After holding steady through most of 2025, the Fed signalled a potential rate cut in the coming months. Here’s how this will impact the Singaporean investor.

When the US Federal Reserve makes a move, the world takes notice. That’s because US interest rates—the Fed funds rate—influence everything from the cost of mortgages in Singapore to the performance of Asian stock markets.

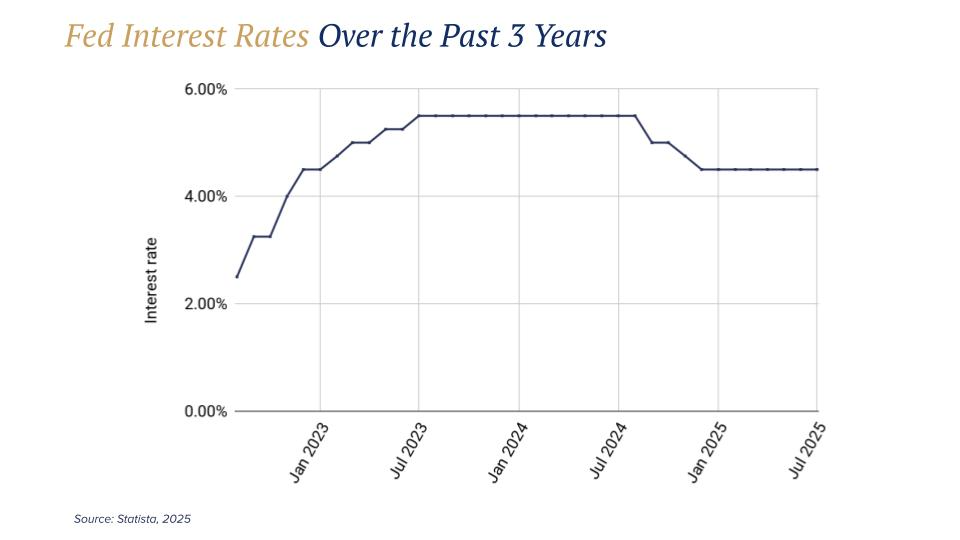

After holding steady through most of 2025, the Fed signalled a shift in September when Chair Jerome Powell suggested that rate cuts could be on the table, especially if labour market data continues to soften. This follows several rounds of cuts in late 2024, which buoyed markets but did little to revive momentum in early 2025.

Now, all eyes are on the August US jobs report due 5 September 2025. A weak July payrolls print—just 73,000 jobs added—already set the stage for easing. Economists expect another modest gain of 75,000 in August. Markets see this as near-certain confirmation that the Fed will cut rates at its 16–17 September meeting, with futures pricing an 89.7% chance of a 25-basis-point cut (at the time of publishing).

But the key question for Singapore investors remains: What does a US rate cut mean for my money?

Understanding Fed Rates—and Why They Matter

The Fed funds rate is the short-term interest rate US banks charge each other for overnight loans. It might sound remote, but because the US dollar is the world’s reserve currency, this benchmark influences global borrowing costs, investment flows, and risk sentiment.

Think of it as the tide:

- When rates rise, the tide goes out—borrowing gets more expensive, money leaves riskier markets, and economies slow down.

- When rates fall, the tide comes in—credit is cheaper, investors take on more risk, and growth often picks up.

Singapore’s central bank, the Monetary Authority of Singapore (MAS), doesn’t set interest rates directly. Instead, it manages the Singapore dollar against a basket of currencies. Still, because Singapore is an open economy and global financial hub, US rate decisions quickly filter into our local mortgage rates, bond yields, and investment returns.

What Drives Fed Decisions?

The Fed has two main goals:

- To keep prices stable (inflation).

- To support maximum employment (jobs).

Several key factors determine when it cuts or raises rates:

1. Inflation

If prices rise too quickly, the Fed raises rates to cool demand. If inflation falls too low, rate cuts encourage spending. For Singaporeans, US inflation matters because it drives global interest rates. A high-inflation US tends to mean higher mortgage and loan rates here.

2. Labour Market

The health of US employment influences Fed policy directly. A strong jobs market suggests the economy can handle higher rates. Weak payroll growth signals trouble, prompting the Fed to cut. When the US job market slows, global markets often wobble at first, but lower rates can provide support.

3. Economic Growth (GDP)

If the US economy expands strongly, the Fed can keep rates high. If growth slows or recession risks rise, cuts are more likely. Slower US growth often drags on Asian exports, including Singapore’s, so Fed support can be a stabilising force.

4. Financial Stability

The Fed monitors credit markets, stock valuations, and liquidity. If financial conditions tighten too much, rate cuts aim to ease the strain. Singapore’s markets, being globally integrated, feel these shifts quickly.

5. Global Factors

Geopolitical risks, trade tensions, or capital flows also impact Fed decisions. For instance, if investors pull money out of emerging markets during global stress, Fed easing can help stem the outflow. Singapore, as a safe and open market, often attracts inflows during such times.

In general, markets can be volatile in the short term, but lower interest rates generally support both the economy and stock markets. Even if economic data shows some weakness, rate cuts tend to provide a stabilising effect.

How Fed Rate Cuts Affect Singaporeans

Here’s a closer look at how lower US interest rates will influence the financial landscape in Singapore:

| Borrowing costs and mortgages | Lower borrowing costs and cheaper mortgages |

| Property market | Demand for homes will rise but price may not |

| Savings and deposits | Rates and returns will fall |

| T-Bills and Singapore Savings Bonds (SSBs) | Yields will decline |

| Investments and markets | Equities, bond prices, and REITs will rise |

1. Borrowing Costs and Mortgages

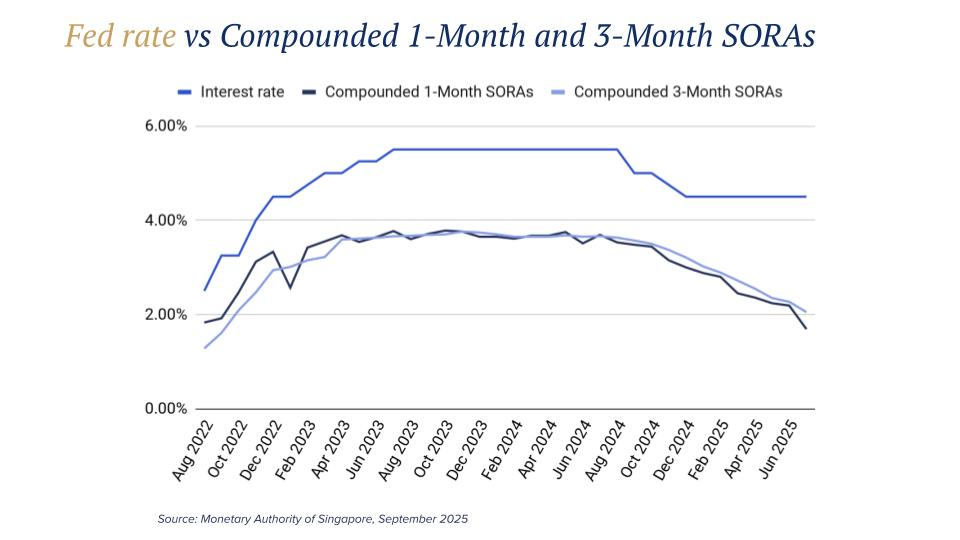

When US rates fall, borrowing costs in Singapore usually decline as well. That’s because local banks use benchmarks like SORA (Singapore Overnight Rate Average), which tend to move in tandem with global interest rates.

- Floating-rate mortgages: These usually get cheaper when rates are cut, lowering monthly repayments. For example, a homeowner with a $1 million loan might save hundreds of dollars each month if rates fall by just 0.5–1%.

- Fixed-rate mortgages: These offer stability. While they don’t adjust down when rates fall, they protect you if rates unexpectedly rise again. In fact, fixed packages sometimes become more attractive in uncertain times.

What this means for you:

- If you’re a homeowner, consider whether refinancing makes sense.

- If you’re planning to buy property, lower rates can make affordability easier—but don’t forget the TDSR (55% cap on debt vs income) and MSR (30% cap for HDB loans) still limit how much you can borrow.

2. Property Market

Lower borrowing costs often boost demand for homes, especially in the private market. Buyers can afford bigger loans, and investors may be tempted by property as an asset class.

But this doesn’t mean prices will automatically soar. Singapore’s property market is tightly regulated with cooling measures like Additional Buyer’s Stamp Duty (ABSD). Demand may rise, but policymakers can step in to prevent overheating.

What this means for you:

- If you’re a genuine homeowner, rate cuts make mortgages more manageable.

- If you’re an investor, weigh the long-term rental demand and holding costs, not just cheap financing.

3. Savings and Deposits

For savers, rate cuts are a mixed bag.

- Bank savings accounts: Interest rates typically fall, meaning less passive income.

- Fixed deposits (FDs): The generous campaigns we saw in 2023–2024 are unlikely to return in a low-rate world.

What this means for you:

If you’ve relied on FDs or saving accounts for stable returns, you’ll need to consider alternatives to preserve and grow your money.

4. T-Bills and Singapore Savings Bonds

Singapore government securities like Treasury Bills (T-Bills) and Singapore Savings Bonds (SSBs) are often seen as safe havens. But when global interest rates fall, their yields usually decline too.

- T-Bills: Useful for short-term cash parking, but rates can be volatile, and funds are locked up for the tenor.

- SSBs: Backed by the government and offer step-up interest over 10 years, but redeeming them early isn’t instant and requires advance notice.

For those seeking stability and liquidity, Syfe’s Cash+ Flexi can be a compelling alternative. It invests in short-term cash management funds like LionGlobal SGD Enhanced Liquidity Fund SGD, offering competitive yields that often outpace traditional savings accounts, T-Bills, or even SSBs. Most importantly, it allows fast withdrawals, making it both safe and flexible.

What this means for you: If you want your money to work harder than in a savings account while staying liquid, Cash+ Flexi provides a practical solution. It combines stability, higher returns, and instant access, something neither T-Bills nor SSBs can fully offer.

5. Investments and Markets

For investors, rate cuts usually act as a tailwind. Lower rates support equities, bonds, and REITs. Here’s how:

- Stocks: Cheaper financing helps businesses expand. Investors also tend to shift money from low-yielding bonds into stocks, lifting valuations.

- Bonds: When rates fall, bond prices rise. Investment-grade bonds become more attractive for income-seeking investors.

- REITs: Lower rates reduce borrowing costs for REITs and increase their appeal relative to deposits. Singapore REITs, in particular, often benefit in such cycles.

- Asian markets: Lower U.S. yields can push more capital into Asia, boosting regional equities.

What this means for you:

Stay diversified. Income-generating assets like REITs and dividend stocks shine in low-rate environments, but balance them with quality global equities for growth.

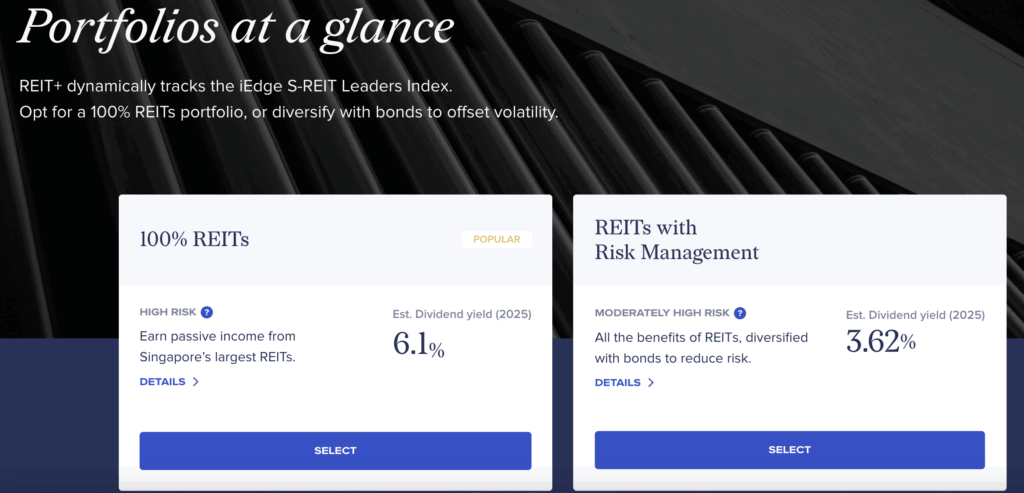

Ride the tailwinds of rate cuts with Syfe REIT+, a professionally managed portfolio that tracks the iEdge S-REITs Leaders Index and comprises the top 20 SGD-denominated S-REITs. They are also optimised based on liquidity and market cap, and dividends are automatically reinvested.

Conclusion

A Fed rate cut ripples across the globe and directly into your wallet. For Singaporeans, the smartest move isn’t to time each Fed decision, but to stay diversified, review your portfolio regularly, and align your money with long-term goals. With the right mix of strategies, you can turn a changing rate environment into an opportunity to build lasting wealth.

Read More:

Why S-REITs Could Be Poised for a Bounceback in 2025

What History Reveals About Interest Rate Cuts

A New Chapter in Interest Rates – What Does This Mean for You?

You must be logged in to post a comment.