U.S. GDP Turnaround Tempers Recession Fears

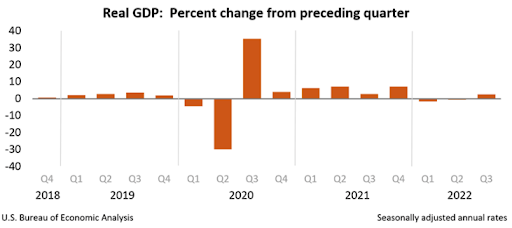

After entering a mild technical recession in the first two quarters of the year, real GDP increased at an annual rate of 2.6% in the third quarter, beating analysts’ estimates by 0.3%.

A narrowing trade deficit owing to increased oil exports combined with increased consumer and government spending were the major drivers of the growth. However, consumer spending is decelerating and the dollar is gaining strength as interest rates climb, which does not bode well for domestic demand and exports, respectively. Analysts do not expect this growth to sustain, and forecast a mild recession in the first half of 2023.

Reopening China

Grow Investment Hao Hong tweeted a post on the Reopening Committee. So rumor has it that Politburo Standing Member Wang Huning is leading the committee and targets the open by 2023-March. After the 20th National Congress of the Chinese Communist Party, the government still implementing a dynamic zero policy. It disappointed the market, especially the Hong Kong market on concerns of a sloppy China economic growth, and crashed CNY. Hang Seng Index ended -14.72% in October.

Sunak Calms Markets, For Now

The appointment of the former Chancellor of the Exchequer, Rishi Sunak, as Prime Minister of the UK, has temporarily calmed markets that were thrown into turmoil by his predecessor. The Pound was up 2.7% as of Friday while the 10-Year Gilt Yields fell by over 0.5% in the same week.

However, his appointment has bought nothing but time for him and his Chancellor, Jeremy Hunt, to come up with an ironclad recovery plan to shore up investor confidence. Skyrocketing inflation and rising interest rates have eroded public finances, forcing Sunak and Hunt to consider a cut in government spending. Unfortunately, the UK is also facing its biggest cost-of-living crisis in 30 years, meaning that austerity could prove to be politically detrimental.

Growth is now clearly a secondary objective for the new government. Hunt quickly reversed the £32 billion in unfunded tax cuts, but there is still a £30-40 billion hole in public finances that needs to be filled.

U.S. Indices Post Solid Gains for Second Consecutive Week

The S&P500, the Dow Jones Industrial, and the Nasdaq 500 rose 4.7%, 4.9%, and 5.2% last week, respectively, posting strong gains for the second consecutive week, and making it their best week since June.

The indices rallied on the news of the U.S. positive third quarter GDP growth, as well as a fall in the 10-Year Treasury Yield. The 10-Year Yield briefly crossed 4.30% before settling at 4.00% by the end of Friday, which ended 12 straight weeks of increases.

This year’s tech beatdown continued into earnings week, with Big Tech in particular declining by, on average, 9% on the day they announced earnings. Snap fell 28% after reporting a quarterly revenue figure that fell short of expectations. Apple, however, remained surefooted in comparison to its peers, beating EPS and revenue forecasts. Its shares traded higher post-earnings, but CEO Tim Cook attributed the absence of double-digit growth to the strengthening dollar and supply constraints.