Not Yet But Maybe

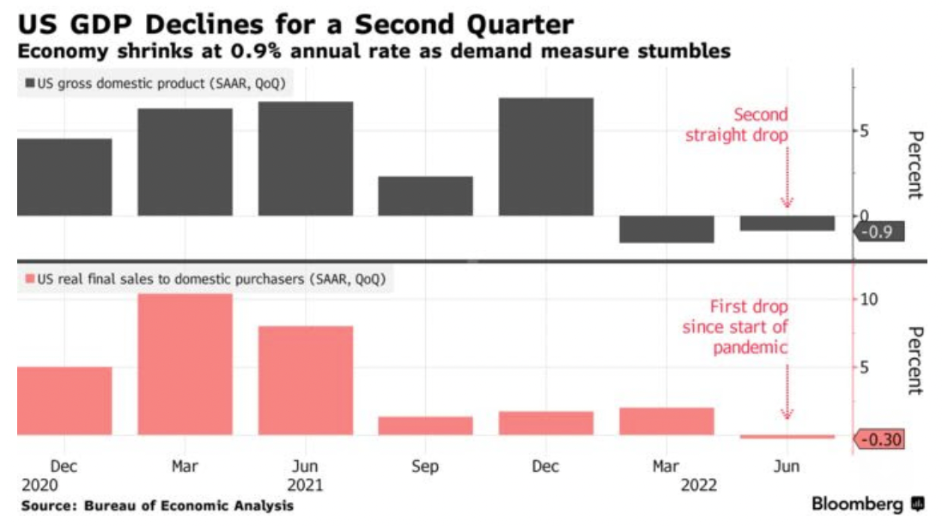

Inflationary concerns in the US have shifted towards recession recently as many accept that it could be the price to pay to bring inflation down. US GDP fell for the second consecutive quarter – the latest reading showed a 0.9% annualised contraction, following a decline of 1.6% (also annualised) in the first quarter of 2022.

Technically, a recession is often defined by two consecutive quarters of negative growth. But according to the National Bureau of Economic Research, the official arbiter of recessions in the US, the country has not entered a recession yet as the labour market remains strong – wages, prices and consumer spending all continue to rise.

More worryingly but unsurprisingly given the rise in prices, personal consumption (about ⅔ of US GDP) fell for the first time since the start of the pandemic. It is hard to see things turn around quickly, especially with a strong dollar. A rise in domestic demand through imports would actually count against GDP measures. A strong dollar could also hurt export competitiveness.

Another supersized move

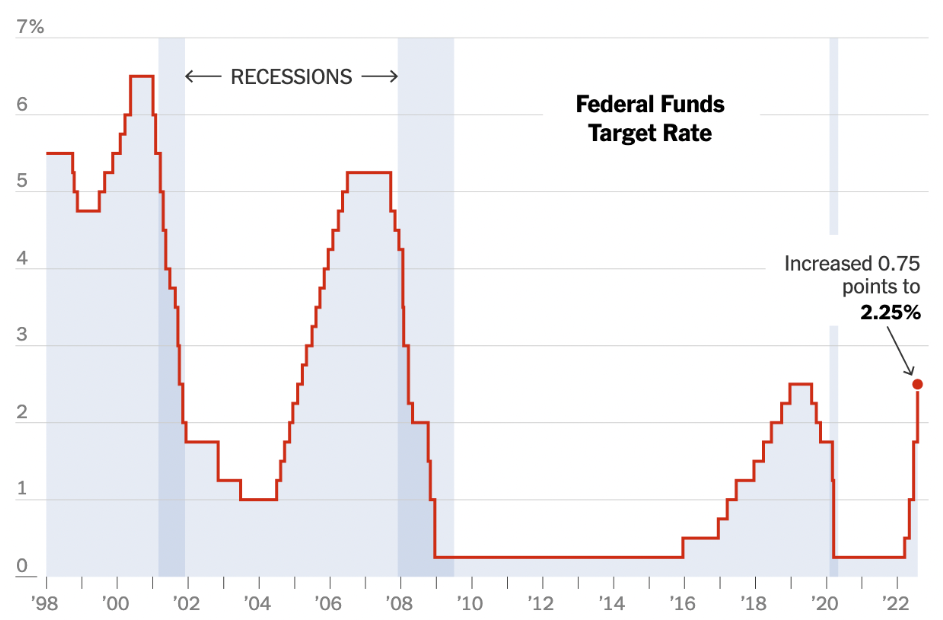

The Federal Reserve raised interest rates by 0.75% in the July FOMC meeting, a move that was regarded as the base case prior to the meeting. Committee members voted unanimously to make the same move as in June, pushing the federal funds rate up to 2.25-2.50%.

Chair Powell left large rate hikes on the table for subsequent meetings, yet major indices gained following the meeting.

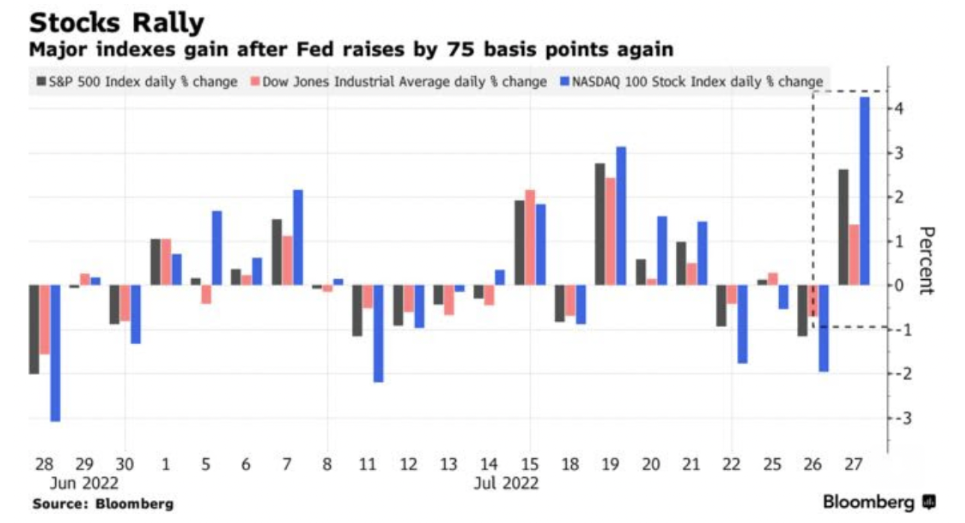

Relief rallies

The S&P 500 index is set for one of its best months – gaining 9% in the last month. 10-year bond yields fell to the lowest since April post GDP release, which showed a technical recession and US equities rallied on Friday on better than expected earnings from big tech – Apple and Amazon.

Regardless of whether we have peak inflation, global bonds are looking at their best monthly gain since 2020. Investors may be signalling that the Fed’s aggressive stance has reached a peak, to the extent that it is going to cause a recession.

5.5% GDP growth target muted

Politburo’s mid-year assessment took place on Jul 28. There was no new stimulus and the 5.5% GDP growth target was not mentioned, which the market considered as a cut. The meeting addressed China’s property issues as ‘to ensure the delivery of housing’ and for local governments to be held primarily accountable in home delivery.

We see some local governments are helping. The acquisition of properties from non-SOE developers for the usage of affordable housing is one of the potential solutions. Zhengzhou is mobilising a relief fund with a total scale yet unknown, and is proposing four solutions for key developers operating in the city. New home sales momentum weakened, the rate ran slower vs. Jun 2022, overall sentiment turned more cautious.

The delinquent mortgage loans would continue to be a drag on market sentiment. No one really can assess a full picture for the commercial banks at the moment. China plans a real estate fund worth up to CNY 300 billion for the distressed sector, China Construction Bank will take the lead. Considering the fact that banks can gear up the leverage further, the ultimate borrowings can be bumped up to 1-2 trillion.

Jul 22 China’s disappointing manufacturing Purchasing Managers’ Index dropped to 49, from 50.2 in Jun and 49.6 in May, implied a weakened recovery momentum. Fixed Asset Investments remained a key driver, construction industry PMI reached 59.2.

On Friday, the US SEC put Alibaba on its provisional list for delisting after Alibaba released its annual report. This followed the same practice with its other ADR peers. Alibaba announced the change of primary stock listing to HK. Negotiations to solve the audit papers access are ongoing, according to both US and Chinese officials, but a resolution is unclear. In addition, Jack Ma plans to relinquish control of Ant Group, part of the company’s effort to appease regulators. It lured the fears of further regulatory control for the TMT industry.

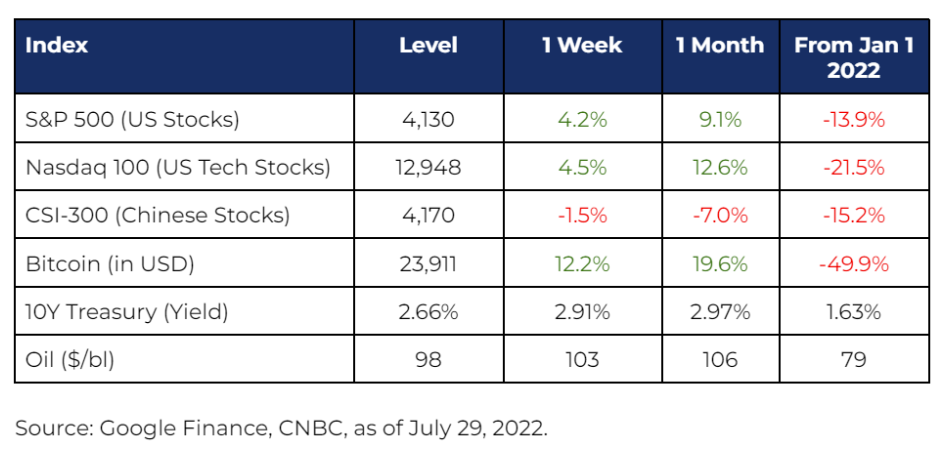

Market Stats