The coronavirus pandemic can be remembered for many things, one for being the speediest stock market recovery in history. If you had bought a S&P 500 index fund at the bottom of COVID-19 crash, you would have made approximately 130% of your invested amount.

Fast forward to this date, both S&P 500 and the tech-heavy Nasdaq have been consistently hitting all-time highs. For instance, S&P 500 and Nasdaq had recently done so, hitting above 5,300 and 19,000 respectively to mark another all-time high on 5 June.

From a valuation standpoint, stocks appear expensive. As of the end of May 2024, the S&P 500’s latest 12-month P/E ratio was at 24.7X, dating back to just the end of last year and an 11.5% increase from the previous year. This might have left many wondering if it’s now too late to get in the game of investing.

It doesn’t matter that the market is at an “all-time high”

If investors are supposed to “buy low, sell high”, then the current environment is a terrible time to invest, right? Absolutely not!

Waiting for the market to correct again results in missed opportunities. Think about it this way. The S&P 500, the benchmark for US stocks, notched 20 new all-time highs in 2019. In 2018, there were 18 all-time highs. And in 2017, there were a record 62 all-time highs achieved.

If you had decided not to invest when the market was at an all-time high during these years, you would likely have missed the subsequent highs that occurred. Of course, the market has stretches of positive and negative performance, but historically, the market goes up over the long term.

While everybody prefers to buy at market lows, timing the market is incredibly hard. Even professionals fail to get it right. What’s more important is time in the market, being invested early on so that you don’t miss out on the new highs that will inevitably follow.

But what if I invest right before the market crashes?

The fear that the market could crash immediately after you’ve invested is a valid concern that frequently holds investors back. After all, the market cannot keep going up indefinitely. With the ongoing tensions around the world and mixed economic data, investors would be more skeptical about the outcome of the market.

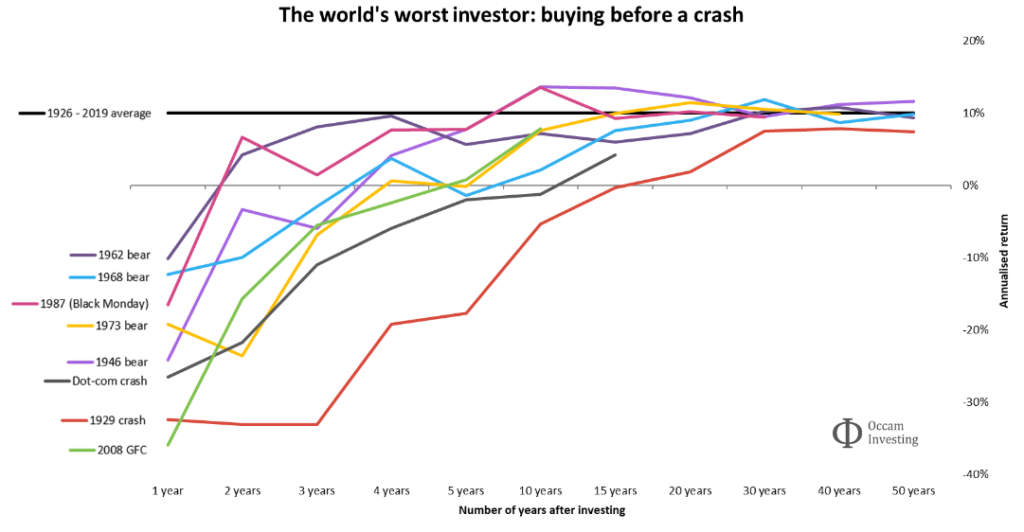

Here’s the truth: if you do happen to invest just before a market crash, your short-term returns will be affected. There’s no avoiding it. But the longer you stay invested, the more likely that your eventual returns will be closer to the long-term average. In the words of Kenneth Fisher, “Time in the market beats timing the market”.

As the chart above shows, even if you were to invest just before these major crashes occurred, your returns prospect improves the longer you stay invested. After about 15 to 20 years, your returns tend to converge on the long-term average return of about 10% annually. If you are planning for a long term financial goal such as retirement, investing just before a crash is still better than not investing at all.

Let’s say for instance, you’ve invested into the market right before the most recent market crash, during the COVID-19 pandemic. It would have only taken approximately half a year for the market to recover and for you to level your losses. And if you continue to stay in the market, the returns to this date would be skyrocketing. Sure, it might not have been as remarkable as a 130% increase, but there is still no doubt that you would have profited tremendously from your actions.

The key is to not panic and stay invested. Of course, that’s easier said than done when you see the market falling 34% in less than a month, as it did from February 19 to March 23 on 2019. This is also why it’s so important to invest according to your risk tolerance i.e. the degree to which you can stomach losses when your investments perform poorly.

The best strategy to follow

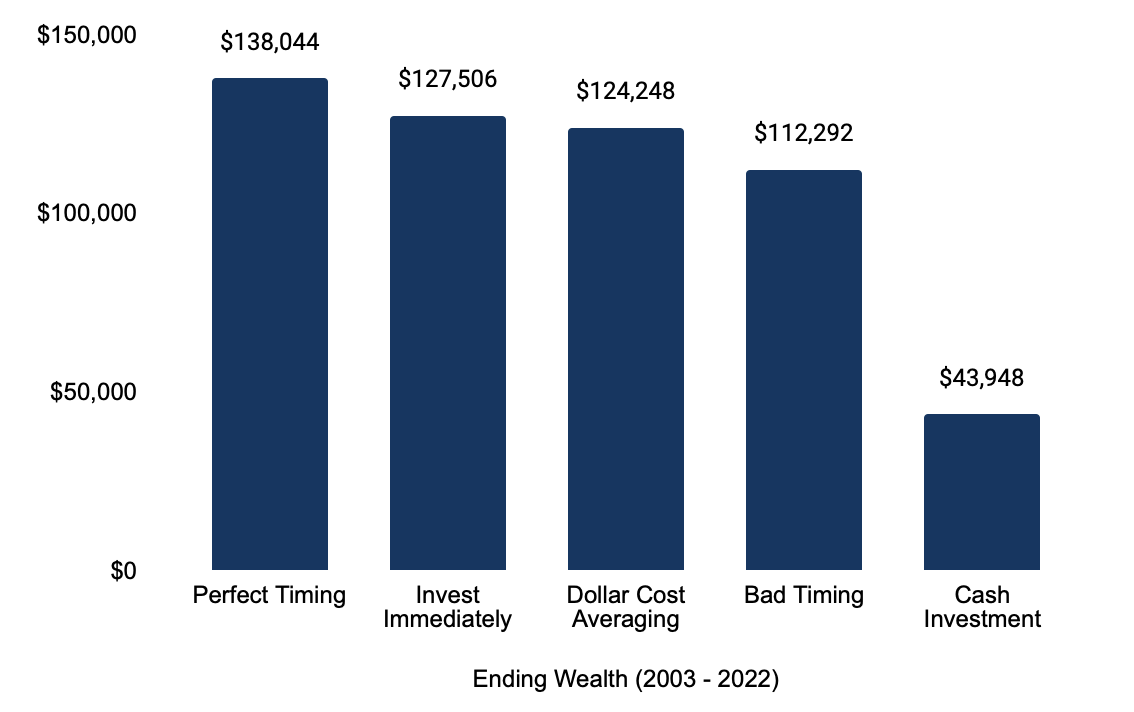

Given the upward trend of the market over time, it makes sense to simply enter the market and stay invested, instead of worrying whether the market is at a high or low point. A study from Charles Schwab highlights this best. It found that procrastination can be worse than bad timing itself.

The study looked at five fictional characters, each investing $2,000 annually from 2003-2022 in a portfolio that tracks the S&P 500 index. As such, the capital would be equal amongst these characters, but what differs would be the timing and strategy of the investment.

- Peter Perfect timed his investments perfectly, always investing when the markets hit their lowest point.

- Ashley Action didn’t time anything. As soon as she received her $2,000, she would invest it immediately.

- Matthew Monthly used a dollar-cost averaging strategy. He invested his $2,000 across 12 months, putting his money to work at the beginning of every month.

- Rosie Rotten had terrible luck. She ended up always investing her $2,000 at market all-time highs.

- Larry Linger kept waiting for the perfect moment to invest. Because he always thought a better opportunity would come up, he ended up not investing in stocks at all.

Why you should invest as soon as you can

The results are surprising. Ashley Action invested immediately and did not try to time the market at all. But her performance was comparable to Peter Perfect’s. She ended up with only $10,538 less, even though Peter Perfect was able to invest at all the very best moments.

Even Bad Market Timing Trumps Inertia

(Each investing $2,000 annually from 2003-2022 in a portfolio that tracks the S&P 500 index)

You would expect Rosie Rotten to fare the worst given that she had such bad marketing timing. Surprisingly not. She ended up with slightly less money than dollar cost averaging Matthew, and significantly more money than Larry Linger, who didn’t invest in stocks but instead bought US Treasury Bills.

The takeaway from this is to invest at the earliest possible moment, no matter what level the market is at. Nobody, not even professional wealth managers, can consistently identify market bottoms. And even if you do somehow get the timing right on a regular basis, the study shows that you won’t be much better off than someone who puts her money to work right away, regardless of market highs or lows.

If you are still uncomfortable with the thought of investing a large amount of money when the market is peaking, consider dollar cost averaging. It is a better strategy than market timing, and it ensures that you don’t end up like Larry Linger. Ready to start investing? Achieve your wealth goals with Syfe’s expertly managed, low-cost portfolios.

This article was first published as a guest post by Syfe on Guidesify. Updated on 11 June 2024.

This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone.Past returns are not a guarantee for future performance. Investors should consider his/her own circumstances. The information or advertisement contained herein does not constitute an offer, any solicitation, invitation or recommendation to engage in any investment activities.