This week’s Federal Reserve meeting marks a significant shift in the US monetary policy, indicating an end to the aggressive rate hike cycle and forecasting lower borrowing costs by 2024. This pivotal change, acknowledging subdued inflation, is crucial for investors as it signals a shift from a rising rate environment to potentially easing rates, impacting various investment strategies.

On Top of Our Mind This Week: Navigating a New Investment Landscape: Implications of the FOMC Meeting

Source: Bloomberg

Event Details:

The Federal Reserve’s recent meeting marks a pivotal shift in U.S. monetary policy, a nuanced transition from a period of rigorous rate hikes to a potential easing phase. This significant development reflects the Fed’s response to evolving economic conditions, particularly in relation to inflation and economic growth.

During the meeting, the Fed’s decision to maintain interest rates steady reflects an anticipation of lower borrowing costs by 2024, a notable departure from its recent aggressive rate-hiking stance. The median forecast among Fed officials suggests a possible reduction of three-quarters of a percentage point from the current rate range of 5.25 to 5.50 percent by the end of 2024. This suggests that, contrary to the previous trend, further rate hikes may not be necessary.

Fed Chair Jerome Powell’s comments at the press conference post-meeting emphasized this shift. He acknowledged the unpredictable nature of the economy and expressed the Fed’s openness to resuming rate hikes if needed, while also indicating a leaning towards a lower policy rate. The market’s positive response to this announcement, with a rise in stocks and a fall in Treasury yields, underscores the significance of the Fed’s revised stance.

Why should we care:

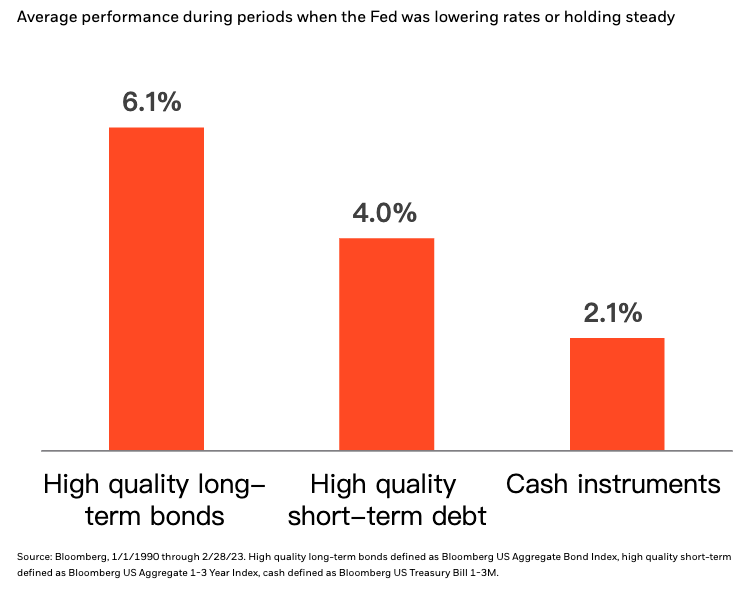

Source: Bloomberg

Investors traditionally favouring cash or money market funds should note this transition. Historical data indicates that, after peak rate hikes, returns from cash significantly lag behind those from investment-grade corporate bonds. With rate cuts likely on the horizon, bonds, particularly longer-dated ones, are poised to offer more attractive returns as lower interest rates typically increase the value of fixed-rate bonds, while returns on cash align with declining central bank base rates.

This environment presents a critical opportunity for investors to reconsider asset allocation. Shifting from cash-centric strategies to a balanced approach that includes bonds can capitalise on the anticipated market dynamics.

In summary, the Fed’s pivot from a rate-hiking stance to a potential easing phase marks a significant turning point for investment strategies. The shift towards bonds over cash or money market funds could be a strategic move for investors navigating this new landscape, balancing the need for safety with the potential for higher returns.

Market Recap This Week

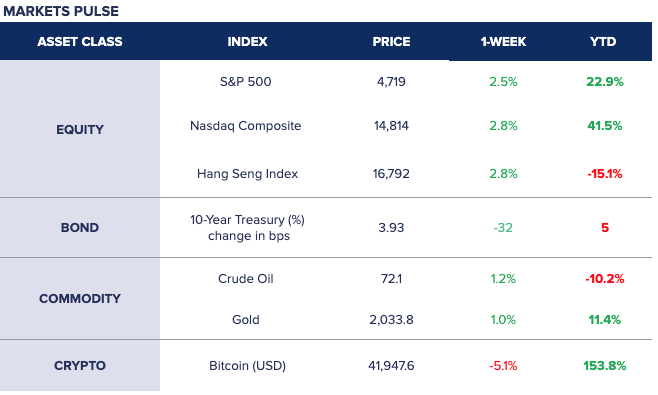

This week in the financial markets, buoyed by the Federal Reserve’s proactive monetary policy, the U.S. equity market witnessed a notable uptick. The S&P 500 and the Nasdaq Composite Index each saw appreciable gains, rising by 2.5% and 2.8% respectively. In Asia, Hong Kong’s Hang Seng Index reversed its downward trend, climbing by 2.8%. In the bond market, the 10-year Treasury yields declined to 3.93% from 4.25%. The commodities market also showed signs of stabilization, with crude oil and gold experiencing modest increases of 1.2% and 1.0%, respectively. However, Bitcoin bucked the trend, recording a decline of 5.1%, underscoring the volatility in the cryptocurrency market.

Source: Google Finance, Syfe Research, 16 December 2023

What is on the Radar for This Week?

Next week, financial markets are poised to closely monitor two key economic releases. On Tuesday, the Eurozone is set to announce its CPI Year-over-Year. Analysts forecast a figure of 2.4%, marking a 0.5% decrease compared to the previous year. This inflation data holds significant importance for the Central Bank, as it plays a crucial role in maintaining price stability. Additionally, on Wednesday, the United States will release its GDP Quarter-over-Quarter data, with expectations pointing to a robust 5.2% growth, substantially higher than the previous quarter’s 2.1% increase. These releases are critical indicators of economic health and will be closely scrutinised by investors and policymakers alike.

Source: Yahoo Finance, Bloomberg, Google Finance, The Business Times, Financial Times