As the Iran War roils global markets, many investors are worried about the impact on their portfolios. A closer look at history, however, suggests that they can be cautiously confident. We review the lessons from the past and explore the possible paths ahead.

Long Story Short: Risk Assets Rise (Eventually)

It’s hard to believe this when you’re in the thick of it. But most military conflicts have only a short-term impact on financial markets. Risk assets, such as equities, ultimately prevail.

On average, it takes less than two weeks (13 days) for the S&P 500 index to bottom after a geopolitical crisis and less than a month (28 days) to recover, according to this tally put together by RBC Wealth Management. The average fall from peak to trough is only about 6%.

By design, markets are forward-looking. They try to price the future value of assets. So, once there are signs of de-escalation or clarity around a resolution to a conflict, investors begin to shift their attention to the recovery and profit from depressed valuations.

The Caveat: Conflict Longevity Matters

Where it gets tricky is if there is a protracted conflict. Confidence erodes as the war goes on, and disruptions to energy flows and supply chains eat into economic growth, weighing on earnings expectations. Markets, consumed by imminent and seemingly insurmountable challenges, cannot see a way through the crisis and a path to recovery.

The fundamental question right now is whether the war in Iran will push up inflation and derail global growth. The answer depends on what happens next in the Strait of Hormuz, the narrow stretch of water off Iran’s shore responsible for 20% of the world’s oil shipments and liquified natural gas (LNG). At the time of writing, it is closed down by Iran. How long that lasts will help determine the path ahead for financial markets.

The Bull Case: Peace Prevails, Albeit Fragile

In this scenario, the Strait reopens six to eight weeks into the war. A de facto ceasefire is achieved – either because the US and Israel consider their campaign complete without regime change, with the degradation of Iran’s ballistic missile and naval capabilities, or the Iranian leadership capitulates under pressure. Fighting may continue, but no more fiercely than at the outbreak of the conflict. Markets could see a way through to peace, even if it’s a fragile one.

With supply obstructions removed, investors are reminded that oil remains in oversupply. Oil prices duly correct. Crucially, inflation resumes its downward trajectory, putting interest rate cuts back on the table in the US, Europe, and many parts of the world. The global economy is largely undented. Markets soon bottom out, as they did in the 1991 Gulf War and 2003 Iraq War.

The military threat could still be an overhang in this scenario. But it will be overshadowed by the market narratives that dominated before the war. The US dollar, in particular, will once again face headwinds from both rate cut expectations and investors diversifying from the US to less concentrated, higher-growth markets. Net importer markets, hard hit by the initial sell-off, would claw back lost ground. In this case, we would expect AI to regain investors’ focus again.

The Bear Case: Protracted War Brings Back Inflation Threat

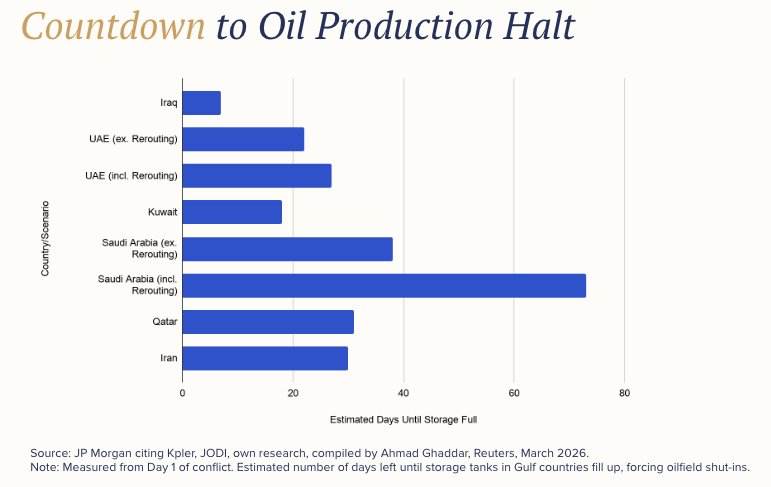

In this scenario, neither side would de-escalate. Even as the US and Israel ramp up strikes, Iran and its proxies persistently disrupt maritime traffic in the Strait of Hormuz, effectively keeping it shut indefinitely. With no clear route to ship oil, Gulf states freeze production. Oil reserves, initially abundant, deplete in net importer countries. Oil prices surge and stay elevated, inflation jumps, economies crater, and industries suffer across the board.

A week into the war, part of this scenario is beginning to play out. Gulf production could be halted within days, Qatar has warned. Analysts at JPMorgan had expected this to happen weeks into the conflict. Markets are moving rapidly to price in the risk. Oil prices came close to testing US$120 a barrel, which would be the highest in more than a decade and a half. This run-up is already steeper than the one in the early stages of the war in Ukraine.

The prospect of a long war is significant as it is upending several popular trades. Going into 2026, markets had expected dollar weakness to persist, setting up emerging markets for another year of outperformance. Hardware-heavy developed Asian markets have performed well as investors seek to diversify away from the US but stay exposed to AI-driven growth.

These tailwinds are all at risk from a protracted conflict that would stoke inflation, stifle rate cuts, and send investors chasing the greenback as a safe haven. The sell-off in Asia, where China, India, Japan, and Korea are all net importers, has been particularly painful.

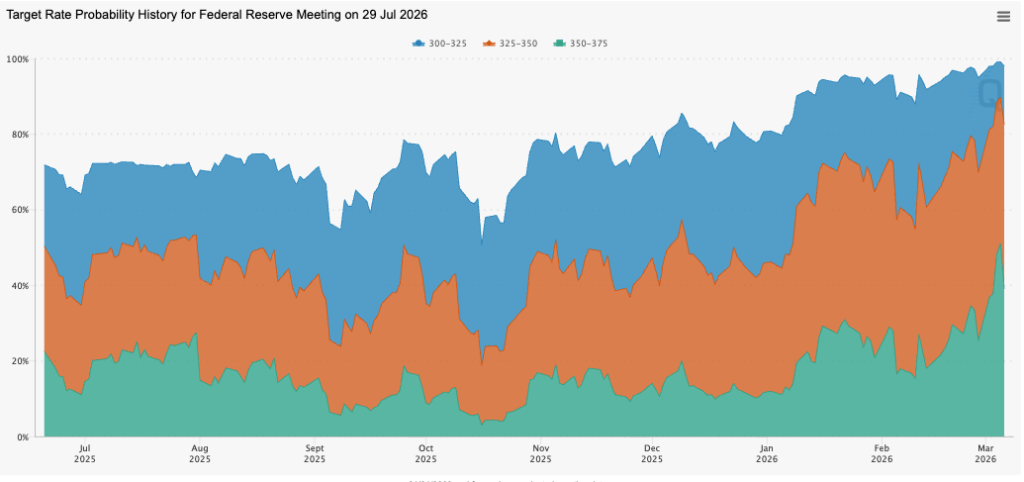

The biggest risk in this basket is a reversal in US inflation, which, incidentally, was intensified by another war just a few years ago. Progress in pushing down prices has been hard-won. Even if the new Fed chair is inclined towards rate cuts, he and other voting members of the Federal Open Market Committee would have to contemplate the effects of elevated oil prices. In the futures market, traders are raising the probability of the Fed resisting rate cuts as far out as July (the green portion of the chart below represents bets on the rate range staying at 3.5%-3.75%).

Source: CME FedWatch, March 2026.

Three Tips for Navigating Volatile Times

Diversification remains the best defence. Gold has served as a strong buffer and driver of returns. Investors with a broad portfolio across geographies and asset classes should be better protected. Equities in the US, a net exporter of energy, have been holding up better than those in Asia of late.

Discipline matters. Investors have been used to dip-buying whenever there is a correction in the market in the past few years. But that phase of broad equity gains, fuelled mostly by AI, is behind us. Markets are less forgiving as concentration builds and valuations get stretched. Selection and quality will form another line of resilience in a diverse portfolio.

Finally, focus on fundamentals. If history is any guide, the unfolding crisis will unlikely remain the market’s focus three years from now. But the impact of AI will likely be more pronounced in that timeframe, with real productivity gains and fresh impetus for growth. Viewed in that prism, markets will eventually return to evaluating fundamentals, however volatile it gets in the interim.

Build Your Portfolio On Syfe

Our Core portfolios continue to offer a solid foundation to capture long-term growth and help investors stay invested. For those with a greater risk appetite, they can add the newly launched Equity Alpha to that mix, strengthening their ability to be selective in a “dispersion” market where the gap between winners and losers is widening. These portfolios are mutually complementary, and together, give investors the flexibility they need to build a broad portfolio.

On Syfe Brokerage, where you can express your high-conviction ideas, our Gold Bundle has been one of the most popular of late. It provides access to the broader global gold ecosystem through a mix of physical gold ETFs and gold mining stocks. You can start investing from just US$100, and, as with all Syfe Bundles, enjoy 50% off commission fees.

You must be logged in to post a comment.