A key policy meeting in Beijing this week reaffirms that policymakers are taking their time with economic growth, prioritising quality over velocity. We see greater dispersion in markets developing from this stance, favouring strategic sectors, industry leaders, and patient investors.

What Happened

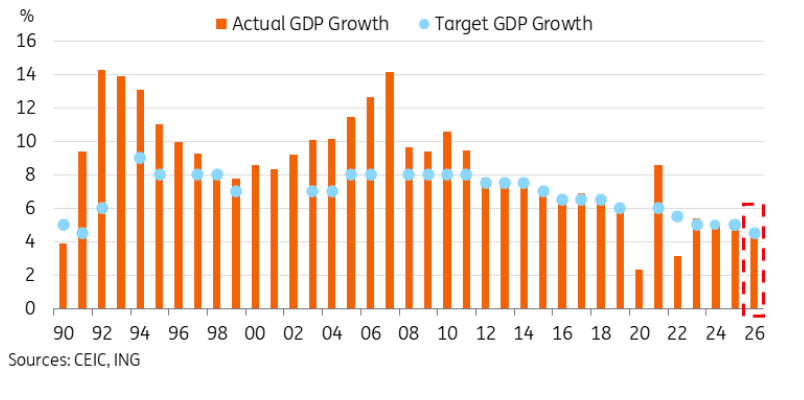

China kicked off the “Two Sessions” this week, the forum where the government unveils targets for GDP, budget deficit, and key policies for the year. Markets watch this meeting keenly to gauge how willing and able policymakers are to support the economy. This week’s meeting, the first in a new five-year policy cycle, will set the tone for the rest of the decade.

At 4.5%-5%, the GDP target is the lowest in over three decades. This reflects China’s structural slowdown as the government shifts the economy from emerging market-style investment-led growth, underpinned by the housing market and infrastructure, to consumption-led growth seen in more mature economies. The budget deficit, maintained at 4% of GDP, signals more fiscal support to boost growth and fight deflation.

But that firepower will be highly targeted. There’s no sign of a fiscal “bazooka”, any cash handouts, or reflation of the gigantic real estate market. Their absence underscores Beijing’s long-term view on the economy’s rebalancing and generating “high quality” growth. In all, China’s policy stance is more akin to the art of “Tai Chi” – slow moves that are ultimately good for the economy’s health – rather than the lightning actions in a Kung Fu movie.

Why It Matters for Markets

Stepping out of the “uninvestable” narrative of the pandemic years, Chinese stocks rallied more than 30% in 2025, outpacing the US and many major markets. The worst seems to be over for the economy. The property market, though still sluggish, appears to be finding a floor. Meanwhile, new growth drivers are emerging in tech and consumption.

In the process, valuations have re-rated from being dirt-cheap to more reasonable (although still attractive compared to the US and the global benchmark). Investors are now looking for more evidence of earnings growth to extend the rally, or policies that could fuel earnings growth. This is why the market’s performance has been more muted so far this year.

With a slow economic recovery, winning industries will pull away from lagging ones. Sector selection is becoming more important.

Who Stands To Win?

Tech is the standout winner in this year’s “Two Sessions”. The government is emphasising the need for self-reliance as the rivalry with the US heats up. This means going beyond building a company or two that can compete with OpenAI, but constructing whole supply chains. Other than AI, priorities include artificial intelligence, supercomputing, semiconductors, aerospace, humanoid robots, 6G, bio-pharmaceuticals, and the “low-altitude” economy (e.g. drones).

You can get a sense of this in the breakdown of investments. RMB 800 billion of the new RMB 1.3 trillion long-term government financing raised this year will be allocated to strategically important projects like high-tech manufacturing. Financial institutions are also directed to lend more to these projects.

Boosting domestic demand is another priority, with consumer confidence still weak. The continuation of the consumer goods trade-in programme (albeit scaled back slightly) and a new fund worth RMB 100 billion to promote domestic demand should benefit consumer durables companies. More favourable holiday and consumption tax arrangements would benefit a broader set of companies tied to domestic consumption, from tourism to retail.

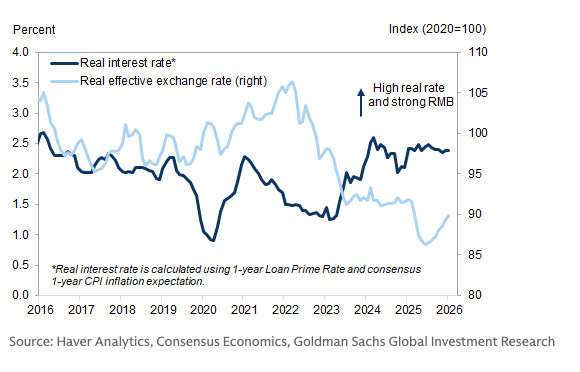

But given the patient stance policymakers take on boosting consumption, the sector as a whole is unlikely to see the sort of breakout growth in the tech industry. Another data point that reflects this limitation is China’s real interest rates (after taking account of inflation), which, despite the headline cuts to financing costs, are kept close to their highest levels in a decade.

Then, there are the “anti-involution” winners, which we highlighted a few weeks ago. Beijing is actively forcing supply discipline in overcrowded sectors like electric vehicles, solar, and batteries to hold off deflation. In these industries, those already winning (in market share and pricing power) will likely make more gains, as policymakers encourage consolidation. Industries like EV, in particular, where Chinese companies are already the leading players, will be in focus. Those already exporting to emerging markets that welcome Chinese products are better positioned to navigate the increasingly protectionist global trade order.

Where should China be in my portfolio?

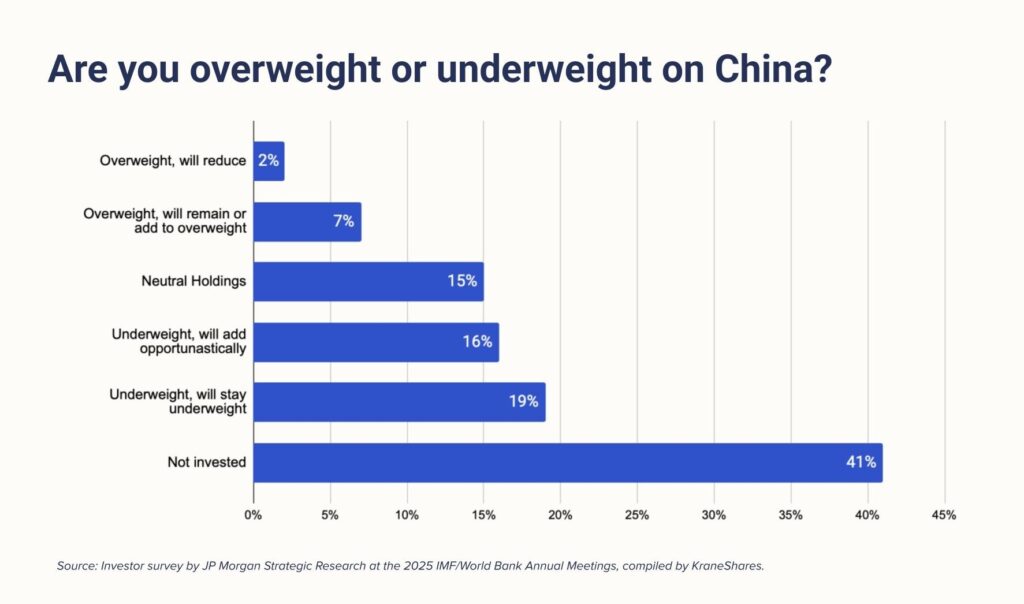

China has the world’s second-largest economy and stock and bond markets. Its weighting in the global benchmark, however, is still in the low single digits. This is why our globally diversified Core Equity100 portfolio has historically taken an overweight position on China. There is potential for more global investors to go in this direction, given that many of them still hold no exposure to this market at all. See this survey taken at the IMF/World Bank Annual Meetings last year, which our partners at KraneShares highlighted at our outlook event last week.

Source: Investor survey by JP Morgan Strategic Research at the 2025 IMF/World Bank Annual Meetings, compiled by KraneShares.

Our China Growth portfolio offers more targeted exposure with a group of leading companies across internet, consumer, healthcare and more.

Risk Disclosures

Investment involves risks including possible loss of the principal amount invested. The portfolio and/or the constituent funds in the portfolio may not achieve their investment objectives. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment. Investors should consider the investment objectives, risks, charges and expenses carefully before investing.

Some of the risks within the constituent funds include market risk (potential losses from market-wide changes), liquidity risk (difficulty selling an asset), interest rate risk (changes in interest rates affecting the market value), credit risk (risk of default on a debt or default of an exchange), and fund management risk (the chance that the constituent fund managers’ investment strategies do not work as planned).

Some of the constituent funds may also use derivatives. Transactions in options (and derivatives generally) also carry a high degree of risk. Selling (“writing” or “granting”) an option generally entails considerably greater risk than purchasing options. Although the premium received by the seller is fixed, the seller may sustain a loss well in excess of that amount. The seller will also be exposed to the risk of the purchaser exercising the option and the seller will be obliged either to settle the option in cash or to acquire or deliver the underlying investment. If the option is “covered” by the seller holding a corresponding position in the underlying investment or a future on another option, the risk may be reduced. You should understand the risks associated and be willing to assume the risks before making any investment decision.

The information in this website is for information only. The information and opinions contained in this publication has been obtained from sources believed to be reliable at the time of writing, but Syfe makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose. Opinions and estimates are subject to change without notice. Syfe does not provide legal, tax or accounting advice.

There is no assurance that the credit ratings of any securities mentioned in this publication will remain in effect for any given period of time or that such ratings will not be revised, suspended or withdrawn in the future if, in the relevant credit rating agency’s judgment, the circumstances so warrant. The value of any product and any income accruing to such a product may rise as well as fall.

Information on this website is not and should not be construed as an offer to sell, or a solicitation of an offer to buy any security, investment product or service, nor a distribution of information for any such purpose.

")