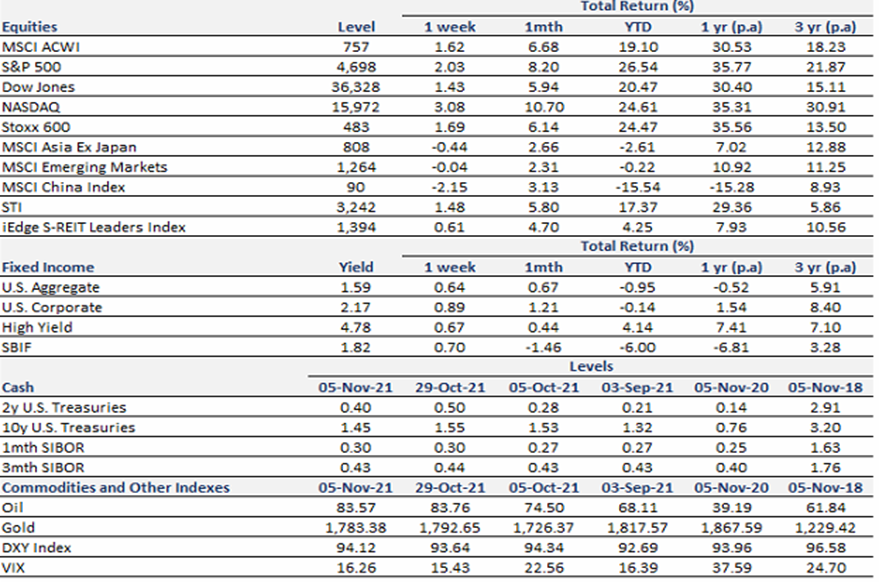

Thought Of The Week

FED Meeting and US Equity Markets

The US Federal Reserve met on Wednesday this week and came up with the decision to commence tapering bond purchases and to hold interest rates steady. The tapering decision was on the back of an anticipated stronger economy. In light of the Federal Reserve’s outlook, small cap stocks jumped strongly as per the previous time the Federal Reserve announced the commencement of tapering. Bond yields also correspondingly rose with the tapering decision, with longer dated treasuries being more sensitive. It was also notable that Powell clarified that the rate of taper could change after December and would not rule out either increasing or decreasing the rate of asset purchases.

Despite the backdrop of higher inflation, Powell maintained that inflation was transitory and showed little urgency to raise interest rates. Powell also noted that progress was still needed to achieve “maximum employment” which led the Federal Reserve to hold interest rates steady. The Federal Reserve’s decision bode well with equities – with the NASDAQ and S&P 500 reaching record highs on Wednesday and the Russell 2000 and Dow Jones ending with a positive close near a record high on Wednesday.

G20 Summit and COP26 Outcomes

Over at the G20 Summit, climate issues were one of the main focus. Nations agreed to limit global warming to 1.5 degrees above pre-industrial levels and pledged for carbon neutrality in the mid century. With regard to climate financing for less developed countries, there were divergent views. Post G20, at the COP26, substantial progress was made on Thursday with 20 countries agreeing to end public financing for international fossil fuel projects by 2022. This agreement is the first of its kind with past agreements revolving around coal only.

At the G20 Summit, Leaders also pledged to support WHO’s vaccination goals of 40% vaccination rates by 2021 and 70% by mid 2022. This would be done by increasing vaccination supplies for developing countries. Lastly, leaders also noted that the economies were still in recovery and dismissed a quick removal of economic stimulus.

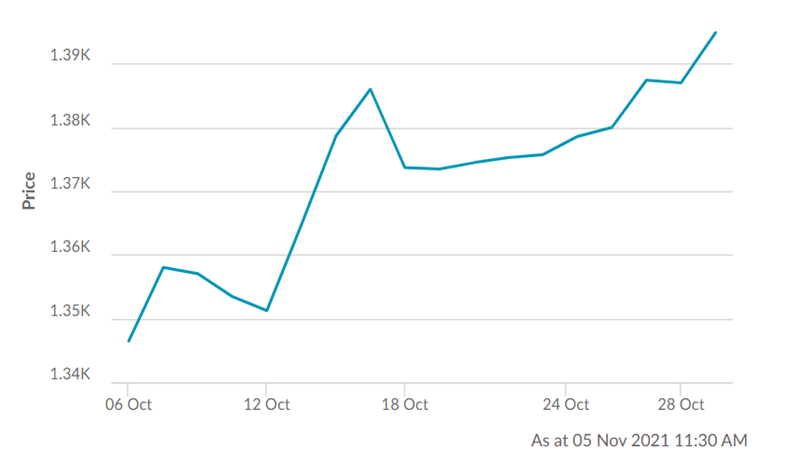

Singapore REITs

Earlier in the REIT earnings season, we noted good performance in a few major REITs. Mapletree Logistics Trust and Mapletree Industrial Trust posted a DPU increase of 5.7% and 11.9% respectively while Ascendas REIT posted a slightly higher occupancy rate. This week, Lendlease REIT posted steady occupancy rates driven by high tenant retention rates of 90% at its 313@somerset property. Parkway REIT despite headwinds, posted a slight DPU increase of 0.8% this week. For Singapore REITs which solely focus on overseas properties, Prime REIT and Elite Commercial Trust posted DPU increases this week while Manulife US REIT posted better leasing activity. The overall better financial and operational performance of Singapore REITs have fueled a recent REIT upturn.

Chart Of The Week

Important Information and Disclosure

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.