From Boom to Caution: The Q3 Market Review

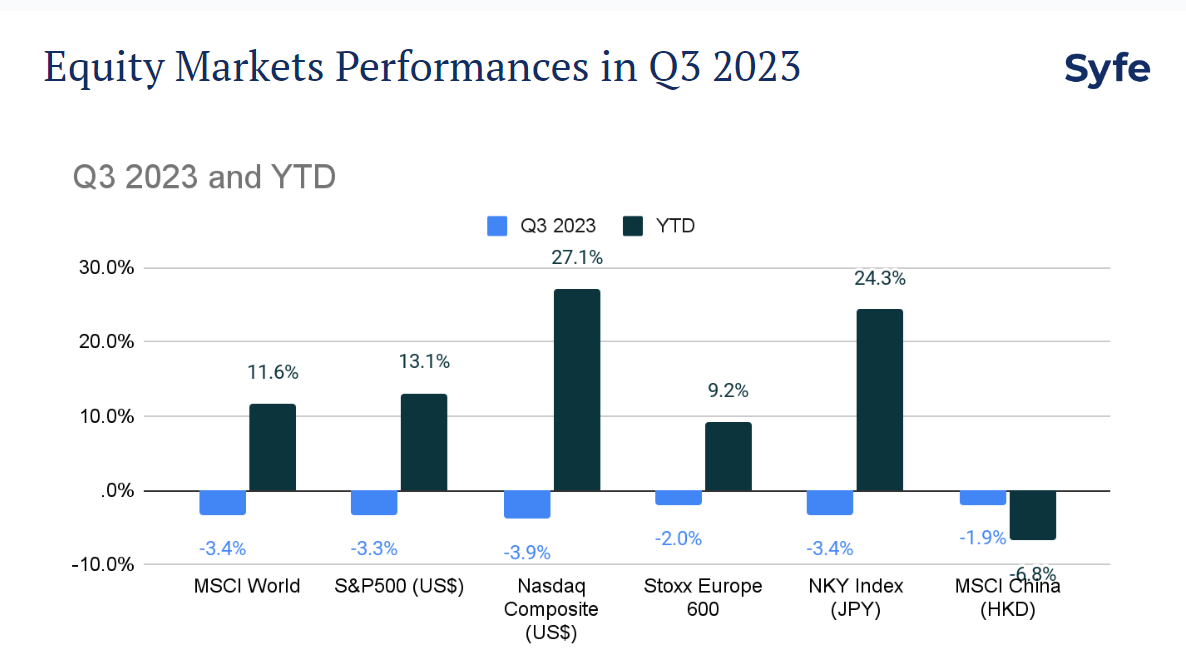

Following a stellar performance in the first half of the year, Q3 painted a different picture. Global stocks faced headwinds, with MSCI World index marking a 3.4% decrease. Notably, the US equity arena bore the brunt, with the tech-centric Nasdaq Composite Index experiencing the steepest pullback at 3.9% for the quarter. However, its year-to-date performance remains robust at 27.1%. In an intriguing twist, despite abundant media attention on its real estate, China’s stock market declined by 1.9% in Q3, outperforming global equities, but it stands as the most underperforming equity market for the year so far.

Navigating the fixed income territory in recent times has been challenging, especially with US treasuries and investment-grade bonds witnessing fluctuations across a range of quality and tenures. High-yield bonds stood firm in Q3, reflecting the resilience of the US economy in the quarter.

Has China’s market bottomed out?

China has been a major concern for investors in the third quarter. The initial post-reopening optimism has been rapidly replaced by pessimism, with the highly leveraged property market and local government at the epicentre of this crisis. Evergrande, one of the largest property companies, has filed for bankruptcy, while leading home builder Country Garden teeters on the brink of default.

This has prompted many to question: Is China experiencing its own version of the “Lehman Brothers moment”? The temptation to equate China’s property turmoil to the 2008 financial meltdown is strong. However, our analysis suggests caution in drawing such direct parallels. The backbone of China’s financial ecosystem – its major banks – are state-owned. Most of its debt remains domestically anchored with limited foreign borrowings. The Chinese government has also learnt from its previous periods of capital flight, and now appear to have put more effective control in place.

Even though the property market continues to be a drag on the economy, there are initial signs that China’s economy is stabilising, especially in the consumer sector. Retail sales accelerated to 4.6% in August, up from 2.5% in July, primarily fueled by service consumption such as tourism.

Fed’s stance: Higher for Longer

In our H2 outlook, we highlighted that the Fed would likely hit the brakes post-June hike. Our stance remains unchanged; we believe the Federal Reserve’s hiking cycle might have reached its end for now. This perspective is anchored in two main observations:

Inflationary Trends: Major economies have witnessed a downtrend in inflation, a trend consistently seen into Q3. While core inflation remains more sticky than headline inflation, the inflection point has been reached.

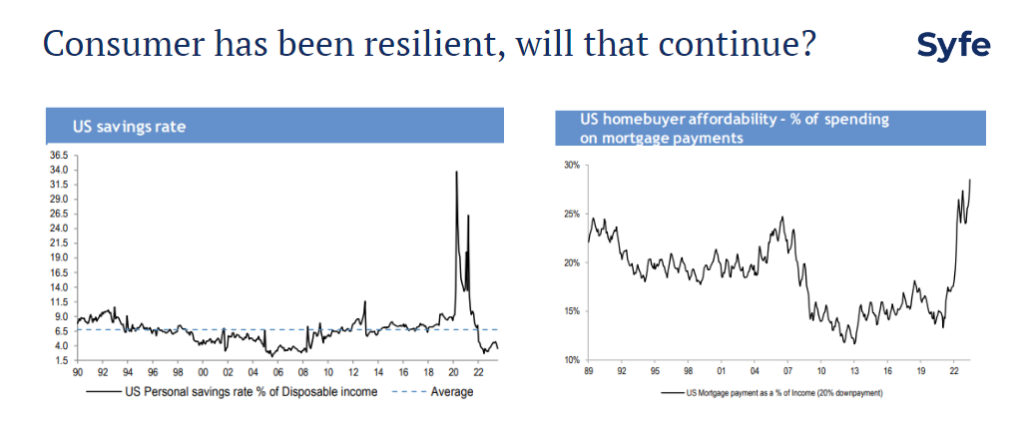

Economic Vulnerabilities: US consumption has been resilient in Q3, complemented by encouraging employment figures. Yet, there are some concerns looming in the near future. The savings rate hovers near a decade-low. With potential resumption in student loan repayments, younger demographics may find their disposable incomes strained. This is further exacerbated by the multi-year peak in mortgage rates.

Given the potential pitfalls and economic repercussions of further hikes, we are inclined to think the Fed might hold its horses, erring on the side of caution to avert any risk of tipping the economy into recession.

Regarding the anticipated rate cut, our view aligns with the market consensus: rates may stay “higher for longer,” meaning that the Fed could maintain the rates at their current level for an extended period and start cutting them later than initially anticipated. The first rate cut is likely deferred to H2 2024 as guided by the Fed in the September FOMC meeting. The Fed, wary of the stubborn nature of core inflation, might hesitate to ease monetary policy too soon – lest it inadvertently fuels an inflationary resurgence.

Brace for volatility in the short-term

Our base case assumes that the Fed have completed its rate hikes, but we are cognizant of the possibility that the Fed could proceed with another hike. Currently, the CME FedWatch Tool suggests the market is pricing in a 64% probability of no rate hike by December 2023. If the Fed decides to raise rates in their November or December meetings, it could surprise the markets, leading to significant volatility and short-term drawdowns. Key dates to note for the FOMC meeting are on 1st November and 13th December. We anticipate heightened market activity around these dates.

Nevertheless, in a more hawkish scenario, it is highly probable that the Fed will hike just once more, marking the end of this hiking cycle. The likelihood of the Fed raising rates twice or more is minimal. When taking a longer-term perspective, such as over the next 12 months, history suggests that both equities and bonds generally perform well in the 12 months following the final Fed rate hike, especially if a recession is averted.

Implications on asset classes if the Fed pause

A delve into the previous four hiking cycles (1995, 2000, 2006, and 2018) reveals a positive trajectory for major asset classes. Evidently, a plateau in policy rates often signals a boost in risk appetite. The reason? The recession typically has not happened during this period. For the past four cycles, only once did a recession trail within twelve months of the last rate hike. Among equities, US stocks typically stand out, boasting an average surge of 20% post the Fed rate pause.. On the bonds front, Emerging Market bonds and US investment grade bonds are the front-runners in returns.

It is also interesting to note that bonds offer a strong risk-return tradeoff when the Fed stops hiking rates. Delving deeper into the last seven cycles since 1984, bonds have consistently posted positive returns. Whether one observes a short-term horizon of 6 months or extends to 1-year, 3-year, or even a 5-year timeframe, the performance of bonds has remained consistently in the green for all these cycles. This consistent performance not only underscores the resilience of bonds during such periods but also suggests their potential role as a stabilising factor in investment portfolios, especially when central bank policies stops hiking rates.

Summary

Amid the turbulence witnessed in Q3, it is common for investors to feel apprehensive, but it is crucial to lean on historical insights and adopt a broader perspective. Past instances remind us that in most cycles, equities and bonds both tend to do well after the Federal Reserve takes a breather from rate hikes. Short-term market fluctuations, rather than deter, can present savvy investors with opportunities to build up their positions for the longer term.

But it is also important to recognise that every cycle could be different. Fed’s “Higher for longer” guidance may lead to some short-term volatility. It is in these moments of market ambiguity, the value of a diversified portfolio, spanning cash, equities, and bonds, becomes even more important. By holding your ground and anticipating the rate pivot, you set the stage to seize the forthcoming opportunities.

You must be logged in to post a comment.