Peak Inflation?

Markets rallied on Friday, S&P 500 gained 3%, ending the week almost 7% higher as recessionary fears receded slightly. Even with the gains, the S&P 500 is still down 18% year to date.

Three catalyst drivers last week: first, a drop in inflation expectations; second, a weaker economic outlook; and third, the Fed not fully withdrawing the printed liquidity.

CME rate futures implied a 25% chance of a 75bp rate hike in September. The Fed’s five-year breakeven inflation fell from June 15’s 3% to Jun 24’s 2.8%.

The latest consumer inflation expectations came in lower, settling lower than the 14-year high. The survey, from the University of Michigan, said consumers expect the prices to rise by an average of 3.1 percent over the next five to 10 years. Inflation expectations are generally used to gauge consumer behaviour – rising inflation may make consumers think that prices could be higher in the future, so they will front-load their consumption and demand higher wages, thereby contributing to even higher inflation rates.

Federal Reserve Bank of St. Louis President James Bullard said fears of a recession are overblown, while Chair Powell acknowledged that it is proving to be increasingly challenging to engineer a soft landing.

Soft-ish Landing?

Q2 US GDP is expected to remain flat. May retail sales data was negative, the ISM manufacturing and services indexes both fell, and consumer confidence fell. All these slowdown persuaded the market to believe that the Fed has been effective in cooling the economy down.

Powell indicated in the Senate that Fed targets to remove 2.5-3 T within next two years, which is around ~50% of the printed liquidity during covid.

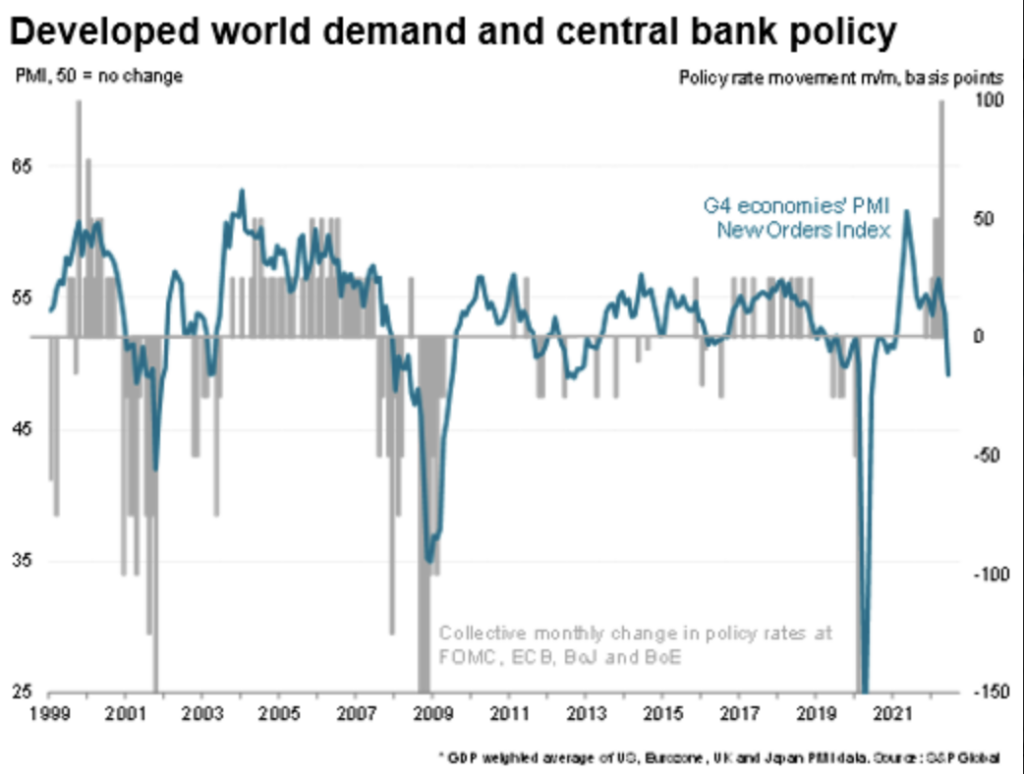

PMI readings from developed nations showed that new orders declined for manufacturing. This fall could be driven by higher interest rates, energy insecurity, Chinese lockdowns and Russia’s invasion of Ukraine.

Analysts at UBS looked at US recessions in the last 100 years and categorised them as shallow (US GDP fell by 3% of less) or deep recessions (US GDP fell by more than 3%). Shallow recessions were often associated with central banks raising interest rates – a situation we’re currently facing.

Data shows that in a shallow recession, markets fall by about 11% on average and bottom out about 4 months after the start. In a deeper recession, markets tend to fall about 24% and bottom out about nine months from the start.

Given that the labour market remains robust, even if the US economy were to head into a recession, evidence suggests that it could be a shallow one.

Bulls in China

The Chinese equity market fared well too, with internet companies, represented by Kraneshares CSO China Internet ETF (KWEB) leading the charge and gaining 4% over the week. Since March, when many of these stocks bottomed, Pinduoduo shares have more than doubled, while Meituan is up 80%, followed by JD.com and Kuaishou that are up close to 50%.

The shopping festival 6.18, hosted by JD.com saw slower growth but highlighted new consumer behaviour (live streams, greater interest in household appliances and outdoor gear). Despite slower growth, sales volumes were still 10% higher. Kuaishou announced that GMV of branded merchants was up 515% YoY during 5.20-6.19 promotion. Douyin indicated strong sales with order volume up over 80% YoY during 6.1-6.18 promotion.

Despite the recent strength among these platform companies, we see founders are taking contrarian views. Liu Qiangdong, JD founder, has sold down around US$ 1b in JD and JD Health in the past month; Wang Xing, Meituan Founder, also sold HK$ 25m shares in a week. Meanwhile, Nasper, the largest shareholder of Tencent in the past, has informed the market that they will gradually sell down their Tencent Holdings on the market, capped by a 5% daily volume.

Electric vehicle sector got a boost from a State Council meeting chaired by Premier Li Keqiang, who reiterated support for the sector and extension of tax breaks for new electric vehicles.

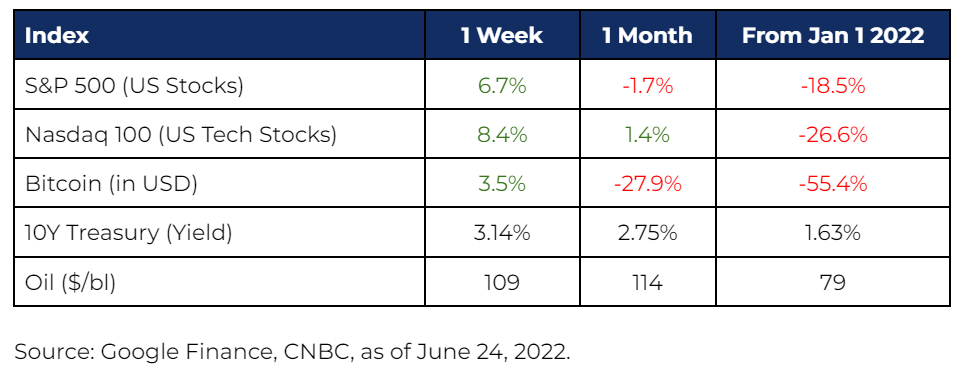

Market Stats