Stock investors have welcomed Japanese Prime Minister Sanae Takaichi’s decisive re-election this week, with the Nikkei surging to record highs. But her promises on public spending and tax cuts have also put currency and debt markets on edge. Here’s our take on what the “Takaichi Trade” really means – and whether you should partake in it.

What Is the “Takaichi Trade”?

The “Takaichi Trade” refers to a weakening yen, a rising stock market in Japan, and increasing yields (i.e. falling prices) on Japanese government bonds (JGBs), as markets expect more growth-oriented spending from the Sanae Takaichi administration’s “proactive” fiscal policy. It took off late last year when Takaichi campaigned for office, and has returned with her resounding re-election.

Takaichi’s agenda includes temporary consumption tax cuts on food (worth US$32 billion annually), increased defence spending, and investments in semiconductors and artificial intelligence. Analysts at MUFG estimate the tax exemption alone would boost GDP by 0.5%.

Her economic strategy echoes “Abenomics”, championed by Takaichi’s mentor and former prime minister Shinzo Abe in the early 2010s, which gave rise to aggressive monetary easing and helped pull Japan out of deflation.

The difference is that Takaichi’s moment has arrived at a very different point of the economic cycle – as the Bank of Japan (BOJ) “normalises” policy through interest rate hikes, not cuts. She is looking to boost growth through fiscal policy (i.e. public spending and tax cuts) instead.

How Do I Participate in This Trade?

The stock market offers the most straightforward path to play this trade. Investors like political stability. With two-thirds of the seats in the Lower House (a “supermajority”), little can stand in the way of Takaichi’s growth agenda. Janus Henderson notes that after similar victories by the ruling party in 2005 and 2012, the Topix rallied 23% and 31% over 60 days.

Takaichi’s focus on strengthening Japan’s national security means defence and critical resources stocks could rise further, according to analysts at Goldman Sachs. Fidelity International favours construction, financials, and industrials as sectors that could gain from fiscal support and are one step removed from yen volatility or potential US tariffs.

Wisdom Tree tips stocks tied to factory automation and electrical machinery, which continue to benefit from reshoring and the energy transition build-out. Takaichi’s emphasis on technology should also be constructive for semiconductor equipment and components makers, which are tied to the global secular capital spending cycle in chips and AI. Japan is accelerating its AI adoption to offset the demographic drag of an aging population on productivity and has been focusing on the digitisation of its economy for some time.

In Syfe’s Managed Portfolios, Japan is the largest developed market exposure outside of the US. Core Equity100, Core Growth, Core Balanced, and Core Defensive have between 4% to 5% of their allocations in Japan. The latter three are “overweight” on the country, which means they are putting more capital in Japan than their benchmark indices recommend.

Investors can also gain exposure to Japan through Syfe Brokerage, where some of the most widely-tracked Japan ETFs are traded. These include iShares MSCI Japan ETF (EWJ), JPMorgan BetaBuilders Japan ETF (BBJP), and WisdomTree Japan Hedged Equity Fund (DXJ).

What Are the Risks?

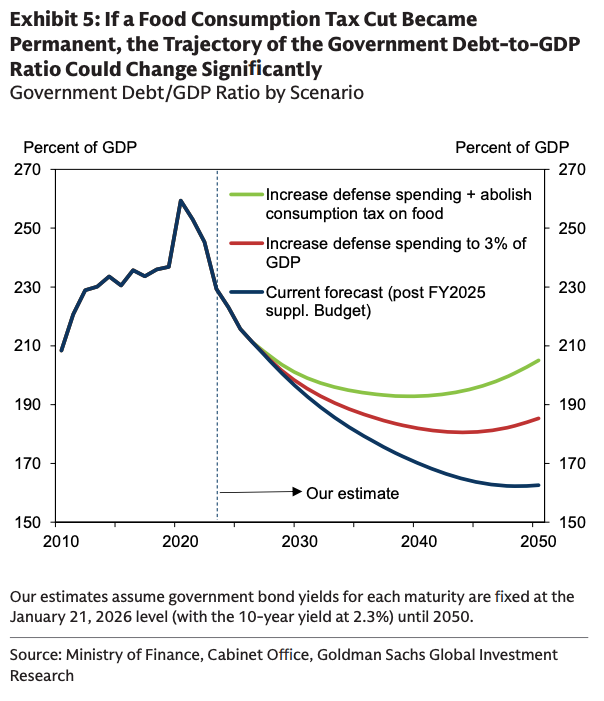

Debt is a clear and present danger. JPMorgan describes the current situation as “fiscal fireworks,” warning that a 237% debt-to-GDP ratio makes Japan the “poster child” for global debt risks. Takaichi’s spending plans have already spooked the bond market, pushing 10-year JGB yields – government borrowing costs – to multi-decade highs before polling day.

Bond markets have since calmed down. But that stability could be fickle. Some analysts worry that tax cuts billed as temporary stimulus measures could end up being permanent, as they are politically difficult to reverse. This could reverse the post-pandemic lowering of Japan’s government debt-to-GDP ratio, albeit still at elevated levels. Bond yields were already trending higher as BOJ tightens policy and phases out bond purchases – a programme created to support markets and shore up growth.

Currency volatility seems to be another hallmark of this trade. A stronger economy should lend strength to the currency, but concerns around debt and Japan’s still-low interest rates have kept the yen weak. Even though the BOJ is now hiking, Japan’s real interest rates (i.e. when accounting for inflation) remain negative and way behind other developed economies, making the yen less attractive for global capital.

Where Could Markets Be Wrong?

As you can see, a lot hinges on the Takaichi administration staying disciplined and responsible while expanding fiscal policy. The bear case, outlined by MUFG, hypothesises profligate public spending spiralling out of control, jacking up interest rates and eroding investor confidence. In that scenario, bonds, equities and yen would fall at the same time.

A more optimistic take by Amova Asset Management suggests Takaichi could surprise to the upside in fiscal discipline. The firm argues that, with such political dominance, Takaichi would actually be less compelled to push for populist measures. The administration would focus on gaining credibility in financial markets.

Is the “Takaichi Trade” right for me?

Patience is paramount in the Takaichi Trade. Near term, there could be more volatility. Many analysts expect more USD/JPY to trade towards 160, at which point the authorities may intervene. That would mean the yen weakening 4.5% from current levels, which would cap gains for global equity investors who have not hedged their foreign exchange exposure.

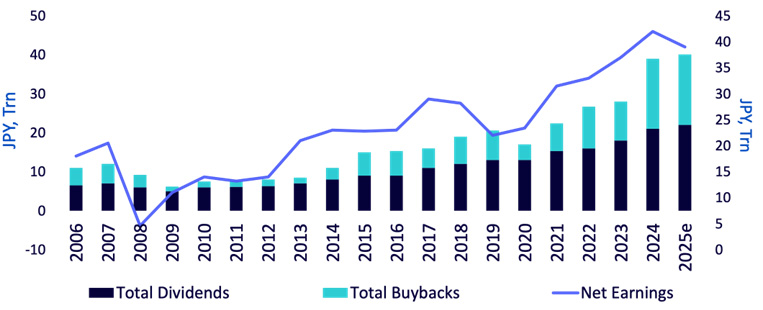

But the stars remain aligned for the market’s long-term growth. The economy has exited the era of deflation, and consumer confidence has begun slowly rising. Corporate governance reforms have progressed steadily, pushing cash-rich companies to return a lot more of that capital to equity investors through buybacks and dividends. Sectors like banks, shunned for years because of negative interest rates, are back into play.

More support could be on the way. Janus Henderson notes that global investors are still “underweight” Japan. More of them could return as Japan’s outlook brightens. At the same time, as Japanese interest rates catch up with major economies, more Japanese capital could also be repatriated.

You must be logged in to post a comment.