China’s real estate market, once the emblem of robust growth, is currently facing notable challenges. Country Garden, a leading property developer in China, recently reported significant financial loss and missed bond payments, sparking industry-wide concerns.

What caused the Property Sector’s Decline?

While many intricate factors are at play, a few primary reasons include:

- Demographic Shift: The fertility rate in China decreased to a record low of 1.09 in 2022. This trend indicates a reduced future demand for housing as the population growth slows, making property a less appealing long-term investment.

- Over-investment in the Real Estate: Since China’s market reforms began in the 1980s, its real estate market has been instrumental in driving the nation’s economic growth. Historically rising prices fostered over-optimism, leading to excessive investment in this sector.

- Regulatory Adjustments: Towards the end of 2020, the Chinese government decided to tighten the reins to reduce the leverage in the property sector, leading to liquidity constraints for many developers.

- COVID’s Ripple Effects: The pandemic’s economic impact has not done the property sector any favors, as people are becoming more cautious about spending.

The confluence of these factors has dealt significant blows to the industry.

Market Reactions So Far

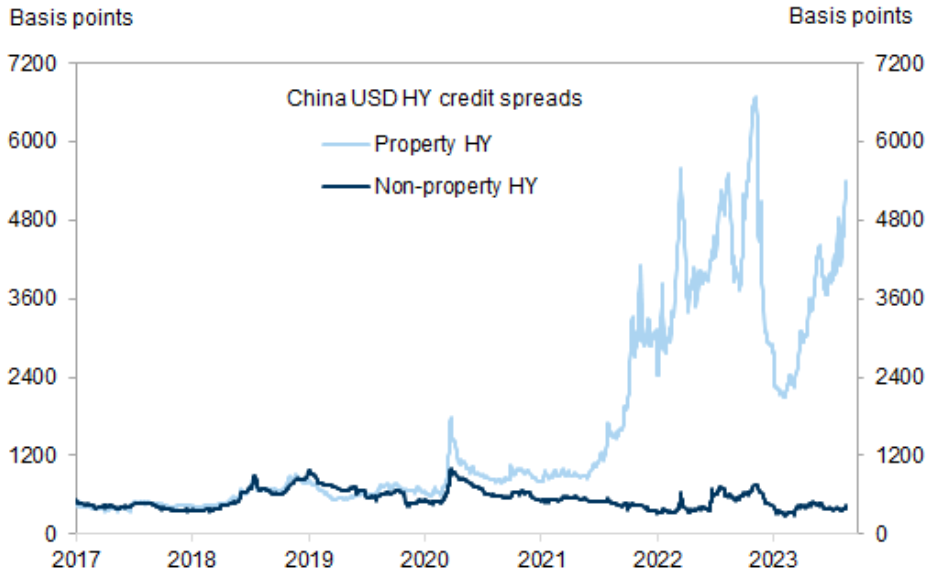

Following the headline news, equity markets experienced volatility with foreign investors showing caution. Interestingly, the credit market reacted more calmly. The impact has largely been confined to property high-yield bonds, with limited spillover to other sectors. Credit spread, a measure that reflects the risk investors are willing to take to hold certain bonds, spiked for high-yield property names but remained relatively unchanged for other sectors.

Property HY credit spreads rose sharply, but relatively unchanged for other sectors

Source: GS Research, ICE-BAML, 18 August 2023

The Big Question – Can the Systematic Risk be Contained?

We believe the overall risks are manageable. The property crisis could escalate into a major economic risk if it severely affects the banking system. Currently, the impacts on the banks appear contained. Here are some reasons behind our thinking:

- While property debt is substantial (Rmb 58tn, 47% of GDP) , two thirds of which is mortgage loans. The effective loan-to-value (LTV) ratios of the mortgage loans are generally healthy, suggesting homeowners have sufficient financial cushion to withstand a notable drop in property prices.

- Trust loans, sometimes referred to as “shadow banking”, constitute only 1% of China’s total loans. Trust companies have approached property with caution since the end of 2019.

- China’s government maintains strong control over its banks, reducing the likelihood of sudden, chaotic financial disruptions.

Potential Policy Interventions

It’s important to note that these problems, while significant, are not impossible to overcome. The Chinese government has a track record of successfully handling economic crises in the past. We are likely to see more policy support.

Continued monetary policy easing: We are likely to see broader monetary easing measures, including interest rate cuts and reductions in the reserve requirement ratio (RRR), to stabilize the economy.

Targeted Stimulus Measures on housing market: A recent important official statement omitted the familiar phrase, “houses are for living in, not for speculating.” This suggests Beijing might be considering new supportive measures for the housing market. While no major announcements have been made, we believe these measures could soon be introduced in various cities. Potential strategies might encompass reducing mortgage rates, relaxing home buying restrictions, and extending more loans to both property developers and consumers.

State-Funded Bailouts: While Beijing has traditionally avoided such measures, considering the size and importance of the real estate sector, state-funded bailouts or support for key players might be possible.

How are Syfe’s Portfolios Positioned?

In our Cash+ portfolios, the E Fund (HK) US Dollar Money Market Fund and CSOP US Dollar Money Market ETF have no exposure to the China property sector.

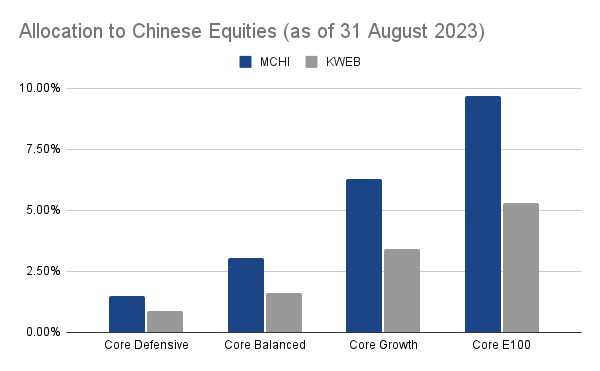

For Core portfolios, we have exposure to Chinese equities via the iShares MSCI China ETF (MCHI) and the KraneShares CSI China Internet ETF (KWEB). Here’s a breakdown of holdings across different Core portfolios in the chart below. As of 30 June 2023, MCHI and KWEB have allocations of 3.1% and 3.6% in the real estate sector respectively. Thus, the four Core portfolios have limited exposure to China’s real estate sector.

Source: Syfe, 31 July 2023

For the Income+ portfolios, Income+ Pure has allocated 25% to the HSBC Asian Bond Fund while Income+ Enhance has allocated 25 % to the HSBC Asian High Yield Bond Fund. Based on our estimates, as of 31 July 2023, their exposure to China Real Estate credit (including both investment-grade and high-yield bonds) stands at 2.8% and 3.4%, respectively.

For Thematic – China Growth portfolio, As of 31 August 2023, real estate accounted for 1.7% allocation within the portfolio.

In summary, the exposure to China’s property sector is relatively small across all our portfolios.

")