Thousands of people turn to Google every month to see if now is the time to invest. It’s a good question, too.

The stock market is known for being unpredictable. It can be erratic – going up one day and then reversing course the very next day. We can understand why some investors are wary about wading in, but that shouldn’t mean sitting on the sidelines. Over the long term, the stock market tends to rise, so you might as well get started sooner rather than later.

But what if I invest right before a correction?

One worry that holds investors back is the fear that they might invest right before the market dips. That’s a valid fear. After all, the stock market cannot keep going up indefinitely.

Here’s the truth: If you do happen to invest just before a market correction, your short-term returns will be affected. There’s no avoiding it. But the longer you stay invested, the more likely that your eventual returns will be closer to the long-term average.

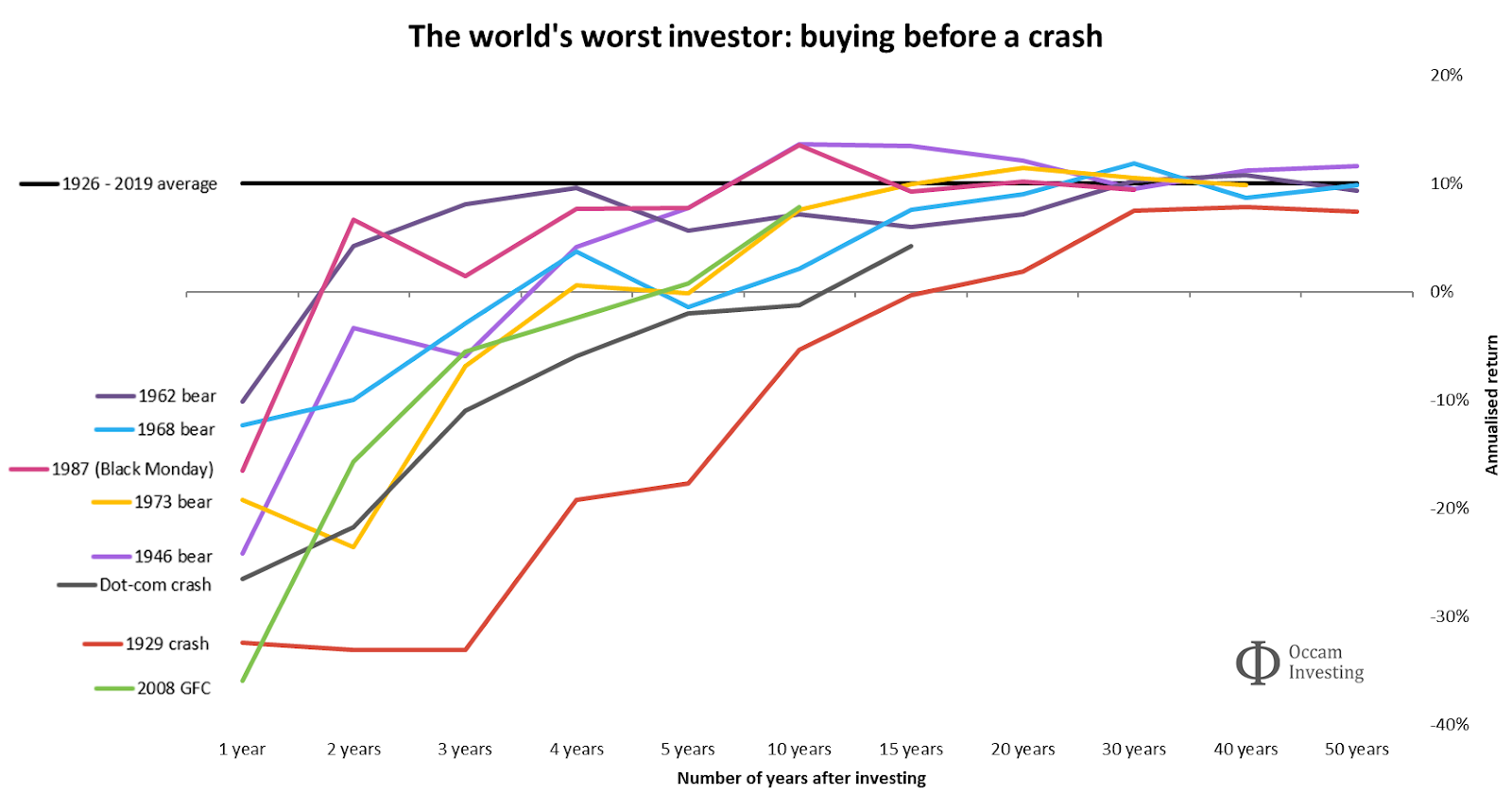

As the chart above shows, even if you were to invest just before these major crashes occurred, your returns prospect improves the longer you stay invested. After about 15 to 20 years, your returns tend to converge on the long-term average return of about 10% annually.

If you are planning for a long term financial goal such as retirement, investing just before the market corrects is still better than not investing at all.

The best strategy to follow

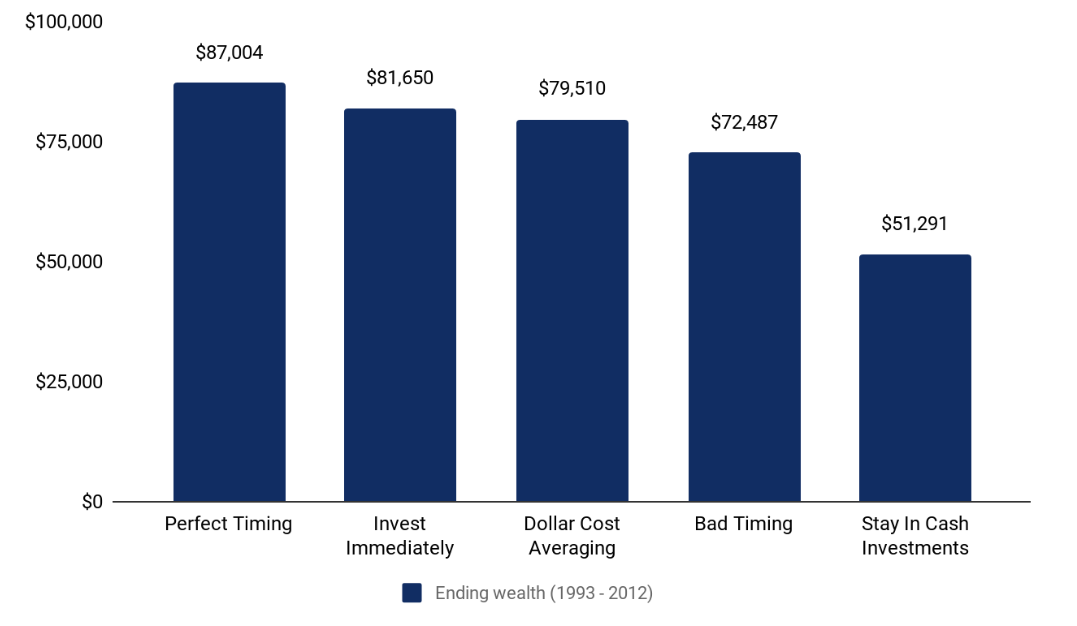

Given the upward trend of the market over time, it makes sense to simply enter the market and stay invested, instead of worrying whether the market is at a high or low point. A study from Charles Schwab highlights this best. It found that procrastination can be worse than bad timing itself.

The study looked at five fictional characters who each received $2,000 every year for 20 years from 1993 to the end of 2012.

- Peter Perfect timed his investments perfectly, always investing when the markets hit their lowest point.

- Ashley Action didn’t time anything. As soon as she received her $2,000, she would invest it immediately.

- Matthew Monthly used a dollar cost averaging strategy. He invested his $2,000 across 12 months, putting his money to work at the beginning of every month.

- Rosie Rotten had terrible luck. She ended up always investing her $2,000 at market all-time highs.

- Larry Linger kept waiting for the perfect moment to invest. Because he always thought a better opportunity would come up, he ended up not investing in stocks at all.

Why you should invest as soon as you can

The results are surprising. Ashley Action invested immediately and did not try to time the market at all. But her performance was comparable to Peter Perfect’s. She ended up with only $5,354 less, even though Peter Perfect was able to invest at all the very best moments.

You would expect Rosie Rotten to fare the worst given that she had such bad marketing timing. Surprisingly not. She ended up with slightly less money than dollar cost averaging Matthew, and significantly more money than Larry Linger, who didn’t invest in stocks but instead bought US Treasury Bills.

The takeaway from this is to invest at the earliest possible moment, no matter what level the market is at.

Timing the market is almost impossible

Nobody, not even professional wealth managers, can consistently identify market bottoms. And even if you do get the timing right each time, the study shows that you won’t be much better off than someone who put her money to work right away, regardless of market highs or lows.

If you are still uncomfortable with the thought of investing a large amount of money when the market is peaking, you can consider dollar cost averaging. You average out the cost of all your investments while eliminating some of the risky guesswork involved in trying to time the market.

Ready to start investing? Achieve your wealth goals with Syfe’s expertly managed, low-cost portfolios.