Positive sentiment persisted in the first half of 2024, bolstered by robust corporate earnings and easing inflation. However, the market landscape is poised to become more complex in the second half of the year. Ritesh Ganeriwal, our Managing Director of Investment & Advisory, analyses the crucial crossroads of change in the second half, where monetary inflection intersects with the US elections. He also highlights key investment themes to capitalise on H2 market dynamics.

H1 2024 Market Recap: Strong momentum continued

The economic momentum from the first quarter of 2024 continued into the second, resulting in another positive period for equity markets. Initially, stronger-than-expected economic data prompted investors to scale back expectations for central bank rate cuts. However, these concerns eased as the year progressed, and hopes for a soft economic landing revived.

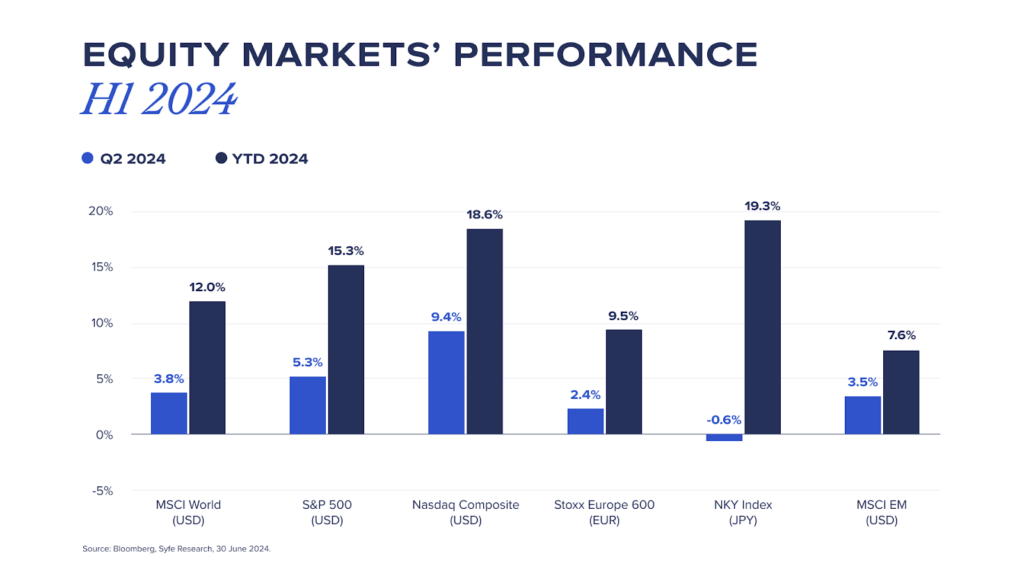

Equities: Against this resilient economic backdrop, global equities gained 3.8% in Q2, bringing the year-to-date (YTD) return to 12.0%. S&P 500 was up more than 15% year to date, its best start in an election year on record. Companies exposed to AI continued to outperform, with mega cap tech names leading the charge backed by strong earnings momentum. As a result, the tech-heavy Nasdaq Index continued its dominance, jumping close to 20% in the first half.

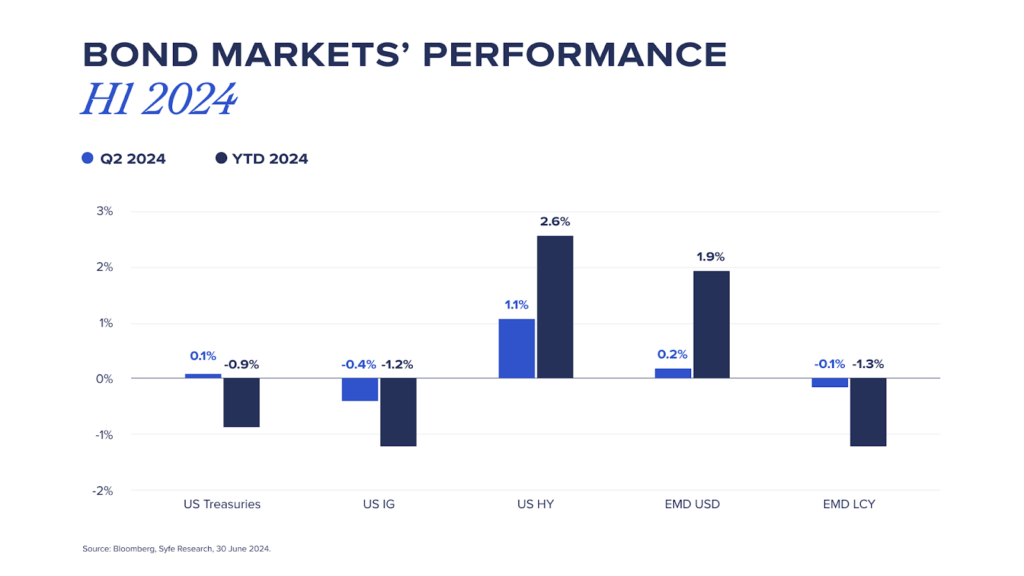

Bonds: In contrast, bond market returns were more subdued. US Treasury yields remained within a narrow range throughout the quarter as investors grappled with varying expectations for rate cuts. Both Treasury and investment-grade bonds were relatively flat for the quarter, posting negative YTD returns. High-yield bonds, in line with the prevailing risk-on sentiment, performed best with a 1.1% return in Q2, maintaining their YTD lead.

As we transition into the second half of 2024, the confluence of evolving monetary policies and the upcoming US election could create a complex backdrop for investing. Let’s explore how these two critical events could shape the financial markets in the near future.

Fed’s H2 Outlook: The beginning of rate cuts?

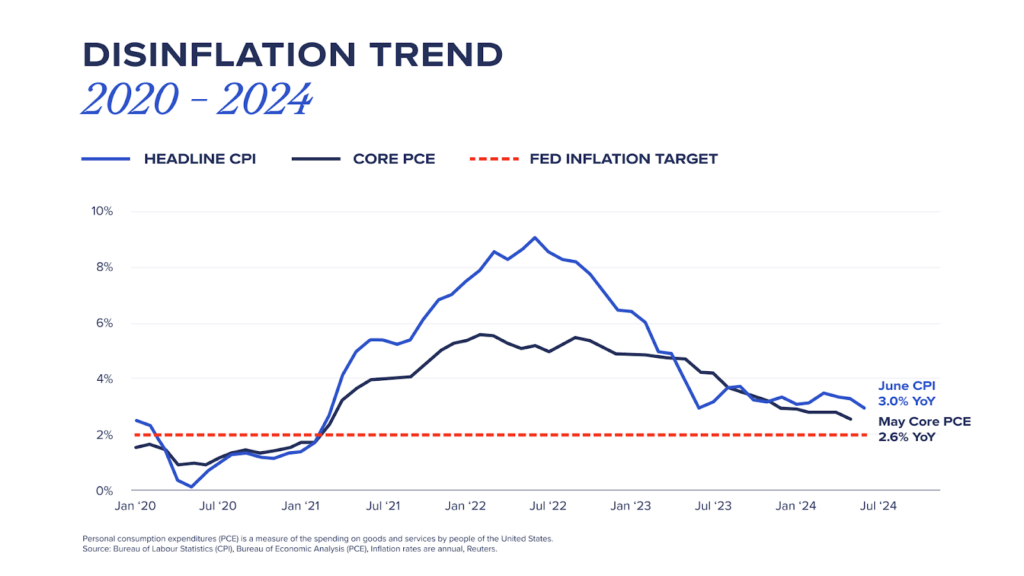

Recent data confirms a disinflationary trend. The Consumer Price Index (CPI) dipped 0.1% in June, bringing the annual rate to 3%—a three-year low. Meanwhile, the Fed’s preferred gauge, the Core Personal Consumption Expenditures (PCE) Price Index, eased to 2.6% in May, inching closer to the Fed’s 2% target.

Fed Chair Jerome Powell, for the first time, indicated a policy shift: the Fed may begin cutting interest rates before reaching its 2% inflation target in response to a cooling job market and a slowing economy. Consequently, market expectations have swiftly adjusted to two rate cuts this year: one in September and another in December.

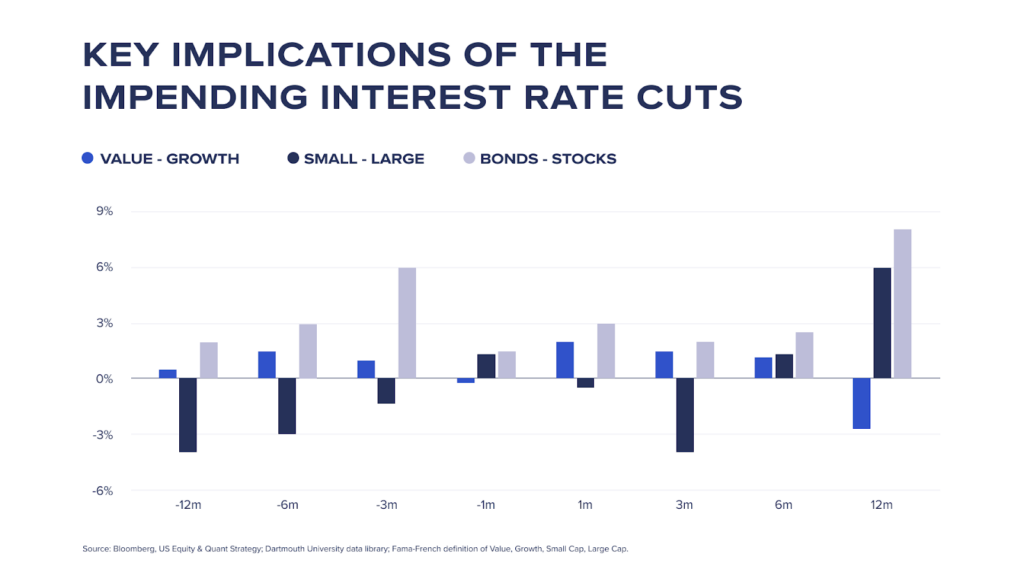

So what are the key implications of the impending interest rate cuts?

Historically, after the first rate cut, value stocks typically outshine growth stocks during the initial six months. Investors shift their focus to these undervalued stocks, seeing them as potential bargains in the new economic landscape.

Similarly, small-cap stocks often catch up and outperform large caps within 12 months, due to their ability to capitalise on lower interest rates.

Across asset classes, bonds have consistently outperformed equities in the 3, 6, and 12-month periods following a rate cut, as rate cuts tend to correlate with economic slowdowns. Bonds are viewed as safer havens during times of economic uncertainty.

US presidential election 2024: Uncertainty looms

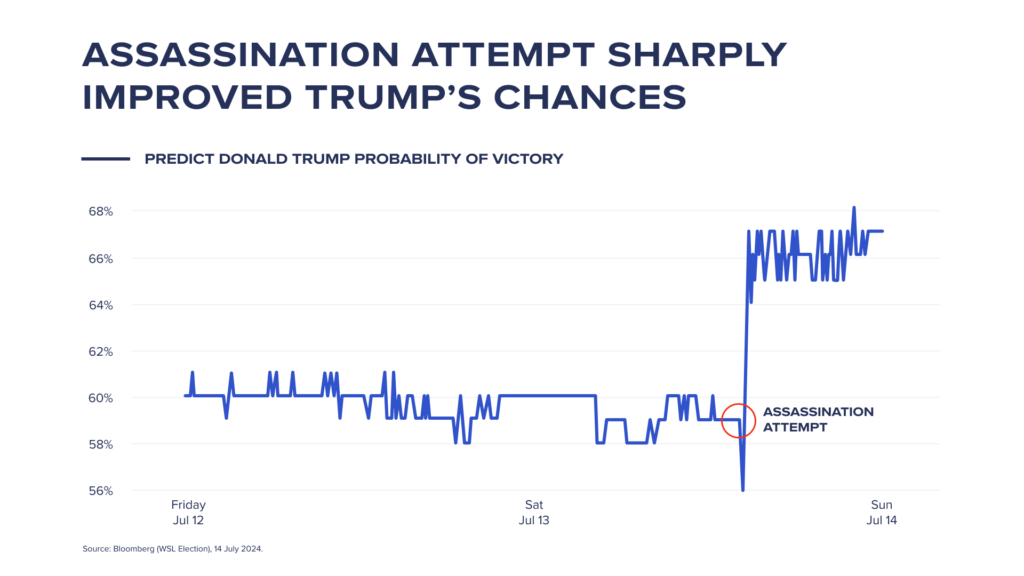

Turning our attention to the upcoming US Elections – this could be a pivotal moment for the US market. The recent failed assassination attempt on Trump has significantly increased his chances of reelection

That said, the US election landscape still remains highly unpredictable. A recent CNN poll shows that after President Biden withdrew from the race, Kamala Harris and Trump are closely matched. Given the fluid nature of election dynamics, these figures could shift significantly as the election date approaches.

Implications of US Presidential Election

Historically, markets tend to be volatile in the lead up to the vote and rebound after the result is known. While short term volatility is expected, equity markets should remain broadly supported.

In case of a Trump win, Sectors such as financials, energy and defence could be key beneficiaries, with the tech sector softening due to more headline and regulatory risks.

China economic trajectory: key takeaways from the Third Plenum

China’s government plays a pivotal role in shaping its economy, and the Third Plenum is a highly anticipated event which focuses on structural reform issues in China. This year’s plenum acknowledged the weak domestic demand and economic challenges faced by China but lacked major policy reforms, leading to muted reaction from the markets.

While the third plenum lacked specific policy decisions, it is important to note that the third plenum is designed to look at China’s economic situation at a high level with further policy decisions mapped out in the weeks to follow. We expect increased fiscal and monetary policy support in the near term to get economic growth back above the 5% level and longer term economic reforms to achieve ‘Chinese style modernisation’.

Take a long-term perspective on the Chinese equities

Chinese equities may remain subdued in the near term. Lacklustre economic data, coupled with the potential for increased trade tariffs due to a possible Trump re-election, could dampen sentiment.

Regardless, we believe in taking a long-term perspective on the Chinese market. A slowing economy often leads to lower valuations, which can present attractive entry points for long-term investors. As China shifts its focus from an export-led economy to a consumption-led one, investors can ride this shift by investing into high growth companies at the forefront of China’s rapidly-evolving “new economy”.

Seeking investments that capitalise on China’s surging healthcare demand and servicing the emerging middle class offer attractive upside potential for investors willing to ride through short-term market turmoil. At Syfe our focus is on balancing investment across both onshore and offshore China companies where there is little overlap and differentiated industry exposure, investor bases, and policy impact which can help smooth the journey through current market conditions while remaining exposed to China’s growth.

Top investment themes in H2 2024: Capitalise on H2 Market Dynamics

With these market dynamics in mind, we have identified three key investment themes for investors looking to capitalise on emerging trends in the latter half of the year.

Theme 1: Lock in attractive yields with bonds

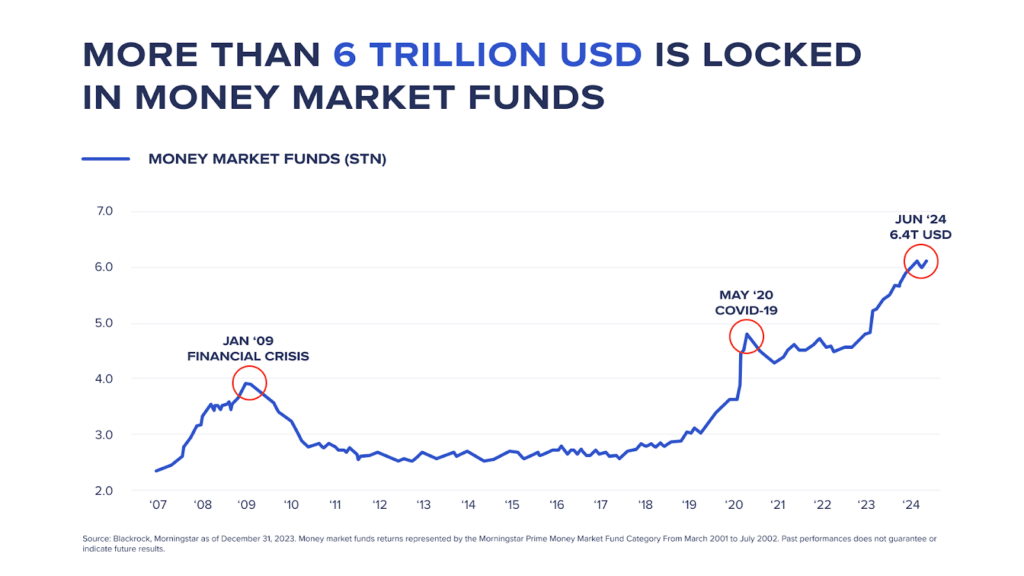

Cash presents significant reinvestment risks. Lock in attractive yields with bonds before the rates drop. We believe the era of elevated yield on cash savings is coming to an end. More than 6 trillion US dollars is still locked in money market funds. As the Fed starts cutting rates, close to 50% of these funds is expected to be reallocated to investments, dominated by bonds.

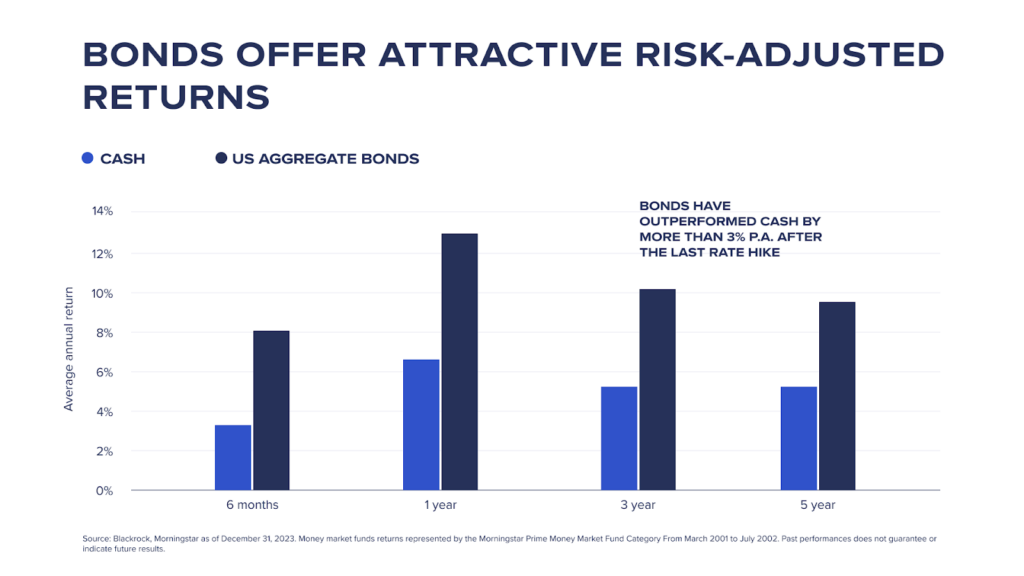

Bonds still also offer attractive risk-adjusted returns and are expected to outperform cash by at least 3% p.a. over the next 3-5 years. The time to act is now as the price action on bonds typically starts taking effect before the actual rate cuts. We recommend investors to lock-in the current attractive yields in the bond market before it is too late!

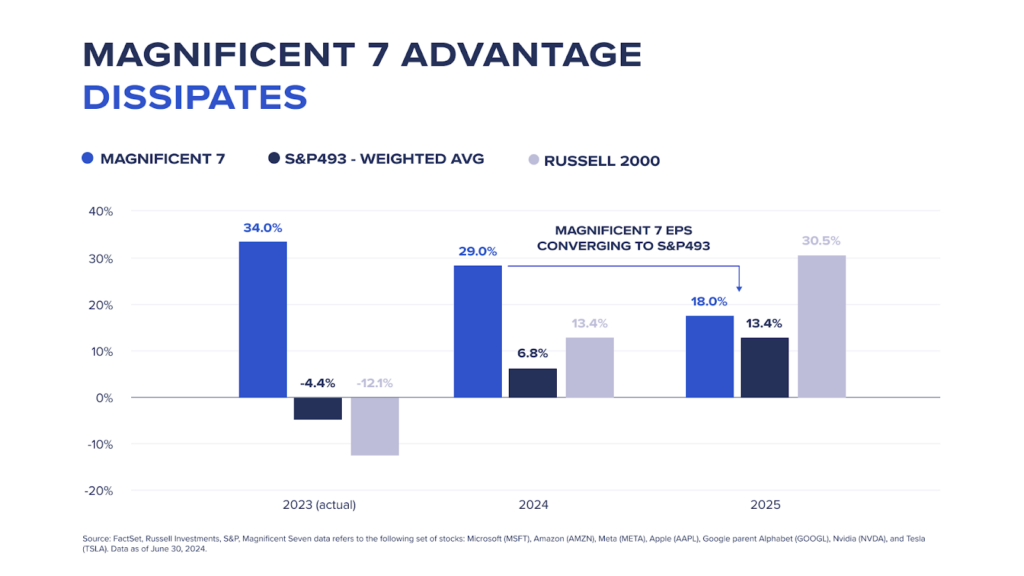

Theme 2: Move beyond Magnificent 7 (Mag 7)

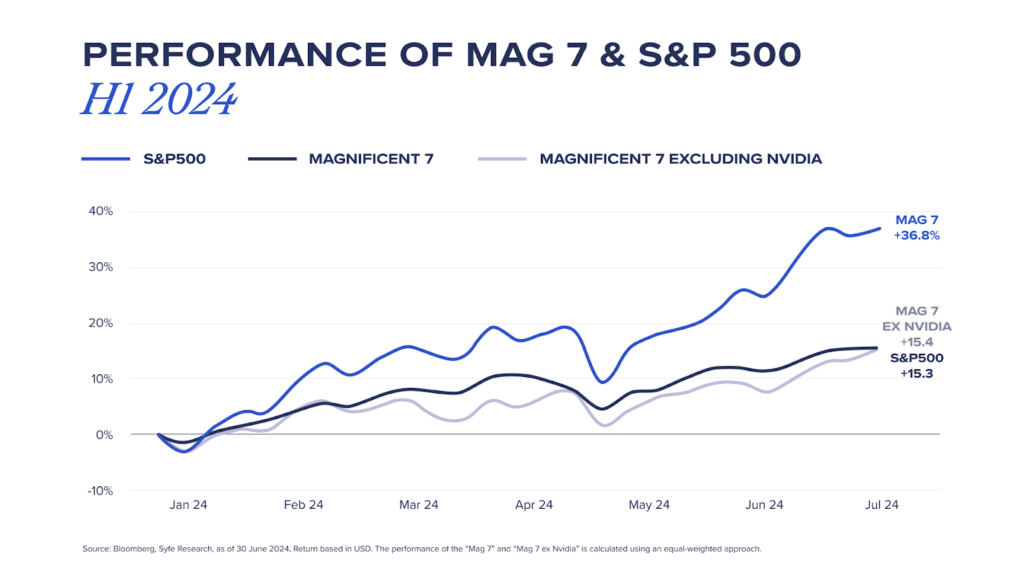

Move beyond the Mag7 and capitalise on sector rotations in equity markets. The concentration risk of mega cap stocks within market cap indices such as S&P 500 has reached unprecedented levels. Despite their collective outperformance, the Mag 7 stocks excluding Nvidia have delivered returns in line with S&P 500 YTD.

Looking ahead, earnings growth in mega cap tech stocks is expected to slow down, while picking up in the small and mid cap space. We are now seeing strong signs of sectoral shifts as rate cuts take hold. We encourage investors to move beyond the Mag 7 stocks and add quality mid and small-cap exposures to diversify and take advantage of the cyclical rotation in the equity markets.

Conclusion

We stand at a pivotal moment where monetary policy and political landscapes intersect, potentially reshaping market dynamics significantly. The recent shift from mega-cap technology companies to small-cap stocks illustrates the fluid nature of investment landscapes. With the Fed poised to cut rates, it’s crucial to re-allocate your idle cash into investments, particularly bonds. For equity portfolios, diversification is key to navigating potential market volatility ahead.

This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone.Past returns are not a guarantee for future performance. Investors should consider his/her own circumstances. The information or advertisement contained herein does not constitute an offer, any solicitation, invitation or recommendation to engage in any investment activities.