Active ETFs are rapidly gaining ground, now accounting for over 80% of new launches in 2026. These active strategies are attracting a growing share of inflows and offering investors more flexibility. Aman Pujara, Director of Quantitative Research and Portfolio Construction at Syfe, sat down with MoneyFM host Michelle Martin to dive into the shifting ETF landscape in the age of active management.

Building a portfolio is personal. Every investor has different objectives, risk appetite, and time horizon, and requires a different mix of investment strategies to achieve their goals.

In this article, we explain the key differences between these “building blocks”, which of these are right for your portfolio, and how you can begin building on Syfe today.

- Active and Passive: The Traditional Choices

- Pros and Cons: Things to Consider

- A “Smarter” Way Forward

- Building Your Portfolio on Syfe

Active and Passive: The Traditional Choices

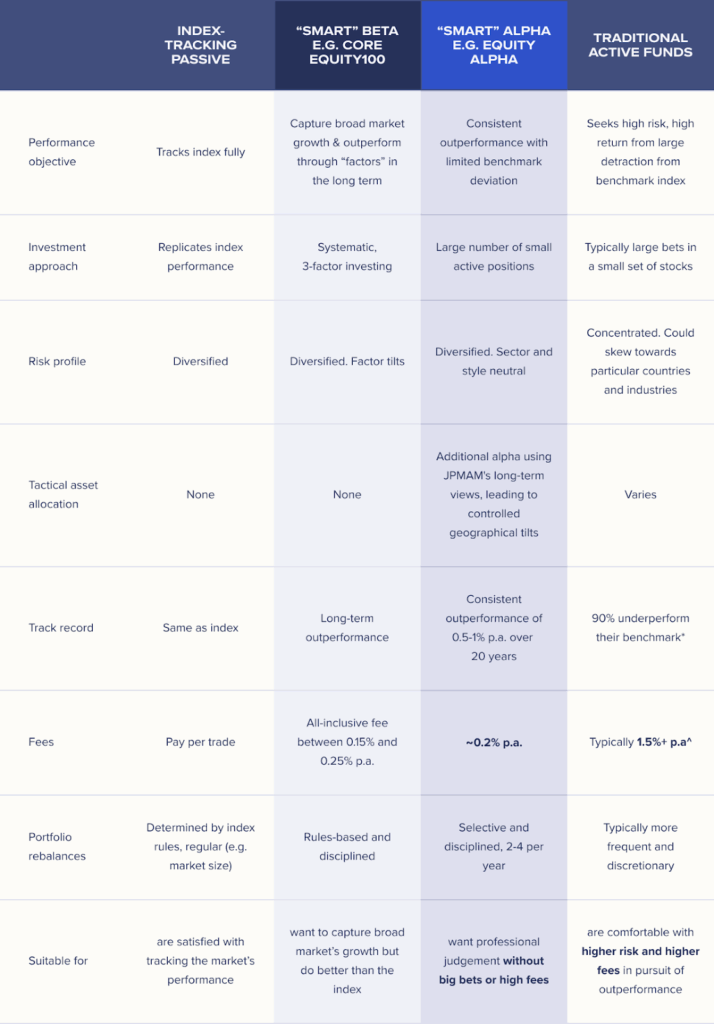

Passive investing’s sole aim is to replicate the performance of a benchmark index, typically a basket of stocks grouped by country, industry, or theme. The S&P 500 tracks the 500 largest publicly traded companies in the US, for example, while the PHLX Semiconductor Sector index (SOX) tracks 30 leading companies in the global chip industry.

Often, passive funds are “market-capitalisation weighting”, meaning the largest companies automatically get the biggest slice of your investment. Sometimes they are “equal-weighted”, meaning every company in the index gets an equal portion of your capital, no matter how big or small they are.

Active investing is the opposite. It seeks to beat the benchmark rather than just mirror it. Instead of buying the entire market based on size, a team of professional portfolio managers and analysts conducts deep fundamental research to take calculated, concentrated bets on a smaller set of stocks that they believe will do significantly better than their peers.

Because active managers intentionally choose not to hold the exact same basket of stocks as the index, their portfolio’s performance will inevitably diverge from the benchmark. This divergence is known as “tracking error.” The ultimate justification for taking on this tracking error is generating “alpha”, which is the excess return achieved above the market benchmark.

Pros and Cons: Things to Consider

Returns Expectations: By simply tracking an index, you remove “decision fatigue” and the stress of trying to time the market. The flip side is that your gains are bounded by the benchmark. Purely passive strategies will not “beat” the market.

Active management offers outperformance over the benchmark. Yet, the odds are famously difficult. Data consistently shows that over a 15-year horizon, roughly 90% of active fund managers underperform their benchmark.

Costs: Passive funds are highly cost-efficient with minuscule fees – often ranging between 0.03% and 0.15%. Active strategies are typically run by one or a couple of experienced – and expensive – portfolio managers. Fees can be in excess of 1.5%.

Diversification and Quality: Active managers seek to weed out the bad apples and pick winners. In doing so, they often focus on a small set of stocks. This cuts both ways – either the bold bets pay off big time, or they could be punishing when the manager misses the mark.

By design, passive index investing offers decent diversification. This is not always the case, however. More recently, the AI-driven rally has made the tech megacaps a big chunk of many investors’ portfolios, making concentration risks more pronounced.

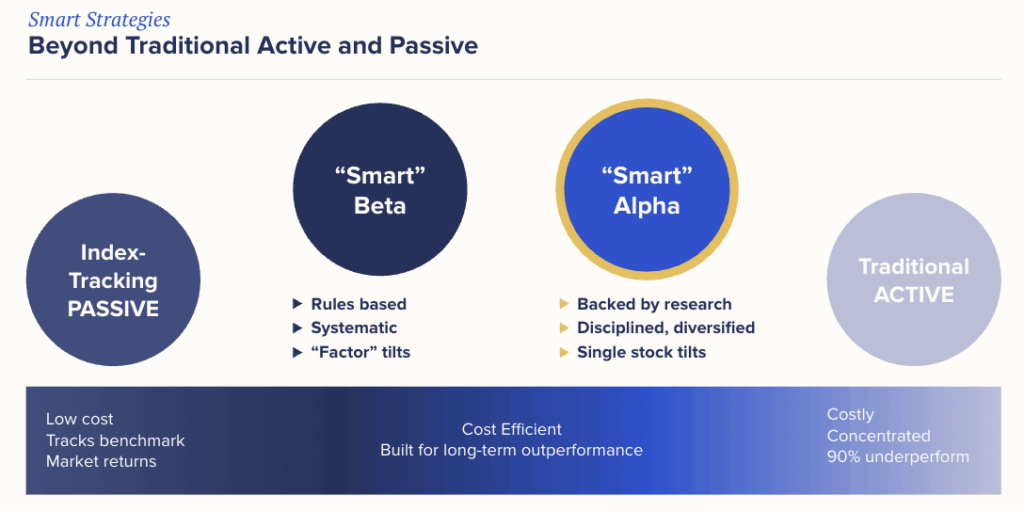

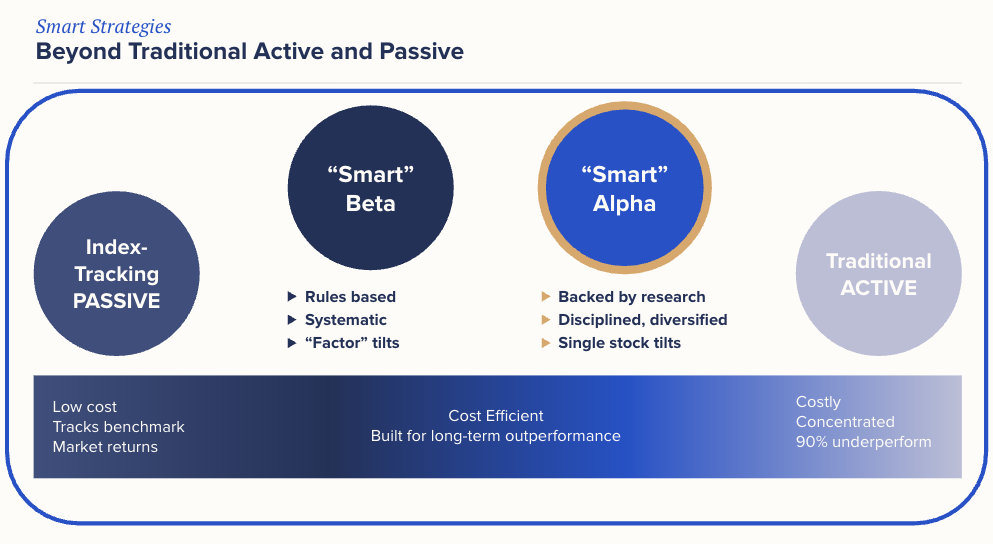

A “Smarter” Way Forward

We believe there are better solutions. There are “smart strategies” that have been able to bridge the gap left between the more rigid traditional approaches, targeting outperformance while keeping costs low. For many years, they were the preserve of large institutions. Syfe has changed that by making them available to individual investors in Asia.

Smart Beta is a transparent, rules-based strategy that selects and weights stocks based on proven performance “factors”, categories that reflect the characteristics of companies, rather than mere market size.

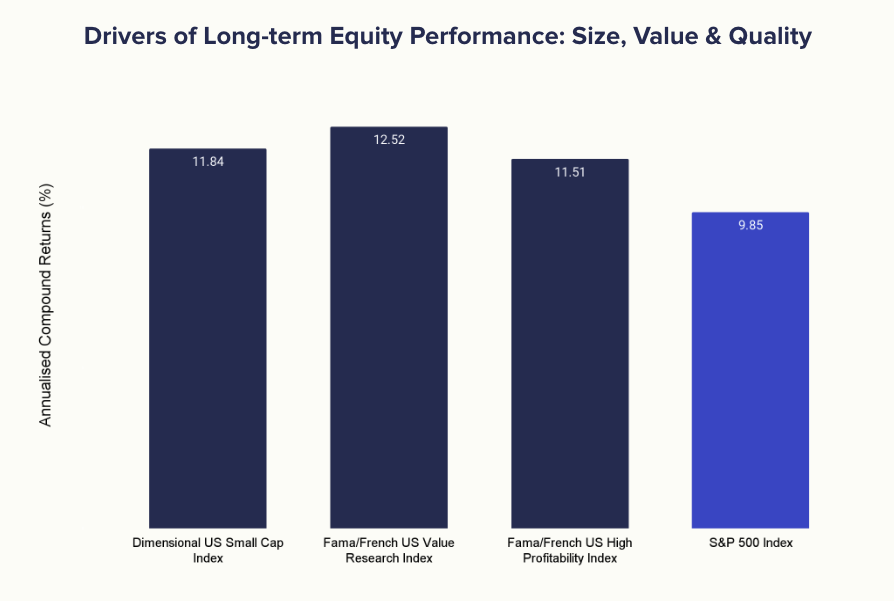

This approach is grounded in academic research. Nobel laureate Eugene Fama and Kenneth French in the 1990s discovered that returns can be explained by three factors: size, value, and market risk. This was later extended to five factors, including quality (or profitability).

Think of traditional passive investing like assembling a sports team regardless of the players’ aptitude, recruiting “star”, average, and poor performers. Smart beta is like using statistics to systematically identify players by their attributes (e.g. pace, distance covered), and focuses on drafting players with traits that will most likely deliver performance over the long term.An example is Syfe’s Core Equity100 portfolio, which uses cost-efficient ETFs to systematically tilt investments towards factors that are expected to outperform. Over the long term, factors-based strategies have a strong performance against the benchmark.

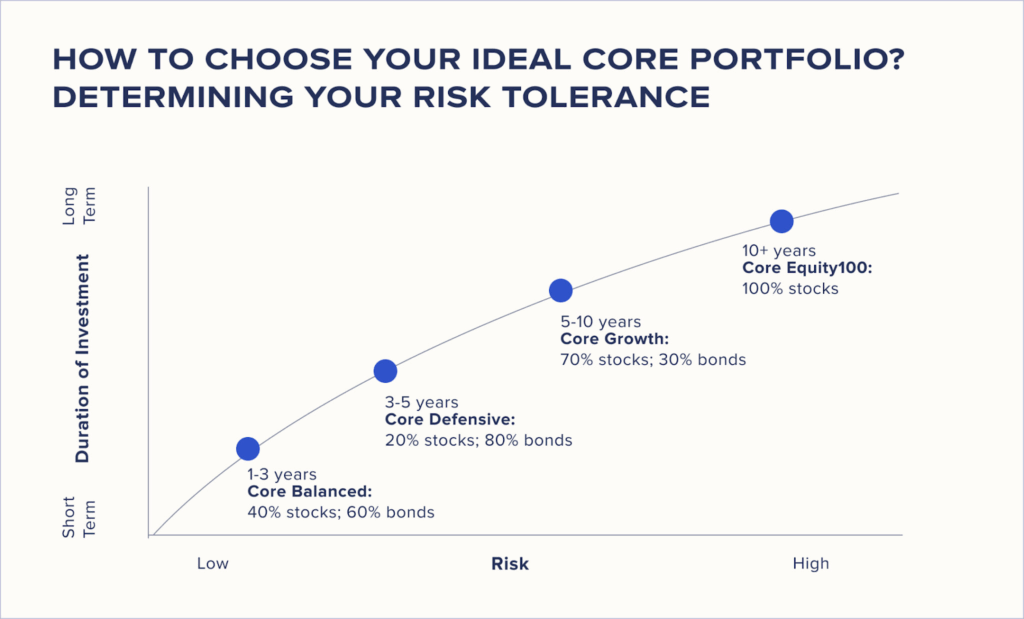

Here, the time horizon matters. A factor that delivers for long-term investors can face challenges near-term, sometimes for several years. Integrating multiple factors would mean that investors are more protected throughout. This is the approach we have taken in our four Core portfolios, which are designed to serve various durations of investment, as well as levels of risk appetite.

Smart Alpha targets excess returns through dynamic, active management rather than rules. It is designed to deliver consistent outperformance through disciplined stock selection. Crucially, this is not traditional active stock-picking. Instead of relying on a few experienced portfolio managers, performance rests on equity research covering a broad set of stocks and a structured ratings system to evaluate these companies. In the case of Equity Alpha, built by Syfe’s investment team and powered by J.P. Morgan Asset Management (JPMAM), the strategy benefits from JPMAM’s equity research team, which is one of the largest and most well-resourced in the industry. This enables Equity Alpha to hold a large number of small stock bets and avoid concentration risks typical in traditional active funds. The cadence and magnitude of changes are disciplined and clearly defined.

Building Your Portfolio on Syfe

Smart strategies do not eliminate the need for all other investment approaches. But they do offer investors choice. Instead of getting stuck between index-trackers that offer no alpha and expensive active managers, many of whom have struggled to beat the market, investors can now add “smart” beta and “smart” alpha to their line-up to drive steady, long-term returns.

For many investors, the “Core” suite on the “passive” half of the scale offers the best foundation to capture broad market gains. For those with a greater risk appetite, they can add “smart” alpha to that mix, strengthening their ability to be selective, which should be supportive of performance in markets with clear “dispersion” between winners and losers. They are mutually complementary, and together, give investors the flexibility they need to build a suitable portfolio.

You must be logged in to post a comment.