Singapore’s retail REITs have proven to be among the more resilient segments within the broader REIT sector.

By early 2025, high shopper footfall, recovering tenant sales, and positive rental reversions are now the norm across well-managed portfolios. Suburban malls, anchored in necessity trades like groceries, healthcare, and Food and Beverage (F&B) led the recovery, with some even exceeding pre-Covid revenue metrics.

Prime malls have also regained momentum, buoyed by international tourism and luxury brand expansion. Occupancy rates are now typically north of 96%, and mall operators are again achieving mid- to high-single-digit rent uplifts on lease renewals, clear signs of restored landlord pricing power.

Corporate Moves Reshape the REIT Landscape

The past three years have been transformative.

An important event is Paragon REIT’s delisting. Driven by a sponsor-led privatisation offer, it reflects the sponsor’s conviction in the long-term value of Orchard Road retail. Paragon is expected to be delisted around 6 June 2025. In contrast, Frasers Centrepoint Trust has deepened its suburban dominance through the 2023 S$652 million acquisition of NEX.

However, while quality REITs are pulling ahead, the weaker ones are lagging. Lippo Malls and Dasin Retail Trust, both exposed to overseas risk, FX pressures, and weak sponsors, have halted distributions and face uphill battles to regain credibility.

Performance Divergence: Stable Core, Fragile Fringe

Domestic-focused REITs like Frasers Centrepoint Trust (FCT), CapitaLand Integrated Commercial Trust (CICT) and Starhill Global (STHL) boast high occupancy, stable gearing, and yields in the 5–6% range. They’ve also delivered positive rental reversions, especially in high-traffic malls.

In contrast, offshore-heavy peers, particularly those in China and Indonesia, have seen capital erosion, DPU cuts, and persistent valuation discounts. Sector gearing stays below limits, with most players refinancing and hedging. Sasseur REIT stands out for its outlet-mall model and low gearing.

Strategic Positioning in a Shifting Retail Landscape

The threat from e-commerce remains real but manageable. Singapore’s retail REITs have responded by re-tenanting towards experience-led, service-oriented offerings, supporting omnichannel models, and investing in tenant sales productivity. Asset enhancement initiatives (AEIs), such as FCT’s rejuvenation of Hougang Mall, are being pursued with IRR discipline and yield accretive intent.

Meanwhile, the limited pipeline of new retail supply continues to support landlord pricing power. Green credentials and ESG alignment are also increasingly differentiating top-tier REITs, with green financing and certified buildings becoming the norm among market leaders.

2025 Outlook: Stability with Selective Upside

The retail REIT sub-sector is expected to generate stable mid-single-digit total returns in 2025. Interest rate pressures are easing, lending support to both valuations and DPUs. Cap rate compression may remain limited, but improving net income growth, driven by occupancy and rental uplift, should offset it.

Investors seeking predictable income and capital growth will find opportunities in Singapore-centric retail REITs with scale, sponsor support, and defensively positioned assets. Conversely, the overseas cohort remains a higher-risk proposition, with foreign exchange, governance, and structural headwinds yet to fully resolve.

Overview of the Singapore Retail REIT Sub-Sector

Market Size and Growth Trends

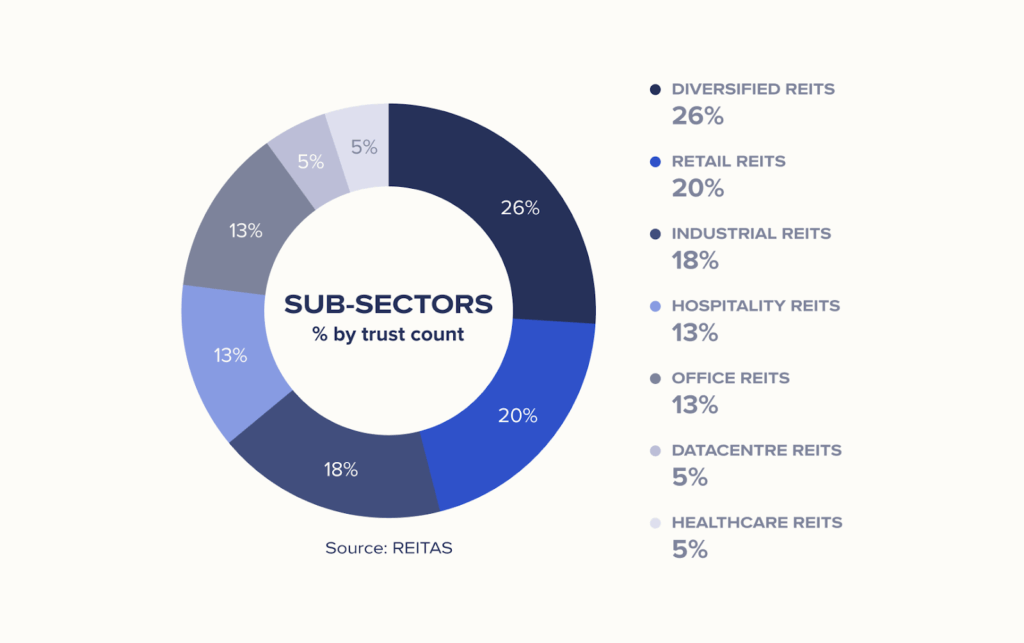

Retail REITs form a significant sub-sector of Singapore’s S-REIT market. According to the REITAS, the market comprises 41 REITs and has a total market capitalisation above S$100 billion. Within this, retail-focused REITs account for a substantial share, led by heavyweights like CICT and FCT. These retail REITs collectively own dozens of malls in Singapore (and overseas in some cases), valued at well over S$30 billion in aggregate.

The sub-sector’s growth trajectory was disrupted in 2020 by the pandemic but has since resumed on a moderate upward path. After a sharp contraction in 2020 (when mall traffic plummeted during lockdowns), retail REIT gross revenues and distributions have grown steadily through 2021–2024, driven by the reopening boost and pent-up consumer demand.

| Company | Ticker | Market Cap (SGD) |

| CapitaLand Integrated Commercial Trust | L0A | 15.3B |

| Frasers Centrepoint Trust | J69U | 4.6B |

| Starhill Global Real Estate Investment Trust | P40U | 1.1B |

| Sasseur Real Estate Investment Trust | CRPU | 0.8B |

| United Hampshire US REIT | ODBU | 0.3B |

Source: SGX, Syfe Research, as of 29 May 2025

By FY2024, many retail REITs saw rental income back at or above pre-pandemic levels. FCT, for example, reported a +35% YoY surge in tenant sales in 2022 and expanded its portfolio with larger stakes in Waterway Point and NEX mall.

New retail supply in Singapore has been limited, and with demand recovering, this has supported high occupancies and modest rental growth.

Overall, from 2022 to 2025 the retail REIT sub-sector has transitioned from recovery to modest growth, underpinned by resilient consumption trends.

Key Drivers of Performance

- Domestic Consumption and Tourism

Retail REITs benefited from strong consumer spending and a tourism rebound. Suburban malls enjoy steady local footfall, while downtown malls have seen rising rents from renewed tourist flows. For example, Paragon REIT maintained near-full occupancy (99.6%) in 2024, thanks to both locals and tourists.

- E-commerce and Omni-Channel Adaptation

E-commerce penetration in Singapore remains modest (~6–8%), so malls still anchor daily essentials and experiences. REITs have adapted by curating F&B, entertainment, and omni-channel services, keeping malls relevant as community and lifestyle hubs. Suburban malls, in particular, enjoy resilient cash flow from necessity-based tenants, supporting stable distributions.

- Asset Enhancement and Management (AEIs)

Active management continues to drive returns. Many retail REITs have undertaken AEIs to refresh and reposition malls, thereby attracting new tenants and higher rents. Examples include FCT’s S$51m Hougang Mall revamp (targeting 7% ROI) and CICT’s +10.4% rental reversion in 1Q 2025. Such initiatives keep malls competitive and support rental growth.

Comparison With Other REIT Sub-Sectors

Compared to office and industrial REITs, retail REITs have shown a surprisingly robust recovery. Office REITs continue to grapple with hybrid work headwinds—even prime offices have seen flat or modestly declining effective rents as tenants continue to right-size.

Industrial/logistics REITs enjoyed strong growth during the e-commerce boom of 2020–2021, but their rent growth moderated by 2024 as supply caught up and economic conditions softened.

While not as high-growth as logistics or data centers, retail REITs remain resilient with stable rents and mid-range yields (~6–7%). Supported by proactive management, Singapore’s retail REITs avoided the severe disruptions seen in overseas counterparts, reinforcing their relative stability.

Future Outlook

The outlook for retail REITs is cautiously optimistic. Occupancy is expected to remain high given limited new mall supply and steady tenant demand.

Rental growth should be modestly positive in 2025, with suburban malls supported by stable local spending, and prime malls benefiting from tourism recovery and luxury brand expansion. However, the post-pandemic rebound is tapering, and retail sales are forecast to grow only in the low single digits. E-commerce’s gradual rise may also cap upside for some categories.

On balance, analysts anticipate stable to improving DPUs in 2025. Stabilising interest costs will ease a major drag, and some REITs could see growth if refinancing at lower rates occurs.

The retail REIT sub-sector’s future looks stable with mid-single-digit total returns achievable, underpinned by high occupancies, slight rental upticks, and improving financing conditions. Risks around the macroeconomy and consumer sentiment remain (detailed later in the Risk While macroeconomic and consumer sentiment risks remain, Singapore’s retail REITs are well-positioned to deliver steady income and modest growth.

Capture this growth with Syfe’s REIT+ portfolio, which comprises the top 20 SGD-denominated S-REITs and tracks the iEdge S-REIT Leaders Index.

You must be logged in to post a comment.