Topic #1: Sticky Inflation in the US & UK

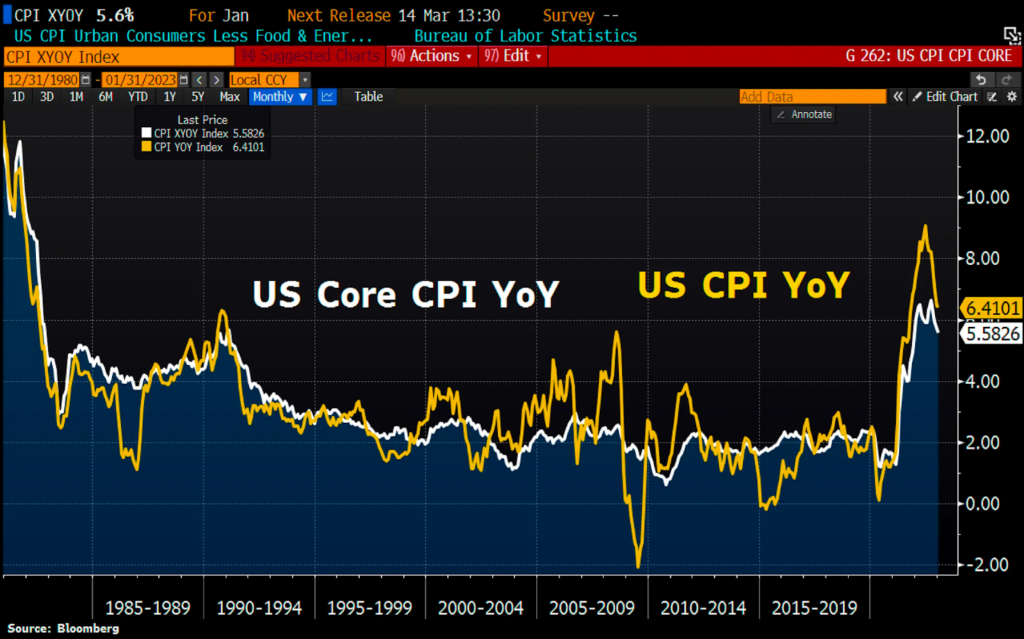

Latest US inflation data out on Tuesday has disappointed investors, as prices continued to rise in January by 6.4% annually. This marked the seventh consecutive month of price increases, with only a slight cooling from December’s 6.5% pace. The “core” measure of inflation, which excludes more volatile items such as food and energy, was also higher than expected, but slightly cooler than the month before at 5.6%. While certain items such as used cars, medical care, and airfares saw price decreases, essential items like energy, food, and shelter kept inflation elevated.

Has the US shown inflation the door?

As discussed in last week’s market wrap, the wildcard impact of China’s reopening and expected spending and growth boom could escalate inflation. The drop-off in the inflation of goods has hit a wall, which means any serious further dip in inflation will likely have to be driven by services. This will also be a challenge since Americans’s wages are rising and have shifted spending to services recently, pushing prices upward.

Why should I care?

The Federal Reserve has been raising interest rates for nearly a year to try to reestablish price stability in the economy, but with inflation cooling slowly, the Fed may have to hike rates higher and keep them higher for longer to bring inflation back towards its long-term 2% target. The persistently sticky and high inflation could further weigh on risky assets, such as stocks.

What about the UK?

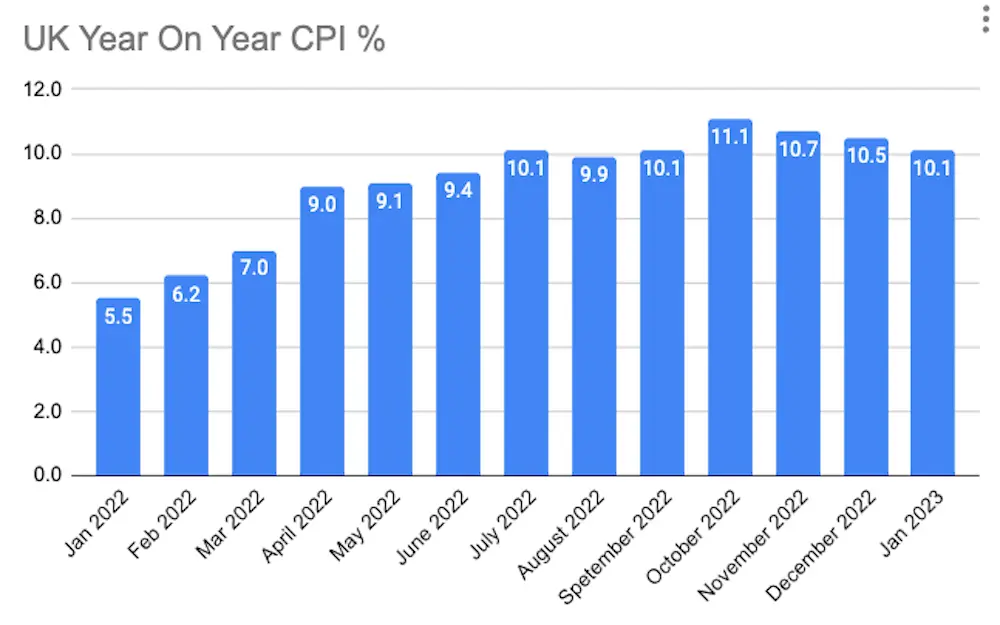

In January, UK inflation experienced a continued decline, with a 10.1% increase in overall prices compared to the same period the previous year, and a 5.3% increase on the “core” rate, which excludes more erratic food, energy, tobacco, and alcohol prices. The Bank has been increasing interest rates to control inflation and predicts that prices will increase by approximately 4% by year-end. This better-than-expected data supports the Bank of England’s projection that inflation will sharply decrease this year, and makes their projection seem less unrealistic.

Topic #2: Airbnb Had Its First Profitable Year

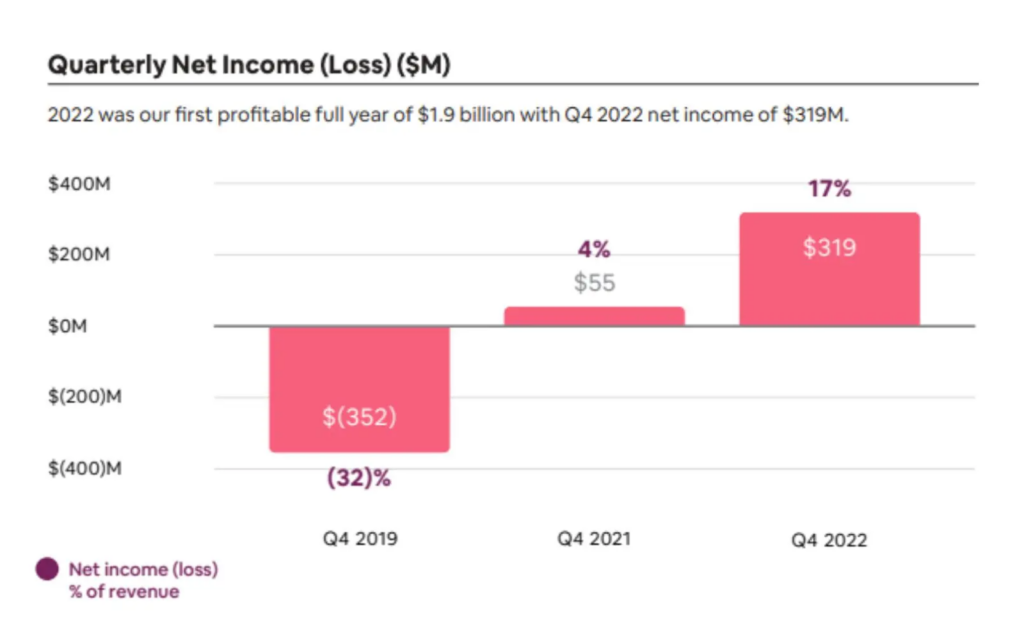

Airbnb reported impressive results, exceeding revenue and profit expectations in the last quarter and making 2022 its first full year of profitability. Despite high-flying airline prices and widespread economic turmoil, cross-border trips surged 49%, with China’s loosening Covid restrictions making travel from the Asia-Pacific region the real grower. Pandemic trends even went into reverse, with people opting for shorter stays in bustling cities, making city breaks account for half of all bookings last quarter, the first time that’s happened since the pandemic hit.

The bigger picture:

The company plans to invest in products beyond its main accommodation services again, giving renewed attention to offerings like “experiences”, including guided local excursions for travelers. With demand resilient so far this year, and travelers increasingly booking ahead, Airbnb gave an upbeat outlook that got investors bumping shares up 12%.

Airbnb’s decision to expand beyond its main accommodation services and invest in offerings such as “experiences” could be a smart move, especially in light of recent trends in the travel industry. For instance, travel firm Tripadvisor reported that consumers have been redirecting their spending from goods to activities, which has boosted tour bookings and helped the company exceed revenue expectations in the last quarter. If Airbnb can tap into this trend, it could see success in its efforts to diversify its offerings and attract more customers.

Topic #3: HK banking system aggregate balance 2 year low

HKMA had bought HK$4.223 billion ($538 million) from the market last Monday (13 Feb) to stop the local currency from breaking its weak end peg to the U.S. dollar. The Hong Kong dollar is pegged to a tight band of between 7.75 and 7.85 versus the U.S. dollar. The HK banking system aggregate balance – the key gauge of cash balances in the banking system – will decrease to HK$91.864 billion on Feb. 15.

Shorting HKD is a crowded trade among hedge funds. In this strategy, hedge funds borrow money in the lower interest rate HKD and then invest that money in the higher interest rate USD. The idea is that the hedge fund will earn the difference between the interest rates, and the HKD-USD exchange rate remains pegged.

Three-monthHong Kong interbank offer rates (Hibor) fell to 3.42958% on lsat Monday from a peak of 5.4% in December, representing a discount of about 140 basis point below equivalent tenor three month U.S. Libor, the widest discount in 16 years.

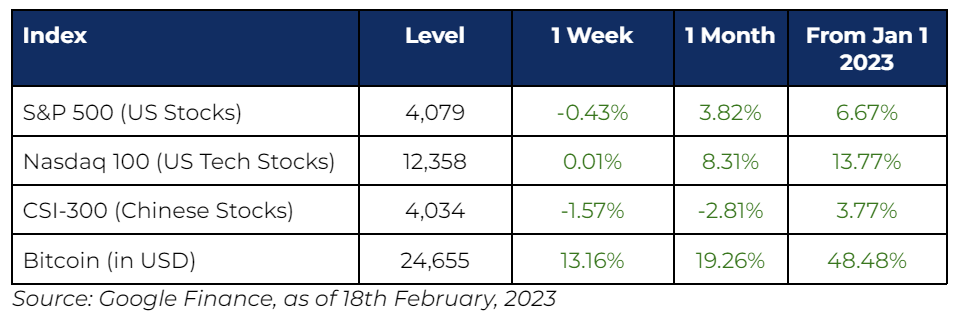

Top Earnings at a Glance: