Getting Ahead of Themselves

Usually, after FOMC decisions, we get to hear nuances and opinions from various members through interviews. In Chair Powell’s press conference the previous week, he left a third 75bps hike on the table, but market participants saw it as a “pivot” (potentially slower rate hikes in the future) and stocks rallied.

This week, members tried to correct that potential misconception. Recall that the last rate hike was unanimous, meaning that members are hawkish across the board. Mary Daly, of the San Francisco Fed (who is not voting this year) and can afford to be more candid, said that “Markets are getting ahead of themselves on Fed cutting rates”.

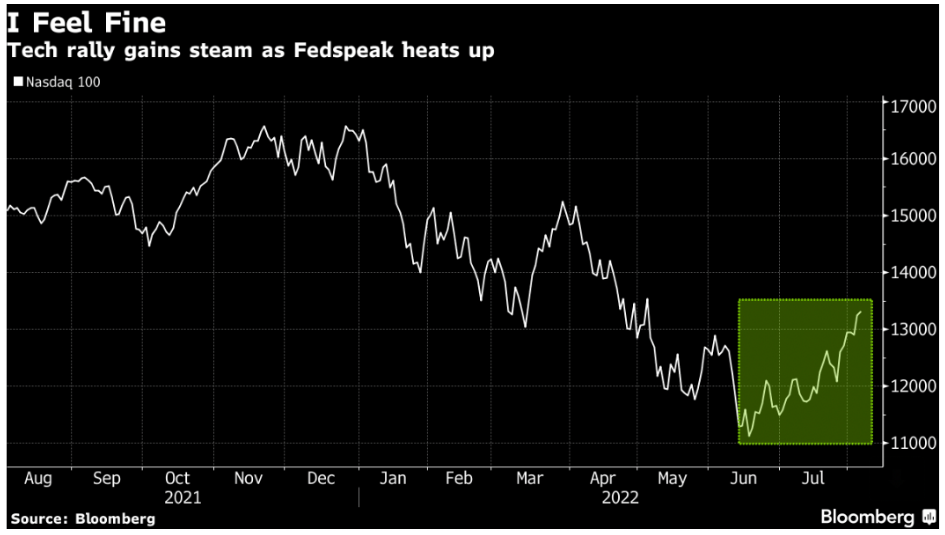

A tale of two markets

The bond market took those comments to heart: with both the 2 year and 10 year treasuries up higher by 20-25 bps but the equity market (using Tech stocks as a proxy) continued to rally.

The optimism might have some legs – ultimately, equity returns are driven by earnings growth, which have overall turned out better than expected for key bellwether companies. However, it would be too soon to tell if this can continue as companies adjust to tighter financial conditions.

Still Rosy

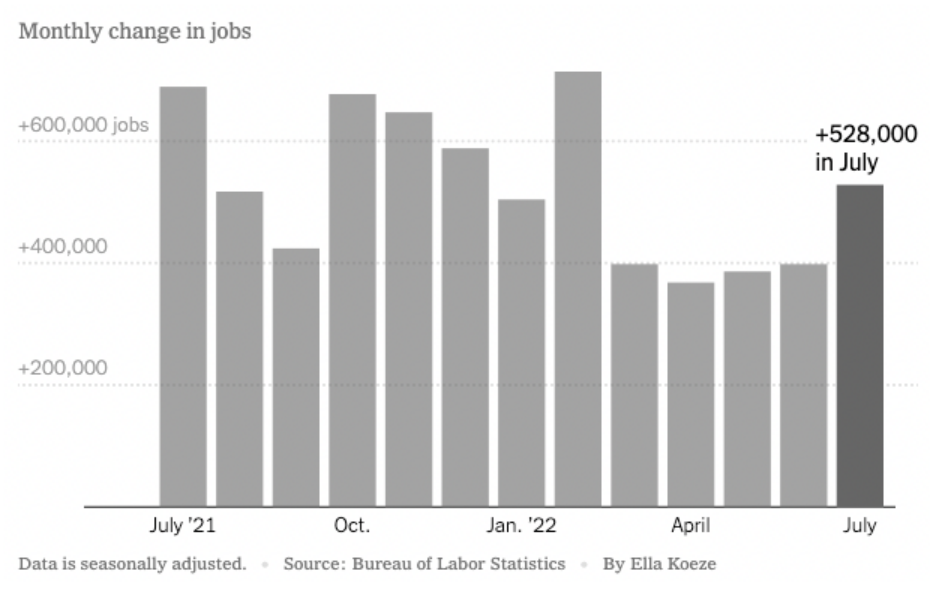

July saw another stellar jobs report, with non-farm payrolls coming in at 528,000 (vs consensus of 250,000). For context, usually late in the economic cycle ( as we are now), job growth of around 250,000 new payrolls is considered to be a good showing.

The unemployment rate fell 0.1% to 3.5%, the lowest since 1969. The US labour market has now recovered all the jobs (and some) lost during the pandemic. Job gains have been consistent across industries, sending a strong support signal to Chair Powell’s assertion that the US economy is not in a recession. Not yet, at any rate.

However, in order to have the Fed pivot that market participants are hoping for, we will also need to see a meaningful slowdown in inflation readings.

Recurring headaches

Chinese equities had quite a week, with the high-profile visit of US House Speaker Nancy Pelosi (third in line to the US Presidency) to Taiwan, despite warnings from China not to go. Stocks initially fell but recovered to end the week flat (using CSI-300, 300 largest stocks traded on the Shanghai Stock Exchange and Shenzhen Stock Exchange as a proxy).

Aggressive restrictions and partial lockdowns continue (with less global attention than before) in major cities, reducing domestic tourism and consumer spending.

Hainan Province started massive Covid testing from Sunday with more local infections, also conducted static management for Sanya – 80k tourists are stranded . Meanwhile Chinese authorities shortened the length of suspensions for inbound airline flights that carry passengers infected with Covid-19.

Real estate headaches continue as well. According to data released by China Real Estate Information Corp, sales at China’s top 100 developers fell 40% compared to a year ago. Their July sales were down 28.6% from June month on month, indicating a weak sentiment among buyers. The first home mortgage rate has dropped to 5.07%, which is the lowest since 2015.

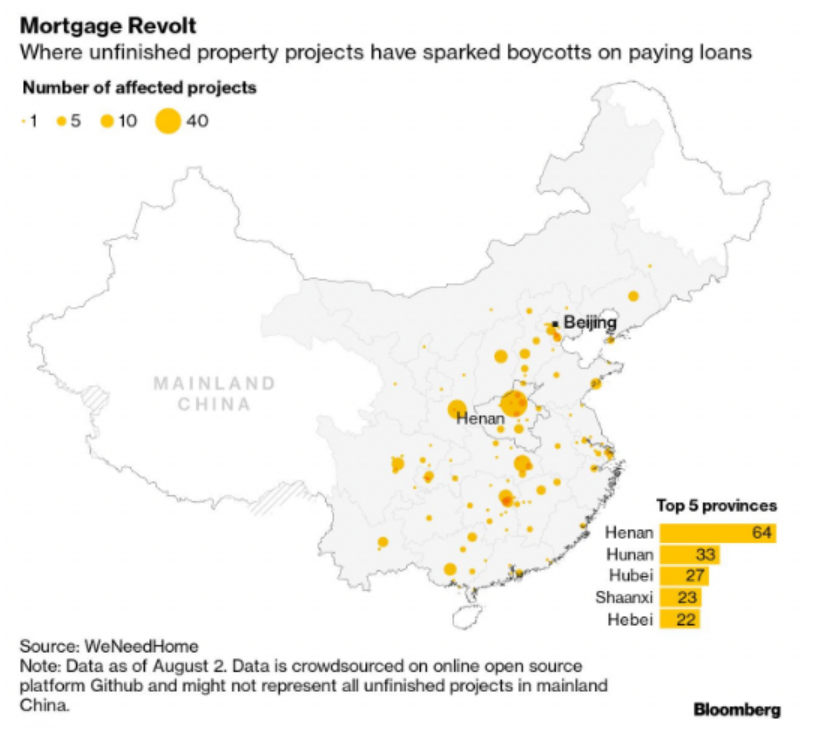

Additionally, unfinished property projects have led to mortgage boycotts by hundreds of thousands of middle class buyers. Although China’s Politburo has promised to prioritise the delivery of unfinished homes, the local government will take some time. If the property market could not turn around for the rest of the second half, all listed private property developers would be in big trouble. Their operating cash flow needs are huge. Take example, Evergrande Group, once the Top 1 property developer in the world, burnt around CNY 20B in monthly operation.

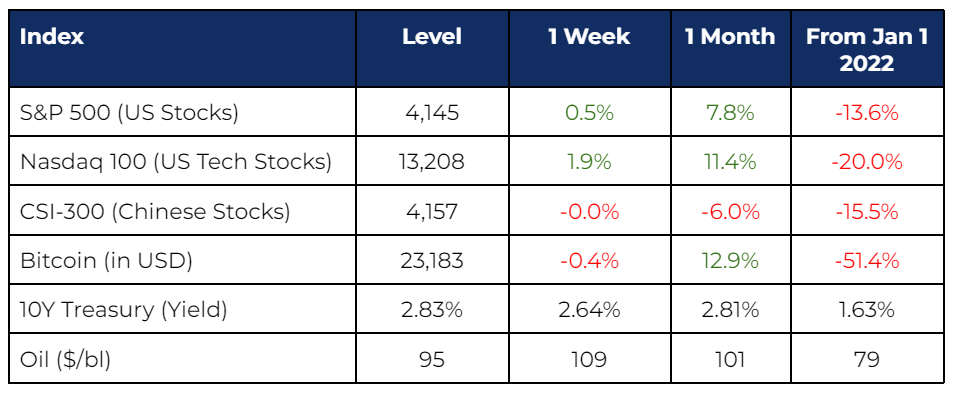

Market Stats