Assets typically seen as “safe” in a crisis – bonds, gold, and the yen – are all falling as the Iran War rattles markets, and just as investors need them most. We explain why this is happening and explore how investors can build resilience in their portfolios right now.

Table of Contents

- What are safe havens?

- How is this time different?

- Why exactly are safe havens not holding up?

- A Word on Income: Anchoring Performance

- Where could markets be wrong?

- What can I do now?

What are safe havens?

Safe havens are assets that are expected to hold their value or even appreciate when the broader market sells off. They are typically liquid (i.e. actively traded) and often tied to countries that are seen as stable. Examples include US Treasuries (i.e. government bonds), the Japanese yen, and the Swiss franc. Gold, a store of value for millennia, is the ultimate poster child.

Even in living memory, we have witnessed plenty of flights to safety. US Treasuries rallied at the outset of the Global Financial Crisis, and again at the outbreak of the Covid-19 pandemic. Gold’s multi-year rally was, arguably, sparked by the war in Ukraine and the geopolitical tensions that followed. The Swiss franc jumped against the euro at the start of that war.

How is this time different?

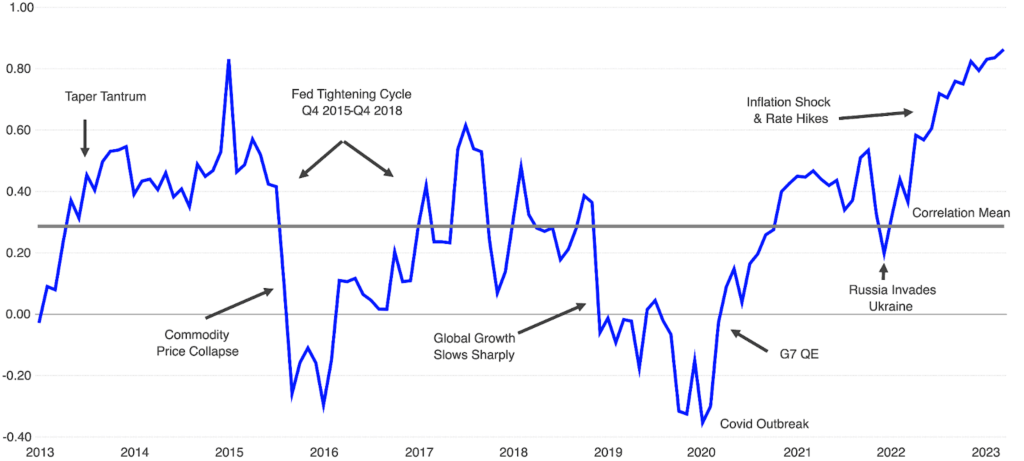

For the past four decades, many major crises followed the same script: growth collapsed, deflation loomed, central banks cut rates, and bonds rallied. Investors were accustomed to worrying first and foremost about demand destruction. This is not the case when supply disruptions dominate. An example would be 2022, when supply chain chaos sparked by the pandemic was compounded by the energy shock from the Ukraine War. In that case, bonds and stocks moved in the same direction, meaning bonds didn’t offer protection (see chart below).

A similar “supply shock” is unfolding now with the Iran War, which has caused the largest oil supply shock in recorded history. The Strait of Hormuz, through which 20% of global oil and liquified natural gas (LNG) supply normally transits, is effectively shut. Surging oil prices are already giving pause to those central banks about to cut interest rates. A protracted conflict could tilt them towards hiking. Some analysts fear the return of 1970s-style “stagflation”, with low growth, high inflation, and punitive financing costs all at the same time.

Source: LSEG. Chart shows the correlation of returns between FTSE Global All-World Index and FTSE World Government Bond Index.

Why exactly are safe havens not holding up?

A couple of weeks into the Iran war, traditional safe haven assets have diverged. Bonds and gold have dropped, while the US dollar has rallied hard.

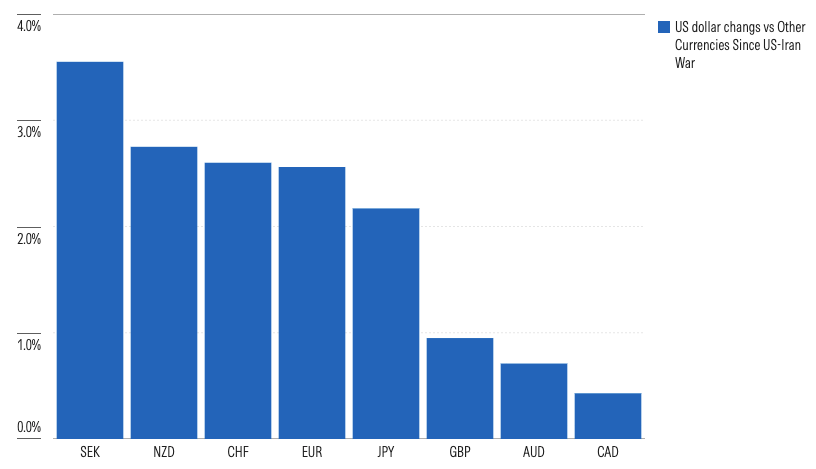

Currency markets are increasingly shaped by how dependent countries are on oil. US energy independence has proven to be a source of resilience. The dollar is also benefitting from shifting interest rate expectations, as markets now see the Fed keeping rates higher for longer.

Compare that with the yen, which has historically been a reliable haven. Its large trade surplus and vast overseas investment holdings mean that a lot of capital typically flows back to the Japanese currency during a crisis. That protection looks less convincing now that we have an oil crisis, with Japan being a big net oil importer.

The currencies of Australia and Canada, which are net energy exporters, have held up better in the face of dollar strength, as shown in the chart below.

Source: Compiled by Morningstar based on Macrobond data, 17 March 2026.

Gold does not generate income, so when rates rise (or stay higher than markets had expected), bullion looks less attractive relative to bonds and cash. Given that gold has been a crowded trade (following an outstanding 80% rally over two years), some unwinding in a falling market is likely. In sharp sell-offs, leveraged investors are sometimes forced to liquidate positions to meet margin calls.

Because gold is priced in US dollars, a surging greenback also makes the yellow metal more expensive for non-USD buyers, dampening global demand and pushing prices down.

Bonds face a double whammy. At the short end of the US Treasury yield curve, traders are pushing up rates as they expect central banks to prioritise the fight against inflation (which they primarily do by raising near-term interest rates) over supporting growth. Bond’s prices and their yields have an inverse relationship: the lower the price, the higher the yield.

Long-dated bonds are faring not much better because markets see governments having to borrow and spend more in the long run, especially if the war drags on and inflicts lasting damage on the global economy. That means the risk for holding long-term bonds is rising, and bondholders want to be compensated for that.

A Word on Income: Anchoring Performance

The recent rout in fixed income can be unsettling, but it only presents half the picture. Total return in fixed income includes both capital appreciation and the coupons that are paid periodically to bondholders. These payments flow regardless of how much the underlying assets swing between now and their maturity date, serving as an anchor to portfolio performance.

With bonds selling off, their yields are also becoming more attractive. The average yield in Bloomberg’s Global Aggregate Treasuries Total Return Index climbed to almost 3.5% this week, the highest level since May 2024.

Syfe’s Income+ managed portfolios (“Preserve” and “Enhanced”) continued to provide investors with steady income, generating payouts between 5% and 6%. Their returns, down about 2% to 3%, have been impacted by the market sell-off, but are not far off the performance of global bonds (Bloomberg Global Agg, FX hedged, is down about 2%) and are stronger than multi-asset portfolios (Morningstar’s 60/40 equity/bond index -5%).

Our 100% REITs offering, likewise sensitive to interest rates, is also yielding 5.6%. Fundamentals remain strong, with an earnings upgrade cycle unfolding in the S-REIT sector.

Where could markets be wrong?

Markets could be overestimating how high interest rates will rise. The economic fallout is less widespread now than in 2022, when a world reeling from the pandemic confronted both an energy crisis and supply chain disruptions. Right now, the crisis is mostly about energy.

Another point to note is that interest rates are already relatively high. This means, unlike a few years ago, central banks may have less room to hike because financial conditions become “restrictive” i.e. more than is needed to rein in price rises. Ramping up interest rates could risk triggering a recession.

Capital could move just as quickly in the other direction. Markets tend to rebound from conflicts once there’s a path to peace, even without a full resolution. That’s why wars generally have a short-lived impact on markets. Rate-sensitive assets could rally once that happens.

What can I do now?

- Cash: Hold enough of it. Cash provides “liquidity” and flexibility, allowing you to preserve capital in a crisis, meet short-term spending needs, and accumulate ammunition to deploy when you see undervalued assets.

Too much cash, however, would mean you’re forfeiting on income – because there are higher-yielding opportunities in fixed income assets like bonds and REITs. Strike a balance. Hold enough cash during a crisis, but stand ready to pivot. - Stay disciplined, stay diversified. Finally, don’t catch the falling knife. Investors have been instinctively “buying the dip” in the broad tech-driven rally of the past few years. As we previously warned, those days are gone. The investors who fare best in more challenging markets are those who stay invested and diversified across asset classes, positioning themselves for the eventual recovery.

- Review your portfolio. Volatile markets provide a reality check. Are your investment objectives really in line with your allocation? Do you have the risk appetite to stomach drawdowns and wait for the eventual rebound? Is your time horizon long enough to ride out the downturn, and do you need more cash out in the near-term?

These questions help determine if you can sleep well at night. For those answering yes, staying invested and “dollar cost averaging” is usually a pretty good strategy. If you have any questions or need assistance, please feel free to reach out to our Investment Advisory team.

You must be logged in to post a comment.