Singapore real estate investment trusts (S-REITs) rebounded impressively in the third quarter of 2025, extending the recovery trend seen earlier in the year. The iEdge S-REIT Leaders Index delivered a total return of +8.95% in Q3 2025, reflecting robust price gains coupled with steady dividends. This outpaced most other local asset classes and outperformed the STI in September, delivering 1.93% versus the STI’s 1.32%. This underscores S-REITs’ appeal as high-yield instruments amid stabilising interest rates.

By the end of September, all but two S-REITs—Acrophyte Hospitality Trust (XZL) and Digital Core REIT (DCRU)—were in the black for the quarter, with 43.5% of S-REITs achieving double-digit percentage gains. This strong performance came as investors grew confident that the US Federal Reserve was done with its interest rate peak, as the Fed cut by 0.25% at its FOMC meeting in September. The expectation of easing monetary policy has been a key catalyst lifting S-REIT prices, given their interest-rate sensitivity.

Fundamentally, S-REIT operational metrics remained healthy. Occupancy rates stayed high across most property segments (95%–99% for prime assets) and rental reversions were generally positive, meaning REITs could renew leases at higher rents in sectors like retail and logistics. For example, retail REITs enjoyed improved tenant sales and could negotiate higher rents, while industrial and logistics REITs benefited from resilient demand for warehouse and data centre space.

S-REITs maintained manageable borrowing costs and attractive valuations, with average yields of 5.34% and a wide spread over government bonds, drawing renewed investor interest as confidence and rate expectations improved.

Singapore’s Safe Haven Asset Class Shines

The third quarter saw a favourable macro backdrop for S-REITs.

Globally, inflation eased and monetary policy turned towards rate cuts, with the US Federal Reserve trimming rates by 25 bps and several other central banks following suit. Even where rates held steady, major banks like the ECB and BOE adopted a more dovish tone.

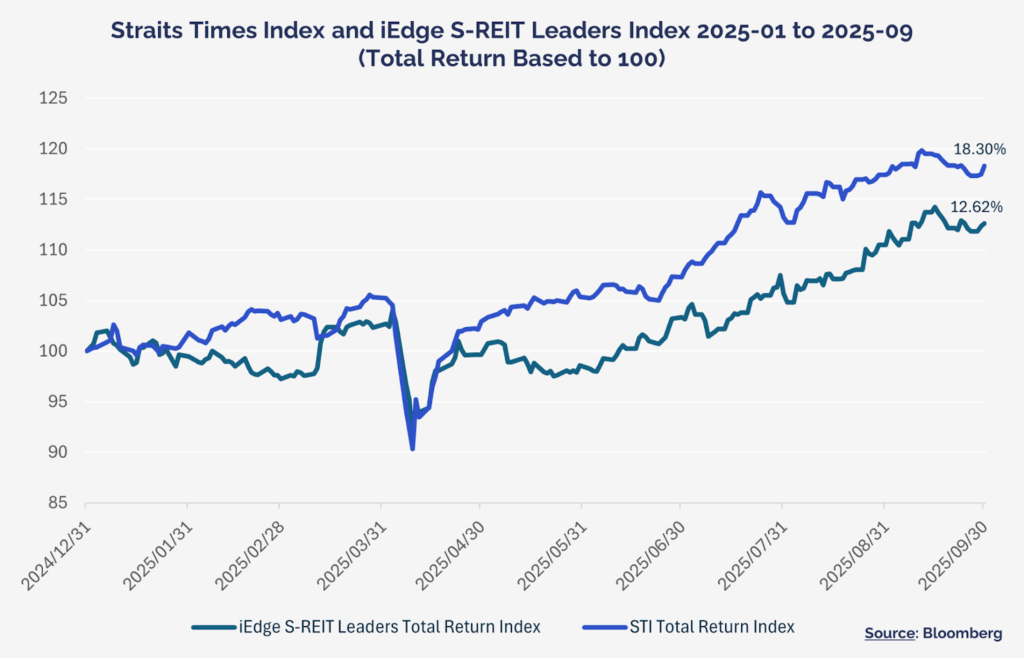

In Singapore, modest economic growth, rising tourism, and stronger retail sales supported REIT performance, while easing rate pressures lifted sentiment. Local bond yields and interbank rates stabilised, benefiting yield-sensitive sectors. The iEdge S-REIT Leaders Index rose +7.38% in Q3 (+8.95% total return), keeping pace with the Straits Times Index’s +10.23% total return.

Year-to-date, S-REITs gained +12.62% versus the STI’s +18.30%, marking a solid rebound and renewed investor confidence after earlier weakness.

| Index | Q1 2025Total Return | Q2 2025Total Return | Q3 2025 Total Return | YTD 2025Total Return |

| iEdge S-REIT Leaders Index | 2.32% | 1.01% | 8.95% | 12.62% |

| Straits Times Index (STI) | 5.33% | 1.89% | 10.23% | 18.30% |

| Source: Bloomberg | ||||

Outlook for Q4: The Tailwinds Align for Sustained Outperformance

The outlook for S-REITs in the coming quarter remains broadly positive but not without risks.

Market consensus expects that major central banks will hold or even begin cutting rates further in late 2025 or early 2026 if inflation continues to moderate. Such a scenario would be a further tailwind for S-REITs, likely compressing yield spreads and boosting REIT prices further as financing costs fall.

In Singapore, the Monetary Authority (MAS) has kept monetary settings stable, resulting in domestic interest benchmarks like SORA easing from ~3% at the start of the year to around ~1.75% for a 6-month benchmark at the end of Q3. Lower interest expense growth in 2026 would directly enhance REITs’ distributable income and could spur higher distribution per unit (DPU) growth. Additionally, the Singapore government has reinforced its support for the REIT sector, extending key tax concessions for S-REITs and REIT ETFs, thus cementing Singapore’s status as a global REIT hub and providing long-term certainty for investors and managers.

That said, if inflation surprises on the upside or if global growth falters (for instance, due to geopolitical tensions or a sharper China slowdown), interest rates might stay elevated longer, tempering the bullish case.

Overall, however, S-REITs appear to be entering Q4 with strong momentum, underpinned by solid fundamentals, supportive government policies, and the prospect of a more accommodative interest rate cycle. Barring any major shocks, S-REITs are poised to finish 2025 on a firm note, continuing to deliver the superior returns that investors enjoyed in Q3 (but likely not at the same strong increase level).

S-REITs Sub-Sector Trends: From Commercial to Residential

Every REIT sub-sector in Singapore ended Q3 with a market capitalisation weighted positive total return, but there was notable dispersion in performance.

| Sector | Q3 2025 Total Return | Weighted Yield | Drivers |

| Office | 18.06% | 4.40% | Flight-to-quality dynamics favoured Grade-A CBD assets as tenants prioritised premium locations and specifications. Singapore properties outperformed offshore portfolios, supported by the city-state’s role as a regional business hub and limited new supply. |

| Diversified | 12.06% | 5.65% | Portfolio diversification across property types proved its worth, allowing REITs to leverage retail strength to offset office weakness and vice versa. Singapore-focused assets with prime locations captured resilient domestic demand across multiple sectors. |

| Residential | 8.33% | 7.47% | Structural demand for worker accommodation driven by Singapore’s infrastructure boom and tight supply regulations supported occupancy. Student housing benefited from international student growth and persistent bed shortages. |

| Industrial | 6.80% | 6.08% | E-commerce growth, supply chain resilience initiatives, and digital transformation drove sustained demand across logistics, and business parks. Modern, well-specified assets in strategic locations commanded premium rents, while Singapore’s limited industrial supply supported positive reversions. |

| Hospitality | 6.62% | 5.72% | International visitor arrivals up year-on-year, with Singapore recording 11.6 million visitors in the first eight months of 2025. Revenue Per Available Room (RevPAR) growth of 4% driven by both higher average daily rate (ADR) and 91.5% occupancy rates demonstrated sector recovery strength. |

| Retail | 5.80% | 5.37% | Suburban malls anchored by necessity trades delivered exceptional performance and higher rental reversions. Limited new supply in Singapore combined with robust domestic consumption created favourable dynamics. Prime Orchard Road assets benefited from tourism recovery and luxury retail expansion. |

| Healthcare | 3.71% | 4.49% | Aging demographics and rising healthcare expenditure provided structural tailwinds, with master lease structures ensuring stable, predictable cash flows. Singapore’s medical tourism strength and Japan’s super-aged population created sustained demand for quality healthcare infrastructure. |

| Data Centre | 2.59% | 3.83% | The mission-critical nature of assets supported high occupancies and long-term lease contracts with creditworthy technology tenants. Trends in cloud adoption, AI applications, and digital transformation drove continued demand. Strong institutional inflows signalled conviction in the sector’s prospects. |

| Source: Bloomberg |

Syfe’s REIT+ Portfolio: The Smart Way to Own S-REITs

Syfe’s REIT+ remains a portfolio that provides investors with a low-cost way to own a basket of Singapore’s top REITs. The portfolio tracks the SGX iEdge S-REIT Leaders Index (consisting of the 20 largest S-REITs), offering broad exposure to the sector.

In Q3 2025, the Syfe REIT+ portfolio enjoyed strong gains in line with the market, and it delivered +9.16% total return for the quarter, reflecting the rebound in the underlying index. Year-to-date, as of end Q3, the portfolio’s return stands around +13.84%, a solid recovery from the previous year’s decline.

The estimated dividend yield of REIT+ is ~5.44% (based on 2025 projections), paid quarterly through the distributions of constituent REITs, an attractive income stream for investors. The portfolio automatically reinvests dividends (if one chooses the growth option) or pays them out (in the income option), making it flexible for different investor needs.

Syfe REIT+ Q4 Outlook

The REIT+ portfolio, being a mirror of the broader S-REIT market, is positioned to continue benefiting from the trends discussed. Its heavy weightings in large-cap REITs mean it is tilted towards high-quality properties (Grade A offices, prime malls, top logistics facilities, etc) and strong sponsors (CapitaLand, Mapletree, Keppel, Frasers), which provides a measure of safety should markets turn choppy. It currently offers a ~5-6% average yield, and is set to remain attractive, especially as interest rates continue to decline.

Looking into Q4 2025, the key drivers for REIT+ performance will be macro: if bond yields pull back on confirmed rate cuts, the index’s heavyweights (which are interest-rate sensitive) could rally further.

However, the portfolio is not immune to global economic downturns. Also, as an index tracker, REIT+ will include some underperformers along with winners. However, the overall health of the S-REIT sector is robust, and with the supportive policy environment in Singapore the long-term prospects remain positive.

Syfe’s REIT+ portfolio offers a well-balanced way to ride the S-REIT sector’s recovery. Investors can expect continued steady dividends and participation in any capital upside as the S-REIT rally progresses, while trusting that the diversification will mitigate shocks along the way.

Read More:

- Why S-REITs Could Be Poised for a Bounceback in 2025

- How to Pick Resilient REITs in Singapore’s Property Market Recovery

- Singapore Office REITs: Why Prime Office Assets Remain a Compelling Investment in 2025

- What’s Driving the Growth in Singapore Retail REITs in 2025

- Why Healthcare S-REITs Are a Hidden Gem for Defensive Investors

You must be logged in to post a comment.