The stock market has been on a roller-coaster ride in the first quarter of 2021. Over the past months, investors grappled with inflation fears and rising Treasury bond yields, witnessed a rotation into value shares, and in recent weeks, watched as technology and growth stocks retook the market’s reins.

Where the market goes from here is anyone’s guess. Growth stocks have dominated for over a decade. But the resurgence of value stocks this quarter has reignited the age-old debate between the merits of value and growth. Is one necessarily better than the other?

What are value stocks?

Value stocks trade at prices below their fundamental value. They are usually defined as those with low price/book ratios and low price/earnings ratios.

Price/book ratio lets investors know how a company is valued by the market compared to how it is valued based on the book value of its business. Price/earnings ratio simply tells investors whether a company is expensive compared to peers in the same sector for instance.

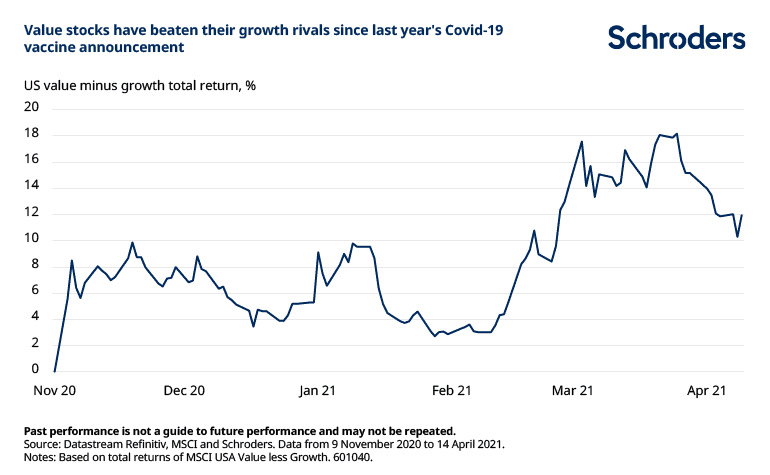

Explaining the rotation to value

Value stocks have been out of favour for some time. But economic optimism and a faster-than-expected coronavirus vaccine roll-out have been catalysts for their remarkable comeback to date.

Value stocks spiked up sharply in the first quarter of this year as investors jumped on stocks expected to benefit most from the economic recovery, such as travel, financial, energy and materials companies.

These sectors tend to trade with low price/book and price/earnings metrics, which explains why they’re usually classified as value sectors.

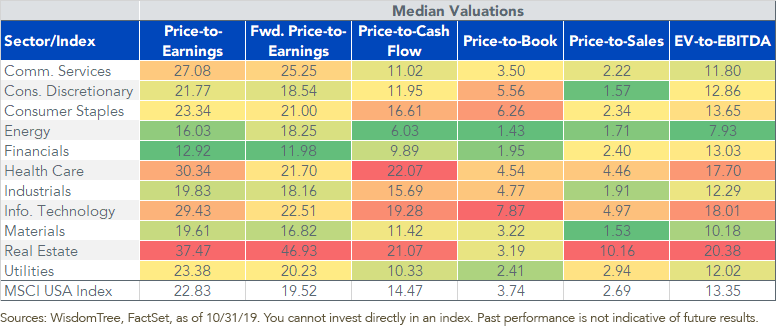

The table below gives a good overview of the significant differences in valuations across sectors.

Financials, energy and materials typically have the lowest valuations while information technology and healthcare have the highest. This makes sense; information technology stocks tend to grow faster than stocks in other sectors so investors are more willing to pay higher prices relative to fundamental values.

Given value stocks’ underperformance over the years, they could now be offering faster recovery potential at a much lower valuation as the economy reopens.

Many factors support a strong recovery; trillions in stimulus, an accelerated vaccine roll-out are all at play. The US Federal Reserve expects the US economy to grow by 6.5% in 2021, its strongest expansion in nearly 40 years.

Rising Treasury yields have played a part too in value’s comeback. Higher yields have diminished the allure of growth stocks and sent investors flocking to value stocks instead.

The value rebound might still have legs

Even after their recent comeback, value stocks are trading some 74% cheaper than growth peers on price/book measures, according to BCA Research. Value stocks remain about 11% below their historic average discount to the market as well, based on data from Societe Generale. This discount is comparable to where value stocks stood in the midst of the 2008 financial crisis.

This steep discount to growth stocks may give value more room to run. With the economic reopening still in early stages, value stocks certainly have more upside potential. In a note published last week, JPMorgan Chase expressed bullishness on the value trade, with emphasis on “higher quality companies with greater staying power, for example retail and energy”.

Growth stocks rebound

Lately however, the market has seen a pause in the gains made by value stocks. Tech-related growth stocks on the other hand have charged higher, in part due to a decline in long-term Treasury yields. The 10-year Treasury yield stood around 1.8% on 30 March and has since come down slightly to near 1.6%.

Rising yields tend to hurt technology and growth stocks. Due to their high valuations and high expected future profits, rising bond yields reduce their stock value in many valuation models.

And while the rotation to value stocks may resume as the economic reopening continues, it doesn’t mean value stocks are always going to be better investments than growth stocks over the long term. The underlying fundamentals of many top technology and growth stocks remain sound.

Furthermore, the pandemic has accelerated trends in technology adoption and digitalisation that might otherwise have taken years to play out. Structural trends such as the move towards 5G and the growth in cloud computing continue to bode well for technology stocks. Over the long term, the potential return tech and growth stocks can offer could still be lucrative.

An eye on both growth and value

It is possible that we may see more frequent rotations whereby value stocks gain steam then slow down, and growth and tech stocks pick up the slack in between.

As such, we believe that having some exposure to value stocks, while still keeping a moderated exposure to growth, is the best way forward for investors.

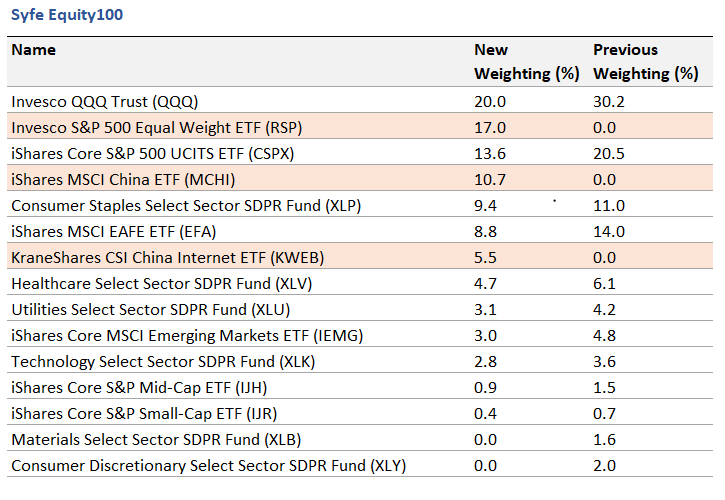

This is a key reason why during our recent rebalancing for our Core Equity100 portfolio, we added a considerable allocation to RSP, while still maintaining a moderate exposure to the growth and tech-heavy Invesco QQQ.

RSP is also known as the Invesco S&P 500 Equal Weight ETF. Simply put, every stock held by RSP has the same weight, regardless of how large or small the company is.

RSP thus leans towards smaller companies and value stocks as compared to a market cap weighted S&P 500 ETF. In the latter, the top holdings are still concentrated in big tech names such as Apple, Microsoft, and Facebook. Essentially, the addition of RSP neutralises Core Equity100’s large-cap factor tilt while moderating its exposure to the growth factor.

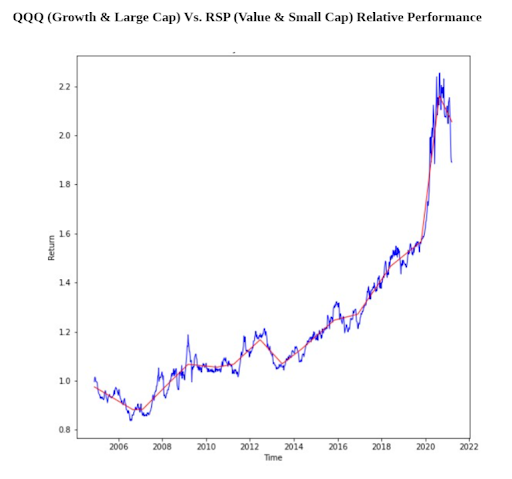

For almost a decade, the QQQ (an ETF with exposure to growth and large-cap stocks) had outperformed the RSP (an ETF leaning towards value and small-cap stocks). But as shown in the graph below, RSP is catching up.

An uptrend indicates that QQQ is performing better than RSP. We see that while QQQ outperformed RSP for most of 2020, that trend has reversed. Since the start of the year, RSP has been outpacing QQQ.

Although there is room for value to make a sustained comeback, we believe that technology and growth is a long-term theme that has legs.

The strength of these companies is in how they innovate. Post-pandemic, these are the companies that will continue to find new ways to change how we work, play and interact.

For long-term investors, our advice remains the same. Ensure your portfolio is well-diversified across different assets, geographies and styles. This approach may not top performance tables all the time but over the long run, it will help you experience a smoother investment journey and sleep better at night.

You must be logged in to post a comment.