The US inflation rate in December unexpectedly climbed to 3.4%, surpassing the forecasted 3.2%. This development is crucial for investors and policymakers, signifying a complex path ahead for the Federal Reserve’s monetary policy.

On Top of Our Mind Last Week: US Inflation Rise in December – A Deeper Analysis

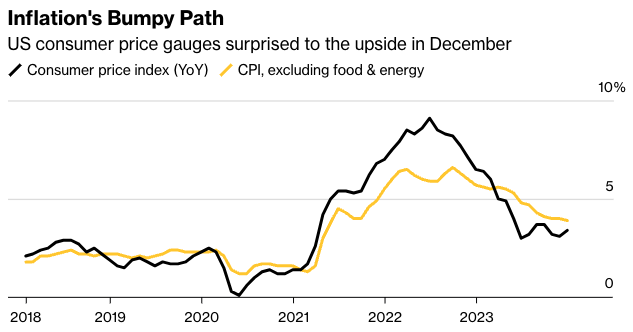

Source: Bloomberg

Data Details:

December’s inflation rate came in at 3.4%, exceeding economists’ expectations of 3.2%, a significant jump from November’s 3.1%. This rise was driven by a confluence of factors, with housing costs and energy prices leading the charge. Housing costs contributed to over half of the price increase. Additionally, energy costs, primarily driven by electricity and gasoline, along with rising food prices, played a significant role in this increase.

However, the core CPI, which excludes volatile food and energy costs, continued its downward trend to 3.9% in December, from 4% in November. This was the lowest reading since May 2021. The decline in core inflation suggests that the prices of goods and services outside of food and energy are rising at a slower rate.

Despite the uptick in headline inflation in December, most market participants looked past this data point, instead betting on the Fed to begin cutting interest rates. Futures markets indicate that there is an 81% probability of a rate cut at the March FOMC meeting.

Why should we care:

The divergence between the headline and core inflations highlights the complex economic currents. While a gradual moderation in inflation is expected, external factors like geopolitical tensions could influence the economic landscape.

The Fed’s next moves, particularly regarding interest rates and monetary policy, will be critical in shaping both the US and global economic outlooks in 2024. In the short term, market anticipation of rate cuts as early as March 2024 will be key to monitor.

Market Recap Last Week

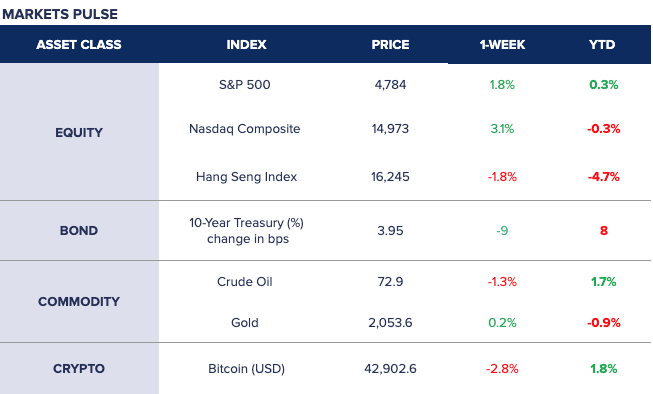

In the second week of 2024, the US stock market rebounded with the S&P 500 and Nasdaq Composite climbing 1.8% and 3.1%, respectively. Meanwhile, the Hang Seng Index in Hong Kong extended its decline, dropping by 1.8%. In the bond market, the yield on 10-year U.S. Treasury bonds fell by 9 bps, reflecting investor uncertainty amid rising inflation. The commodities market saw mixed movements: crude oil prices decreased by 1.3%, while gold marginally increased by 0.2%. In the realm of cryptocurrencies, Bitcoin experienced a 2.8% decline, pulling back after the Bitcoin ETFs were launched.

Source: Google Finance, Syfe Research, 13 January 2024

What is on the Radar for This Week?

In the upcoming week, investors will keenly await China’s fourth-quarter GDP YoY data, scheduled for release on Tuesday. This report is anticipated to show a 5.2% growth, largely due to a lower base from the previous year. Additionally, attention will turn to the US as the Initial Jobless Claims are released on Wednesday.

Source: Yahoo Finance, Bloomberg, Google Finance, The Business Times, Financial Times