What’s Going On?

The Fed completed its first monetary meeting of 2024. As widely anticipated, the Fed has kept the Fed Funds rate unchanged at 5.25% – 5.5% for the fourth consecutive meeting. Although the Fed indicated that rate cuts are unlikely to start in March, as the market had hoped, the overall tone seems to be dovish.

Compared to the last meeting, the Fed provided a much clearer signal for a policy pivot in 2024. Notably, the Fed removed the phrase “the extent of any additional policy firming” from the FOMC statement, indicating a pause in rate hikes for the time being. Fed Chair Jerome Powell also mentioned in the conference that rate cuts are expected to start at some point this year, but not as early as March.

Another significant point was the discussion about rolling back Quantitative Tightening, or the process of removing money from the economy. Tapering of quantitative tightening typically means a slower rate of liquidity withdrawal from the markets, which could result in more cash being available for investments, potentially boosting both stock and bond markets.

In immediate market reaction, equities pulled back with the S&P 500 down 1.6%, while bonds remained positive with the 10-year Treasury yield falling below the key 4% level.

What does it mean for you?

One of the most hallowed commandments in financial markets is “Don’t fight the Fed.” The Fed’s monetary policies have significant implications for investors’ investments.

As the Fed’s policies transition from “tightening” to “loosening,” bonds could be the primary beneficiaries. As interest rates move lower, bond prices tend to move higher. The rout in bond prices over the past two years could now be behind us.

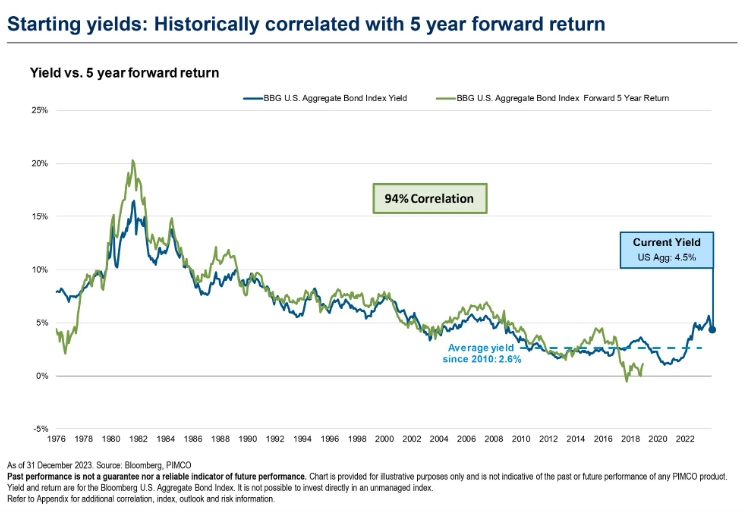

Historically, starting yields have had a high correlation with holding bonds over 3 to 5 years. Currently, bond yields are near 15-year highs. This could represent a good entry point for investors.

Should you act now or later?

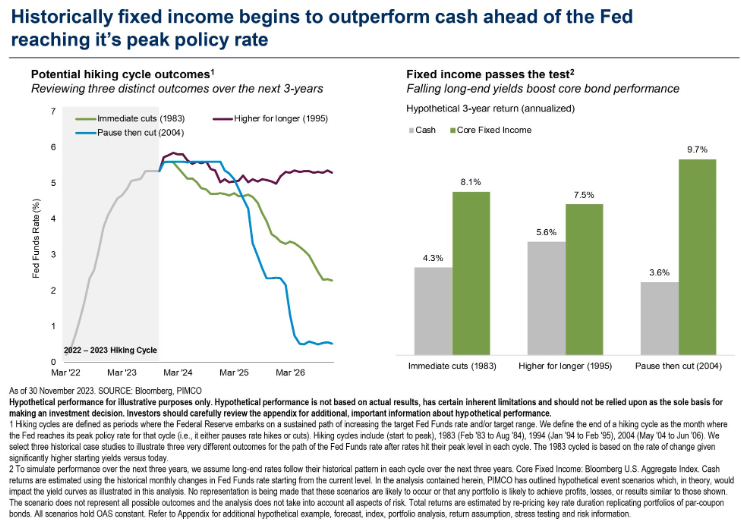

You may ask when to start building positions in bonds, given that the Fed is unlikely to embark on immediate rate cuts.

Based on the study of past cases, the timing of the Fed to start interest rate cuts does not matter as much as you may think.

There are three scenarios for the Fed – immediately cut rates, pause then cut, or maintain higher rates longer. The analysis of past cycles shows that bonds have delivered annualised returns of 7.5% to 9.7% (in USD) over three years, beating returns from holding cash in all three scenarios. This supports the case for investors to deploy excess cash now, rather than waiting for the start of the Fed’s rate cut.

How can you implement the ideas?

- Bond ETFs. One cost-efficient way to buy into bonds is through ETFs. There are many types of bond ETFs for you to choose from, ranging from US treasury bonds to international bonds. However, bond ETFs could be more suitable for experienced investors to express short-term tactical views. Many bond ETFs are US domiciled. Dividends paid are subjected to 20-30% withholding tax. Singaporean investors may also be subject to currency risk as the bond ETFs are usually USD-denominated.

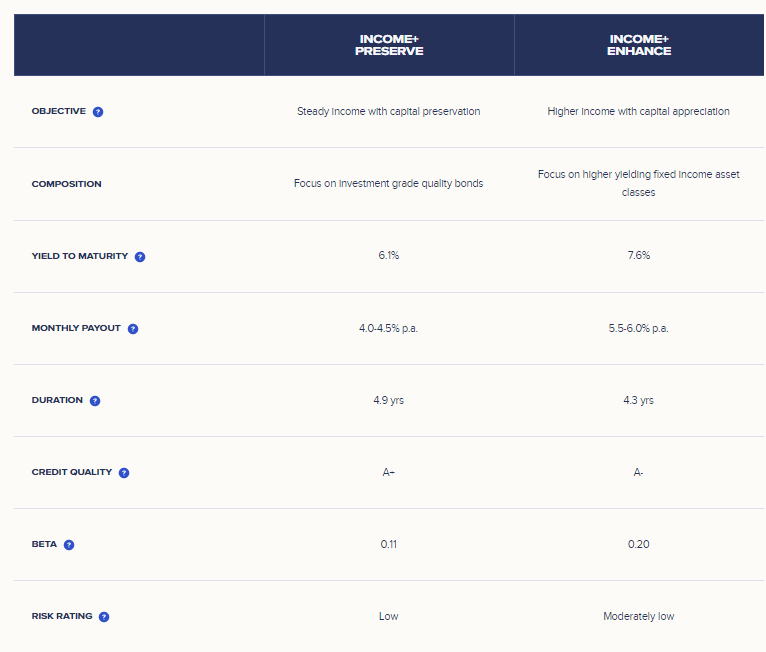

- Syfe Income+. If you are planning to invest in bonds for the long term or to build up passive income, Syfe Income+ might be a more suitable option. Income+ uses PIMCO funds that are actively managed and are able to utilise a broad range of fixed income securities that seek to produce an attractive level of income while maintaining a relatively low risk profile.The funds used in the Income+ portfolios are domiciled in Ireland making them more tax-efficient with respect to dividend withholding taxes. In addition, Income+ portfolios invest into SGD-hedged share classes of the constituent funds to mitigate currency risks.

A Snapshot of Income+ Portfolios

You must be logged in to post a comment.