Experts recommend investing consistently for retirement and other financial goals. That’s where dollar cost averaging comes into play.

What is dollar cost averaging?

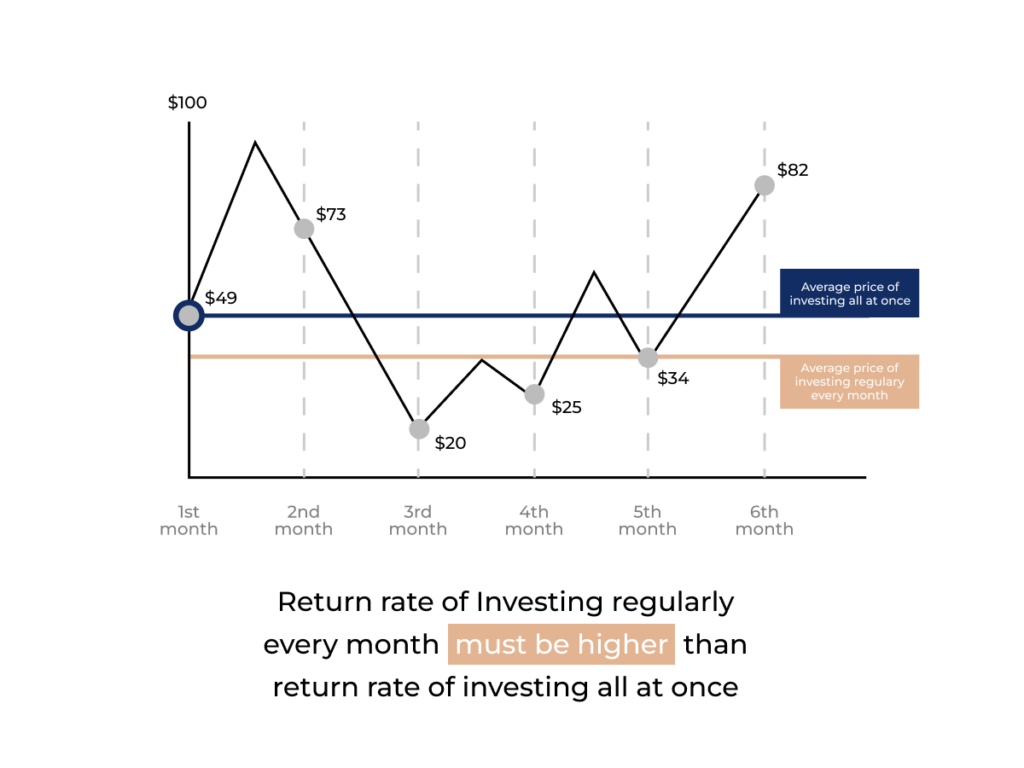

Dollar cost averaging (DCA) is an investment strategy that helps you cushion the impact of market fluctuations through regular investments, regardless of market conditions. The idea is that by consistently investing a fixed sum of money over a period of time, you end up buying more shares when prices are low and fewer shares when prices are high.

Over the long term, the cost of all your investments purchased are averaged out. This mitigates the impact of short-term market fluctuations on your portfolio and eliminates some of the risky guesswork involved in trying to time the market.

How does it work?

Two types of dollar cost averaging exist. The first is where you set up an automatic investment plan so you can invest a fixed sum of money at regular intervals (weekly, monthly, etc.) This is a smart investment strategy – you’re getting into the habit of saving and investing regularly, and you’re growing your net worth steadily over time.

The second type is where you have a huge sum of money – say your bonus or an inheritance – and you decide to invest it in equal parcels over a period of time, instead of all at once.

For some investors, this strategy takes away some of their fear of investing. While no one can predict how the markets will behave, it’s nerve-wracking all the same not knowing if you will be investing all your money the day before a downturn. Dollar cost averaging soothes this worry, and is a much wiser option than leaving all your money in the bank.

Why dollar cost averaging makes sense

One of the most important benefits of dollar cost averaging is psychological. Because you’re investing consistently regardless of market conditions, your emotions are removed from the equation, making you less susceptible to the investing biases other people may hold.

For instance, most people prefer avoiding losses more than they like winning – a behaviour formally known as loss aversion. When the market plummets, some investors may panic and sell their investments at the market bottom. If you’re dollar cost averaging, you’ll instead be purchasing your investments at an attractively low price.

Over the long term, markets tend to go up. Dollar cost averaging helps you recognise that market downturns can be an opportunity, not a threat.

Additionally, you avoid the risk of mistiming the market with dollar cost averaging. Timing the market – investing whenever you think market conditions are good – doesn’t work over the long run because no one can consistently predict how the markets will perform.

Potential drawbacks to note

One scenario where dollar cost averaging may not be ideal is when markets are rising. Dollar cost averaging into an investment that continues to rise each month keeps you from maximising your gains. If you have the means, this is one situation where a lump sum investment would be better. When the markets are on a confirmed uptrend, say the period of recovery after a downturn, splitting your investments means that portions of your money are left on the sidelines and missing out on potential returns.

But if you remain nervous about investing all your money at once, dollar cost averaging is still a reliable strategy to get some money in the markets and take advantage of the market growth.

How to start dollar cost averaging

In Hong Kong, you can easily start dollar cost averaging by purchasing a regular savings plan (RSP). You’ll have to select which share counters to purchase and take note of the fees and any minimum investment amount.

A simpler, more cost-effective way would be to dollar cost average into Syfe’s Core portfolios. Our flagship Core portfolios comprise various ETFs and individual stocks diversified across multiple asset classes.

Dollar cost averaging is ultimately a logical, non-emotional approach to investing. It may seem boring, investing the same amount consistently every month, but it is this boredom that makes dollar cost averaging such a successful investing strategy.

Ready to put dollar cost averaging into action? Start investing.