(5 min read)

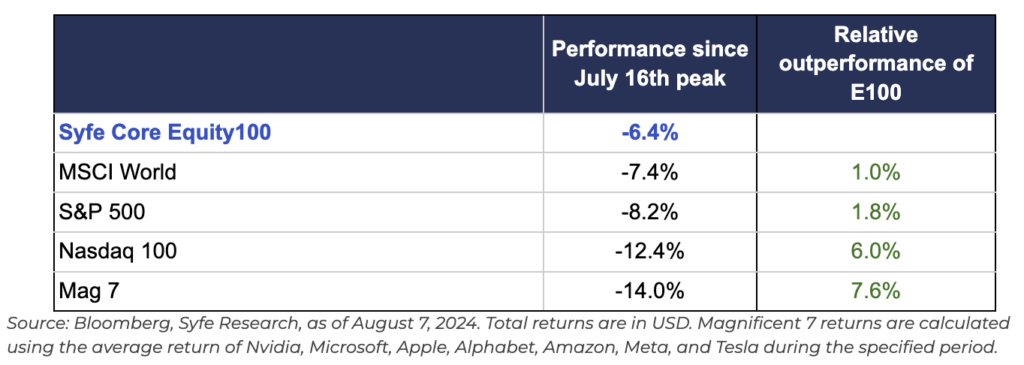

Earlier this week we covered the recent stock market sell-off and the resilience of our managed portfolios. Our Core Equity100 outperformed, slipping 1% less than its MSCI World benchmark and had half the drawdown of the ‘Magnificent Seven’, which plunged 14%.

Today we examine how our Core Equity100 portfolio is set up and what led to this outperformance during a challenging period for the markets. The short answer is a diversified, factor-based approach. The long answer is below… and I promise the car photo will make more sense.

What is a factor, and why should I care?

First let’s consider the various investment options available to us. At one extreme we have passive index funds, which have low fees and track the performance of indices like the S&P 500 and MSCI World.

At the other extreme you could invest in an active fund, where individual stocks are chosen with the aim of outperforming their benchmark (typically the most appropriate index, e.g. MSCI World Index if selecting stocks globally). These have higher fees and can have larger swings in performance. In fact, the vast majority of the time these funds underperform their respective benchmarks.

Factor investing sits in between, but what is a factor I hear you ask… well, a factor is a characteristic that can help explain why certain groups of securities may perform the way they do in terms of risk and return.

The following are examples of factors; value (for under-valued companies), size (companies with smaller market capitalisations) and quality (companies with strong profitability, stable earnings etc.).

Academic research (notably Fama-French) shows that these characteristics explain significant amounts of stock performance over time. One can use factors to seek better risk-adjusted returns than simply following an index or trying to hand-pick stocks.

I find analogies often help, so let’s imagine we’re purchasing a car….

- The passive approach would be to buy the standard model, which will be cost-efficient and gets us from point A to B.

- The active approach would be to heavily modify the car, swapping out most of the parts. Whilst we may get a faster car, it could be more dangerous or we may significantly impact the reliability and long term durability.

- The factor-based approach would be to add a few key upgrades which will most improve the car. We could invest in better tyres, fuel and brakes to enhance our mileage and safety, without sacrificing reliability.

How did this help the core portfolios recently?

When constructing our portfolios we select low-cost ETFs that express a few factors in a diverse manner, which over the long term deliver better risk-adjusted returns. Having a few of these in our portfolio, combined with broader low-cost index ETFs, allows us to cheaply make small, considered, “factor tilts” (i.e. investments into these factors). This helps us to achieve greater risk-adjusted returns whilst not deviating significantly from the market returns.

As we saw at the beginning of this article and in our piece earlier this week, our core portfolios have outperformed during this period of market volatility thanks to our diversified factor exposure.

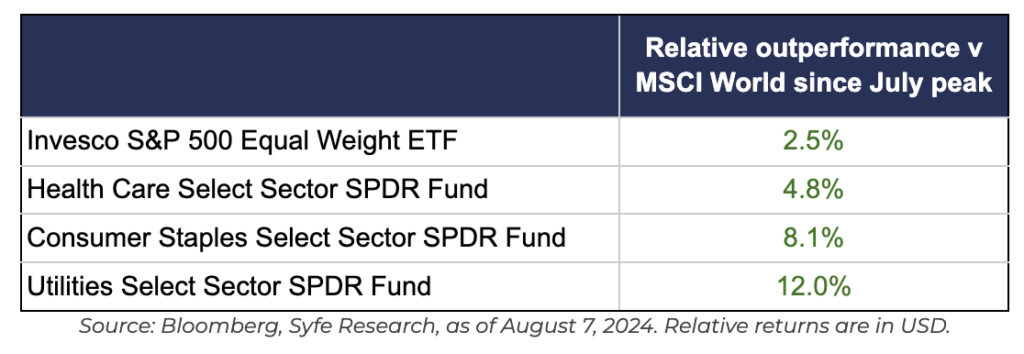

Since we spoke about concentration risk last month, the ‘Magnificent Seven’ have had a challenging time, falling nearly 14% on average from their July peak. At the time we highlighted RSP, Invesco’s equal-weighted S&P 500 ETF, which is essentially an expression of the size factor. This has helped our Core portfolios outperform the broader market indices during the recent market sell-off, with RSP’s drawdown being 3x smaller than the Mag7’s. Similarly, our defensive and value sector allocations contributed to our outperformance as we can see below.

Whilst we can hope to continue timing our articles that well, we would not suggest trying to time the market. This is why we suggest staying calm, in the market, but diversifying and using the sell-off to your advantage.

What’s next?

Exciting enhancements are on the horizon as we refresh our core portfolios in the next couple of months — stay tuned for deeper insights into them.

If there are other topics you would like to hear about or want to see how far we can stretch an analogy let us know at [email protected].

You must be logged in to post a comment.