Financial independence is essential for women, but our recent survey revealed a confidence gap that deters many women from taking charge of their finances. Here’s why women in Singapore can and should build long-term wealth, even if you’re just starting out.

For many women in Singapore, investing is something often delegated or postponed—until we have a higher income, until we have time to “learn properly”, until investing feels less complex or risky.

But the best time to start investing is always yesterday. The next best time is now. Financial independence waits for no woman, especially in this day and age.

Women live longer. Women are more likely to take career breaks due to pregnancy and motherhood. And women often shoulder caregiving responsibilities that can disrupt income trajectories.

As the cost of living rises and careers become increasingly non-linear, women are beginning to face a different set of long-term financial risks.

Yet, despite these realities, many still leave investing for later or in the hands of a partner or parent.

True empowerment is when you have autonomy over your investing decisions. And investing independently—even in small, structured ways—just calls for practical planning, not taking risky bets or constant market-watching. A sensible approach to investing, even if you’re starting from zero, can put women in Singapore on the right path to financial independence.

Why Financial Independence is Important for Women

Women Face Higher Long-Term Financial Risk

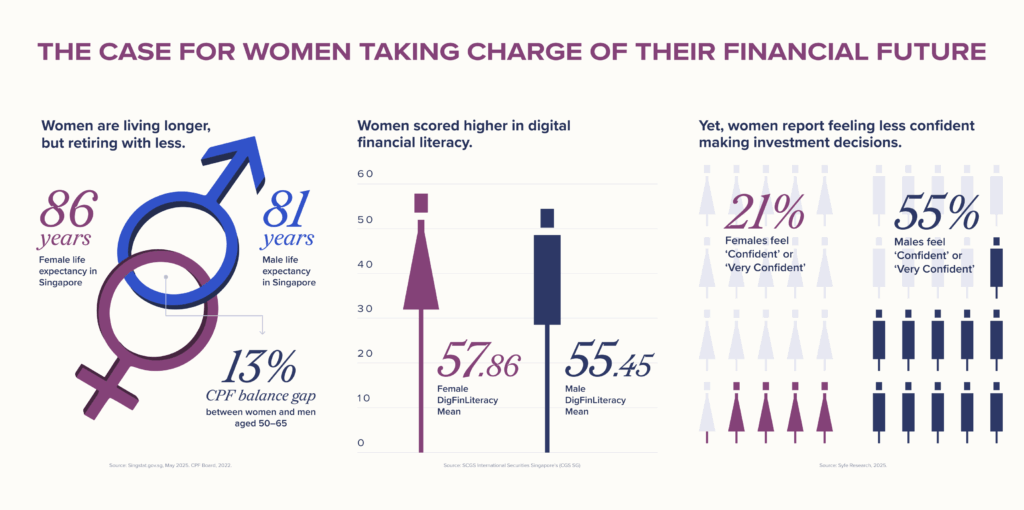

Women in Singapore live around 5–6 years longer than men on average. That alone changes the math of retirement because a longer life means:

- more years of daily expenses

- greater exposure to inflation

- higher cumulative care-related costs, including healthcare

At the same time, caregiving duties—be it for children or ageing parents—are still disproportionately borne by women, who then have to take career breaks for this.

On top of that—or perhaps as a result of that—there is a significant wage gap between male and female earners in Singapore. According to Ministry of Manpower data published in 2024, Singapore women’s median income was 14.3 per cent less than men’s in 2023.

Even when women return to work, their income growth and CPF contributions may lag behind those with uninterrupted career paths. Based on the CPF Board’s 2022 data, among those aged 50–65, women’s total CPF balances were 13% lower than men.

As a result, there’s a double squeeze: retirement needs are higher, while retirement resources are often lower.

CPF LIFE may provide a baseline for a basic retirement, but for many women it is not designed to fully replace income over a 25–30 year retirement. This is why personal investing increasingly plays a critical role in long-term capital growth.

Delegating Investing Decisions Brings Risks

In many Singapore households, women are involved in managing money day to day—tracking expenses, planning budgets, and managing household cash flow. But when it comes to long-term investing, responsibility often shifts elsewhere.

This arrangement is common. Investing can feel intimidating, technical and time-consuming, and there is a tendency to let someone else handle it, especially if they’re already “better at it”.

But when it comes to investing, there is a risk in taking your hands off the wheel.

When you don’t know what assets exist, how those assets are invested, or how much risk is being taken, you may be left vulnerable during major life disruptions. Divorce, illness, job loss, or bereavement can force financial decisions to be made often without the time and consideration needed to make them confidently.

Investing independently doesn’t mean eschewing shared financial planning, but ensuring that you have clarity, access, and agency over some part of your financial future.

Why Many Women Delay Investing And Why Waiting is Costly

Women new to investing tend to wait until they feel “ready”. Often, this means earning more, knowing more, or feeling more confident.

But investing doesn’t reward readiness. It rewards starting early and consistency.

Starting to invest even five or ten years later can reduce long-term returns, even if contributions are increased later. That’s because compounding—the key engine of long-term wealth—works better with time, not intensity.

Many women delay not because they lack money, but because they fear making mistakes. Ironically, the biggest mistake is often starting too late or not starting at all.

According to a recent report by CGS International Securities Singapore’s (CGS SG) and Republic Polytechnic, even though females scored higher in digital financial literacy, males were the ones who felt more confident about having the knowledge and skills to succeed.

This concurs with our findings: Men are twice as likely as women to feel self-assured in their investment decisions.

- 55% of men say they are “Confident” or “Very confident,” compared to only 21% of women.

- 46% of women cite a “Lack of knowledge or confidence” as the main reason they don’t invest more. For men, this drops to 24%.

Yet, the aim of a first investment isn’t to maximise returns, but to just begin participating, learning, and building familiarity without taking on excessive risk or complicating the process.

Saving Is Not Enough

Women in Singapore are generally prudent savers. Emergency funds and savings accounts offer reassurance and liquidity, and they should always come first.

But saving and investing serve different purposes.

Savings protect you from short-term shocks. Investing safeguards your long-term purchasing power.

Over time, inflation quietly erodes the value of cash. Your account balance may grow, but the value of that money shrinks. Relying too heavily on cash can mean having to save much more just to afford the same things years later.

In terms of portfolio complexity, our survey found that 48% of men hold 5 or more asset classes. Only 22% of women have that level of diversification, with a higher concentration in cash/savings and REITs.

A more resilient financial strategy separates money by purpose:

- Short-term needs and emergencies stay as cash

- Long-term goals like retirement are invested for growth

This is where structured, diversified portfolios come into play, especially for beginners. They allow women to invest for the long term without needing to pick stocks or time markets.

An Investing Strategy For Women Starting Out

For women who are new to investing or returning to it after years of delegation, the first question is, “How do I begin?”

A practical strategy usually has three parts.

1. A solid cash buffer

Before investing, ensure you have an emergency fund that covers several months of expenses, ideally 6–12 months. This reduces the likelihood of having to sell investments during market downturns or liquidate funds during emergency situations.

High-interest cash solutions can help here, keeping short-term money accessible while earning more than traditional savings accounts.

For example, Syfe Cash+ portfolios are designed for capital stability and liquidity, making them suitable for emergency or near-term funds.

*Cash+ Flexi projected returns are based on annualised amortised yield estimates of the underlying funds provided by the fund managers, as of 17 Dec 2025. They are not guarantees of future performance. Cash+ Guaranteed returns are guaranteed, subject to underlying bank risk.

#For Cash+ Guaranteed (USD) only: The guaranteed capital and returns apply only to the USD value of your portfolio, regardless of the currency it’s deposited in. Funding or withdrawing in a non-USD currency may impact your returns due to exchange rate fluctuations.

Cash+ Flexi is a cash management account that aims to provide returns higher than a typical savings account by investing in a portfolio of low-risk, high-liquidity money market and short-term bond funds. It comes with no lock-in periods or minimum balances (for SGD), and unlimited next-day withdrawals.

With four underlying fixed deposits, Cash+ Guaranteed is a low-risk cash management solution that offers investors a better place to park their cash. As the name suggests, it’s a capital-guaranteed portfolio that is designed to provide higher returns on your cash while keeping your principal protected by securing the most attractive rates from banks in Singapore.

2. A diversified, long-term portfolio

Once cash needs are covered, long-term funds can be invested for growth. For beginners, diversification is far more important than outperforming the benchmark. Many try to outperform the market only to find themselves exposed when markets move against them. It is far more important to build the foundations through diversification before taking on more risk.

Syfe’s professionally managed Core portfolios—which spread investments across global equities, bonds, and commodities—help reduce reliance on any single market or asset class. This approach suits women looking for long-term growth with a disciplined strategy and structure, but don’t want to actively manage investments on their own.

Our Core portfolios are designed around diversified global assets and rebalanced automatically, making them suitable for long-term wealth building. With four different types of portfolios comprising varying proportions of equities, bonds, and commodities, investors can select their preferred one based on their risk appetite, time horizon, and financial goals.

3. Automation and Regular Review Process

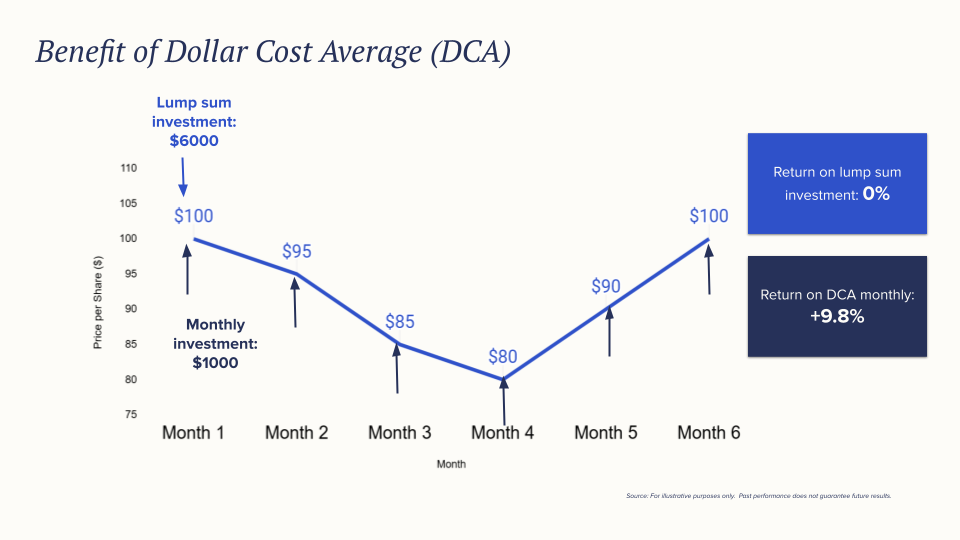

Consistency matters more than timing. Setting up automatic regular contributions removes emotion from the process and helps build investing into a habit.

Dollar-cost averaging also helps to even out the impact of market volatility by averaging out the purchase price and reducing the risk of bad timing.

As for portfolio reviews, these don’t need to be frequent—checking in once or twice a year to ensure that your portfolio still aligns with your goals is usually enough. The goal is not to constantly optimise your portfolio, but to participate in the market steadily and consistently.

Long-term investing is often quiet and uneventful. Traits many women already have—patience, caution, and discipline—are well-suited to this kind of approach.

Building Confidence Is Like An Endurance Sport: Syfe COO Samantha Horton’s Practical Investing Tips

Syfe’s Chief Operating Officer Samantha Horton offers a useful lens for reframing this confidence gap.

In a recent Tatler feature, she likens financial wellbeing to endurance sport—built not on bursts of perfect timing, but on consistency, discipline, and the quiet power of compounding over time.

Her perspective reinforces a key idea for women who feel they are not ready to invest: confidence is often the result of taking action, not a prerequisite for it. You bridge the confidence gap by starting to invest, then finetune your strategy over time.

Her approach to getting started is simple:

- Start before you feel ready

Taking the first step matters more than having perfect knowledge. Much like training for an endurance sport, progress comes from showing up consistently rather than waiting for ideal conditions. - Focus on consistency over timing

Regular investing builds momentum and reduces the pressure of trying to “get it right”. Over time, small repeated actions can compound into meaningful outcomes. - Build for the long term and ignore short-term noise

Short-term market volatility is inevitable, but most financial goals span decades. Staying invested and disciplined through market ups and downs is what drives results. - Simplify your approach

Putting structures like diversification and recurring investments in place can reduce decision fatigue, making it easier to stay on track without constant monitoring. Syfe’s auto-invest feature allows you to make recurring investments to your brokerage account and/or specific managed portfolios.

For those looking to better understand how a steady, structured approach can translate into long-term confidence and independence, her full interview is worth a read.

Financial Independence Gives You More Options

For women in stable relationships or family units, “financial independence” can sound unnecessary or even uncomfortable. But instead of isolation, independence means having options.

It means having:

- assets you understand

- investments you can access

- choices that aren’t constrained by uncertainty

According to Samantha, money as more than just wealth; it is also the ability to create choices for yourself, be it in career, family life, or personal goals. Even modest investments made over time can create flexibility, whether it’s the ability to change jobs, take time off, support family, or simply feel more secure about the future.

You can look at your first portfolio as a learning tool, not a final decision. Over time, contributions can grow, strategies can evolve, and confidence will follow action. With Syfe’s managed portfolios, there is no minimum investing threshold so you can begin with any amount you are comfortable with and let us handle the rest.

For many women in Singapore, intention—not perfection—will build the financial resilience necessary to grow wealth in a meaningful, sustainable way.

Investing in diversified managed portfolios can be a low-pressure way to participate in markets without having to become an expert. Explore Syfe’s options today.

You must be logged in to post a comment.