Markets were in a tailspin earlier this week after Kevin Warsh, an inflation hawk, was nominated to lead the Federal Reserve. But the views of the incoming Fed chair are more nuanced than the market reaction suggests. Here’s why – and what it means for your portfolio.

I missed the action. What made markets so volatile?

On January 30, US President Donald Trump nominated Kevin Warsh as the next Federal Reserve Chair, precipitating seismic moves across asset classes. The markets had expected someone more dovish to get the job, given the Administration’s preference for lower financing costs.

For Janus Henderson, the nomination represents “one of the most consequential” Fed chair appointments in over a decade. Appointing Warsh, an inflation hawk, signals a potential departure from the largely accommodative monetary policy framework that has characterised Fed policy since the Global Financial Crisis in 2008.

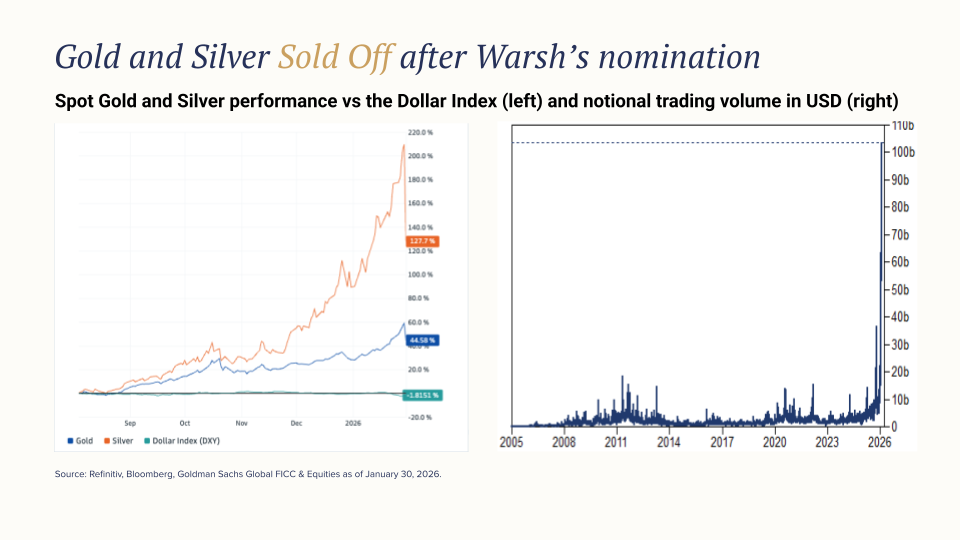

The most dramatic reaction was in precious metals. Gold shed over a tenth of its value intraday, while silver fell more than 30% – magnitudes not seen in decades. The US dollar strengthened. This represented a sharp unwinding of the “debasement” trade, the idea that investors have been diversifying away from the dollar to avoid policy risks and stretched valuations.

Simultaneously, the bond market signalled a “bear steepening” i.e. short-term interest rates remained anchored while long-term yields ticked higher. Investors fear that Warsh’s known dislike for the Fed’s massive balance sheet could lead to aggressive quantitative tightening (i.e. selling bonds), pushing long-term borrowing costs up. But the steady short-term rates indicate that, at least in the near future, markets still expect interest rates to fall.

Remind me: What does the Fed do and how does it impact markets?

The Federal Reserve manages monetary policy through two mechanisms.

Interest rates: The Fed sets the federal funds rate, influencing borrowing costs across the economy. Lower rates encourage investment and spending while supporting asset prices. Higher rates cool economic activity and often pressure valuations.

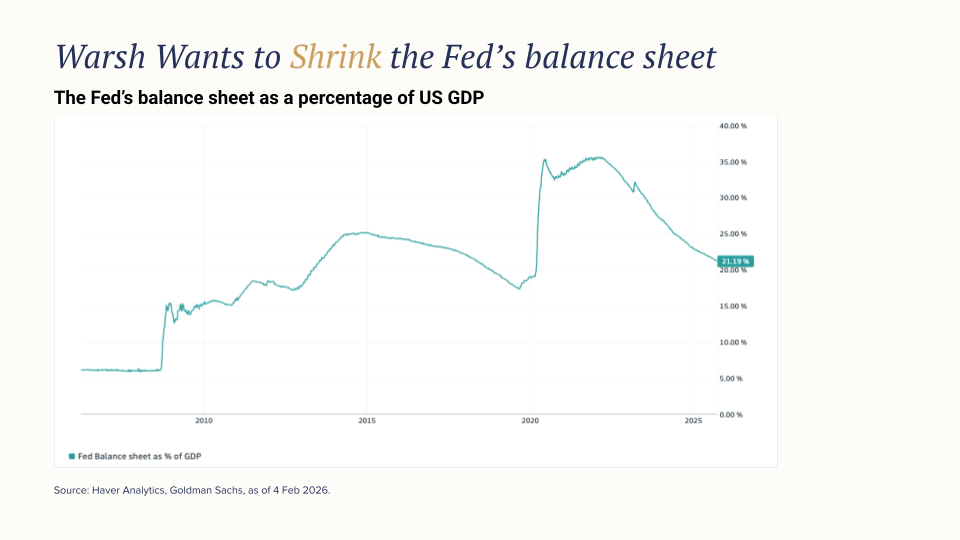

The balance sheet: Since 2008, the Fed has purchased trillions in Treasury bonds and mortgage-backed securities — quantitative easing (QE) — injecting liquidity and compressing risk premiums. Reversing this process would mean quantitative tightening, or QT, which implies withdrawing liquidity and can elevate long-term rates.

Generally, lower rates benefit equities, particularly growth companies. A large Fed balance sheet supports asset prices by maintaining abundant liquidity. A reversal could weigh for a while on the stock market.

Why are investors worried about Warsh?

Kevin Warsh has worked on Wall Street and in government. He was a governor at the Fed during 2006-2011, right through the turmoil of the Global Financial Crisis. “Warsh is well-known, respected, and accomplished,” said asset manager PIMCO.

He resigned from the governorship because he was unhappy with the central bank’s bloated balance sheet. The Fed at that juncture had just rolled out QE2, expanding its huge asset purchase programme to support the economy following the financial crash. Warsh argued at the time that these measures would distort markets and enable fiscal imprudence.

Warsh advocates an unusual policy combo: cutting rates while shrinking the balance sheet. He claims this would support Main Street — households and small businesses — while balance sheet reduction would tighten conditions for asset markets. His unapologetic stance on tightening liquidity is one reason why markets are nervous.

Warsh has also questioned the effectiveness of the Fed’s reliance on “forward guidance” — policymakers trying to manage the market’s expectations by signalling future policy direction. He wants to see a more data‑driven approach with less communication. That opacity could introduce greater swings in markets, as traders react to more data releases.

Could the markets be wrong about Warsh?

Warsh’s policy view is more nuanced than the violent market reaction suggests. The unwinding in precious metals suggests markets are bracing for an extremely hawkish Fed. But economist Robin Brooks of the Brookings Institution sowed doubts over how hawkish Warsh will end up as Fed chair should he come under pressure from the Trump Administration.

Brooks pointed to the movements in two-year Treasury yields, which fell after the announcement of the Warsh nomination, as an indicator of how markets expect policy to evolve. Warsh’s rhetoric on inflation also leans on the dovish side, with an optimistic view on productivity gains suppressing price rises.

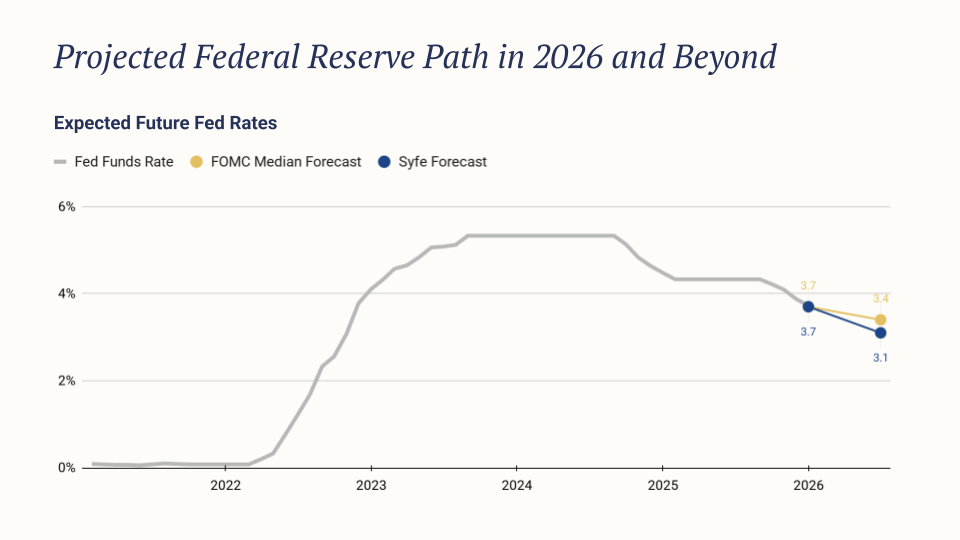

PIMCO expects Warsh to support two to three rate cuts this year before pausing to observe changes in inflation expectations. The asset manager believes his focus on inflation and long-term stability will be constructive for markets.

Whether Warsh gets everything he wants also remains to be seen. Shrinking the balance sheet runs counter to a US Treasury Department that wants to borrow more to stimulate the economy, and Warsh has argued for closer coordination between the Fed and the Treasury in the form of a new “Fed-Treasury accord”. If confrontations arising from this relationship disrupt US mortgage and Treasury markets, Warsh may be forced to moderate the pace or extent of his plan.

Let’s not forget, finally, that the Fed chair does not determine policy alone. Warsh will be one of 12 voting members of the Federal Open Market Committee who call the shots.

Who are the winners and losers?

If short-term interest rates do come down, the broadening in the equity market could continue. Small-caps, which have hitherto not rallied as much as larger companies, could catch up as they benefit from reduced borrowing costs. Smaller banks could see upside from deregulation, analysts at Goldman Sachs wrote in a 1 February 2026 report, noting that Warsh is in favour of facilitating bank consolidation.

Long-dated bonds may face more headwinds as the Fed shrinks its balance sheet. “Yields have risen as investors anticipate less willingness to use the Fed balance sheet to suppress term premiums,” according to Janus Henderson.

We continue to monitor movements in gold and silver. A lot hinges on how far and fast Warsh cuts rates this year. While analysts expect a Warsh-led Fed to cut rates, he could still leave real interest rates in positive territory, i.e. just above inflation to restrict liquidity and speculation. That would mount more pressure on the precious metals and the “debasement” trade.

How does this impact Syfe’s market outlook and portfolios?

Our core thesis set out in the 2026 outlook — continued disinflation, monetary transition toward neutral rates, and broadening equity participation — remains intact. We had expected greater volatility going into the year.

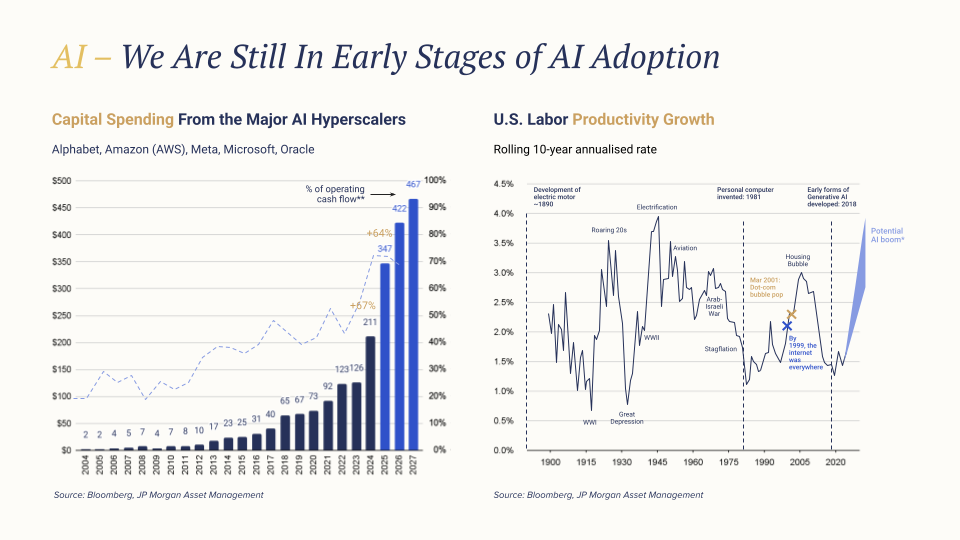

In fact, Warsh’s view on the impact of artificial intelligence on inflation probably aligns more with us than with the current Fed. Warsh believes AI will generate a productivity boom similar to the 1990s internet revolution, creating disinflationary conditions. We continue to expect two more rate cuts this year, bringing the federal funds rate to about 3.1% by end-2026.

Most investors lose out in volatile markets, chasing frenzies as markets rally and closing their positions prematurely during panics, thus missing out on the recovery. Our managed portfolios present a solution to stay invested in uncertain times, as Syfe manages all the rebalancing necessary for optimising long-term performance.

Despite the volatility in the bond market, Income+ continues to produce steady streams of income derived from a broad range of bonds. REIT+ offers non-US exposure to real estate, focused on Singapore, where the economy is strong, and is set to benefit from the lowering of financing costs. Our Core Portfolios provide a suite of solutions to capture the broadening of market leadership and generate long-term value, depending on your risk appetite, time horizon, and financial goals.

You must be logged in to post a comment.