You’ve seen the headlines—trade tariffs from the Trump administration are back in focus, Elon Musk’s latest DOGE-related plans are making waves, and global markets are reacting to renewed policy uncertainty. Meanwhile, investors are feeling the heat. From the peak, the S&P 500 is down -6.6%, and the Nasdaq 100 has dropped -9.6% (as of March 6, 2025).

If you’re feeling uneasy about your portfolio, you’re not alone. Market pullbacks often trigger anxiety, making investors wonder: Is this the start of a major crash? Should I sell now and sit on cash? But before making any hasty decisions, let’s take a step back, put things into perspective, and focus on what you can control.

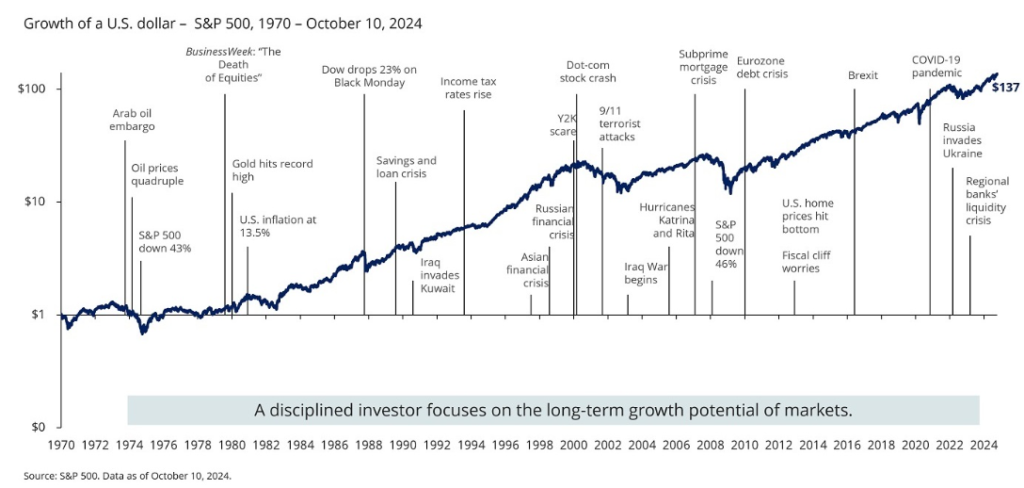

Lessons from History: Market Sell-Offs Are Normal (and Temporary)

Stock market corrections happen more often than we think—they’re simply a natural part of equity investing. Think of it like learning surfing: just as waves are inevitable in the ocean, market fluctuations are part of the investing journey. The key is learning to ride them rather than staying out of the water.

Historically, the S&P 500 experiences an average intra-year pullback of -16%. Yet, despite all the crises, recessions, and financial shocks over the decades, the market has always recovered and moved higher in the long run. Consider a few major market downturns over last two decades:

- Dot-com Bubble (1999) – Tech stocks crashed, but those who remained patient eventually saw the sector thrive again.

- 2008 Global Financial Crisis – Markets plunged, but those who stayed invested saw a strong recovery.

- 2020 COVID-19 Crash – Stocks dropped nearly 35% in weeks, only to rebound to new highs within months.

The key takeaway? Every major market selloff feels like the worst when you’re in it, but history favors those who stay the course.

Source: Source: S&P 500, 10 October, 2024.

How to Prepare for a Market Crash (Instead of Reacting to One)

While we can’t predict whether the current sell-off will spiral into a major crash (which is not our base-case scenario) or when the next market downturn will occur, we can take steps to strengthen our personal finances and better withstand volatility.

Here’s a three-step guide to staying prepared.

- Strengthen your financial position

If a market crash happens tomorrow, would you be forced to sell your investments to cover expenses? If the answer is yes, it’s time to increase your allocation to an emergency fund. Having 6–12 months’ worth of living expenses in cash ensures you won’t need to liquidate investments during turbulent times.

A side note: Your emergency fund doesn’t have to sit idle. Consider Syfe Cash+, which offers significantly higher returns, latest yield of 4.2% p.a., than a regular bank account while maintaining liquidity.

Additionally, it’s a good time to review your leverage. Investing with borrowed money can amplify gains, but it can just as easily wipe out your portfolio in a downturn. Ensuring you’re not overleveraged can help you navigate market volatility with confidence.

- Understand your psychological response to risk

Beyond financial capacity, emotional capacity is just as crucial for long-term investing success.

One of best-selling personal finance books, The Psychology of Money by Morgan Housel, highlights an important truth: our experiences with money—shaped by our upbringing, personal history, and career stability—differ widely. As a result, we all react to risk in different ways.

It’s important to be honest about how much risk you can truly handle. Many investors believe they are risk-tolerant when markets are soaring, only to panic when a downturn hits. The best portfolio isn’t the one with the highest returns—it’s the one you can stick with through all market cycles.

Take a moment to ask yourself:

- If the equity market drops 20% in a month, will I lose sleep?

- Can I resist the urge to sell if headlines scream “Stock Market Crash!”?

- Do I truly believe in my investment strategy, or am I just following trends?

If you find yourself second-guessing your investments every time the market dips, it may be time to reassess your asset allocation and build a portfolio that you can hold with confidence—no matter the headlines.

At Syfe, we offer portfolios tailored to investors with different risk preferences.

If you prefer to reduce risk in your portfolio, consider increasing allocation to:

- Income+ – Bond and Multi-asset income portfolios with an average investment-grade rating and attractive distribution yields (6.0% – 8.6% p.a.). Despite recent volatility in the bond market, Income+ portfolios have demonstrated great resilience, with the Income+ Pure gaining +2.1% and Income+ Enhance gaining +2.3% this year (as of 28-Feb).

- Cash+ Fixed HKD – Earn up to 3.9% p.a. fixed returns on your idle cash across 1, 3 or 6-month time deposits with leading banks in Hong Kong

- Cash+ Flexi USD – Money market fund based portfolio, with daily liquidity and no lock-up, with latest yield of 4.2% p.a. in USD.

3. Have a clear game plan

One of the biggest mistakes investors make during a downturn is freezing up. Without a clear plan, fear takes over, often leading to impulsive decisions that can hurt long-term returns. Instead, it’s crucial to establish clear rules for how you’ll respond to market drops.

A simple yet proven strategy to navigate volatility is Dollar-Cost Averaging (DCA)—investing a fixed amount at regular intervals (e.g., monthly) to smooth out market fluctuations.

Even if the starting point isn’t ideal, DCA can still generate strong returns over time. For example, consider an investor who invests US$2,000 per month into global equities for 12 months and then holds for two years.

To illustrate this, we purposefully chose 2018, when global equities fell -7.5%, and 2022, when global equities dropped -18.9%, as starting points. Despite these challenging entry years, DCA still proved to be an effective investment strategy.

The Power of Dollar-Cost Averaging: Investing Through Market Downturns

| Start DCA Year | 2018 | 2022 |

| DCA Period | Jan – Dec 2018 | Jan – Dec 2022 |

| Monthly Investment ($) | 2,000 | 2,000 |

| Total Invested Amount ($) | 24,000 | 24,000 |

| Portfolio Value After 2 Years ($) | 31,411 | 32,825 |

| Simple Return (%) | 30.9% | 36.8% |

Source: Syfe Research, calculated based on the MSCI All Country World Index. Currency in USD. For illustrative purposes only.

If you don’t have a plan yet, now is the time to set one up. For example, you can easily set up recurring transfers into Core Equity100 with just a single click in the APP.

Final Thought: Prepare, Don’t Predict

No one can predict when the next market crash will happen, and frankly, it doesn’t matter. What truly matters is how well you’re prepared to handle it. The next time the market takes a hit and fear starts creeping in, remember: market corrections are normal and temporary, your financial habits—such as savings and risk management—matter more than trying to time the market, and having a solid plan helps you stay rational instead of making emotional decisions. So, take a deep breath, stick to your strategy, and trust that history rewards patient investors.

Read More:

This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone.Past returns are not a guarantee for future performance. Investors should consider his/her own circumstances. The information or advertisement contained herein does not constitute an offer, any solicitation, invitation or recommendation to engage in any investment activities.

")