Investors seeking value in a volatile market are piling into a new trade: HALO, a basket of “boring” businesses that are hard to replace despite technological and economic disruptions. Here’s our take on what it means for markets and your money.

What exactly is HALO?

HALO stands for “Heavy Assets, Low Obsolescence” stocks. These are businesses that have been considered “boring” by investors for their lack of change over the years. They include companies holding real assets, building everything from logistics networks to roads and bridges.

These “boring” businesses have turned out to be exciting stocks in the era of artificial intelligence. AI is forcing a historic build-out in infrastructure, including data centres and energy grids, while increasingly capable AI agents are disrupting software business models, automating white-collar tasks. Against this backdrop, heavy-asset businesses look less fungible.

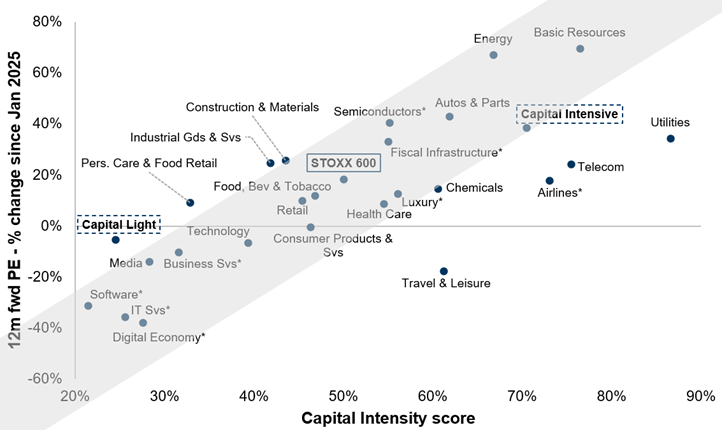

You can see this phenomenon playing out in the chart below, which focuses on Europe. “Capital-intensive” stocks (i.e. businesses that require lots of investment upfront) have clearly done better than their “capital-light” counterparts over the last 15 months or so.

Source: FactSet, Datastream, Bloomberg, Goldman Sachs Global Investment Research.

What it (really) means

HALO may be a new acronym, but it represents an old idea: the rotation from “growth” (rapidly expanding, often innovative companies) to “value” stocks (more stable, profitable businesses that tend to return more cash to shareholders). This rotation typically happens when investors seek shelter from inflated valuations and shifting economic tides.

HALO also reflects the shift towards industries in the global economy. Trillions of state capital is being poured into heavy industries as national and economic security move up the policy agenda, especially in strategic areas like energy and semiconductors. This effectively means governments globally are underwriting long-term capital inflows into heavy-asset sectors.

What are the hottest HALO trades?

In our view, there are several sectors (and some countries) that stand out for their strong HALO characteristics. Read to the end to curate your own HALO trade on Syfe!

- Mining: The physical backbone of AI (data centres, power grids, etc) runs on copper, iron, and steel. Mining companies sit at the nexus of these materials’ supply chains. These are assets defined by scarcity. Commodities are hard to find. Mines take years to be approved and decades to build.

- Utilities: From power grids to telecom towers and toll roads, utilities are the unglamorous infrastructure that everything else runs on. These assets take lots of time and capital to construct, play an essential role in the economy, and produce regular revenue streams (often passed on to shareholders in the form of dividends).

- Defence: Industry leaders in defence hold engineering know-how and regulatory relationships that no new entrant can replicate quickly. They are in for a boon as geopolitical risks ramp up, prompting governments globally to spend more on defence.

- Industrials and Machinery: To build these things, you need machines. Industrial manufacturers (of trucks, turbines, and other heavy equipment) are direct beneficiaries of the boom in capital expenditure.

- Europe & Japan: After decades of underinvestment in industry, Europe is directing capital into energy, defence, and infrastructure at a pace not seen in a generation. Japan, for years mocked for keeping its heavy, “inefficient” industries alive, now possesses a rare industrial base that much of the world is scrambling to rebuild, with highly specialised capabilities in materials and manufacturing.

Should I go HALO now?

Before answering this question, consider the trade-offs.

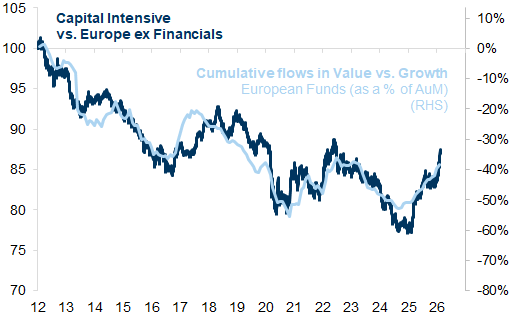

The opportunity – you might (still) be early: Despite the recent surge, investors remain largely under-allocated to this theme. Over the past decade or so, fund flows into “growth” funds have been relentless (see the example of Europe in the chart below). There could be more room to go for HALO as “value” funds close that gap.

Source: Goldman Sachs Research.

The risk – AI surprise: AI is developing at breakneck speed. Further evolution could create new beneficiaries. New AI models could bring capital-light businesses back in favour, and some HALO stocks could turn out to be less safe than they look. Morgan Stanley points to the disruption of railroads by aviation and trucking as proof that true permanence is rare in history.

Long story short: On balance, HALO is not quite a magical bunker in a risk-prone market, as characterised by some commentators. But the concept does capture the market’s zeitgeist in the age of AI disruption. It can be used as a targeted tool to shore up your portfolio’s resilience. Most importantly, it can help you stay invested, which is the key to building long-term wealth.

Risk Disclosures

Investment involves risks including possible loss of the principal amount invested. The portfolio and/or the constituent funds in the portfolio may not achieve their investment objectives. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment. Investors should consider the investment objectives, risks, charges and expenses carefully before investing.

Some of the risks within the constituent funds include market risk (potential losses from market-wide changes), liquidity risk (difficulty selling an asset), interest rate risk (changes in interest rates affecting the market value), credit risk (risk of default on a debt or default of an exchange), and fund management risk (the chance that the constituent fund managers’ investment strategies do not work as planned).

Some of the constituent funds may also use derivatives. Transactions in options (and derivatives generally) also carry a high degree of risk. Selling (“writing” or “granting”) an option generally entails considerably greater risk than purchasing options. Although the premium received by the seller is fixed, the seller may sustain a loss well in excess of that amount. The seller will also be exposed to the risk of the purchaser exercising the option and the seller will be obliged either to settle the option in cash or to acquire or deliver the underlying investment. If the option is “covered” by the seller holding a corresponding position in the underlying investment or a future on another option, the risk may be reduced. You should understand the risks associated and be willing to assume the risks before making any investment decision.

The information in this website is for information only. The information and opinions contained in this publication has been obtained from sources believed to be reliable at the time of writing, but Syfe makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose. Opinions and estimates are subject to change without notice. Syfe does not provide legal, tax or accounting advice.

There is no assurance that the credit ratings of any securities mentioned in this publication will remain in effect for any given period of time or that such ratings will not be revised, suspended or withdrawn in the future if, in the relevant credit rating agency’s judgment, the circumstances so warrant. The value of any product and any income accruing to such a product may rise as well as fall.

Information on this website is not and should not be construed as an offer to sell, or a solicitation of an offer to buy any security, investment product or service, nor a distribution of information for any such purpose.

")