into perspective, the S&P 500 has rallied +6%, and the Nasdaq 100 has gained +10% in just a month and a half since the end of October, reflecting post-election optimism. It seems that some investors took this opportunity to lock in profits.

- For your investment portfolio: stay invested and add diversifiers

Looking ahead to next year, while the Fed has adopted a slightly more cautious stance on rate cuts, the overall policy direction remains accommodative, which could continue to support asset prices.

For US equities, we believe the risks are fairly balanced. On the upside, potential tax cuts and deregulation may bolster already strong earnings growth. On the downside, the possibility of trade wars could dampen positive sentiment. Additionally, high valuations and relatively crowded positioning in US equities pose a risk of sudden selloffs.

In such a market environment, it is essential to stay invested while also adding diversifiers to your portfolio.

Portfolio to Consider: Syfe Income+

For bonds, we maintain a positive outlook, supported by the attractive yields currently available. Historically, the entry yield is a key driver of bonds’ long-term returns, and with the recent sell-off, yields have reached even more compelling levels. This creates an attractive entry point for income-focused investors seeking steady returns. As mentioned above, given the near-term volatility, it’s best to approach this positive view on bonds through globally diversified, actively managed bond portfolios. This strategy allows investors to capture attractive yields while navigating market fluctuations effectively.

Learn more about the Income+ Portfolio here