This week marked a significant milestone as we hosted our first in-person event of the year, “Market Outlook 2024,” featuring a panel of industry experts from BlackRock, PIMCO, and KraneShares.

We thank our distinguished panelists for adding great insights to the discussion:

- Giri Rajendran: Investment Strategist, iShares Asia Pacific, Blackrock

- Alice Lo: Senior Vice President, Head of Singapore Retail, PIMCO

- Brendan Ahern: Chief Investment Officer, KraneShares

If you weren’t able to join us or would like to revisit the engaging discussions, watch the replay here:

Below is a recap of the insightful session:

Global Equity Market Outlook by Blackrock

Not Your Typical Economic Cycle The US economy has stayed resilient in the past year, However, zooming out shows how the economy is still climbing out of a deep pandemic hole. Inflation, including wage and core, is moderating but remains above the Fed’s 2% target. A critical question is whether inflation will slow faster than rate hikes cause a recession. BlackRock believes that the Fed will eventually cause the economy to slow down.

Focus on Mega Forces. BlackRock recommends caution with US equities but also suggests seeking out “mega forces,” or structural shifts, to counterbalance cyclical slowdowns. The top megatrends identified are Digital disruption and AI, Geopolitics and economic competition, Low carbon transition, Demographic divergence, and the Future of finance.

US Industrials Look Interesting. US industrials appear to be an interesting bet on a few of the major megatrends, particularly Geopolitics and Low carbon transition. Approximately 20% of the US Industrial sector is aerospace and defence, making it a relatively diversified play on the geopolitical theme. The demand for industrial products in the US is expected to continue rising, driven by infrastructure investment for clean energy projects and potential semiconductor reshoring.

Bullish on Japanese Equities. Lastly, BlackRock expresses a bullish stance on Japanese equities. Japan has emerged from three decades of low growth and inflation stemming from the real estate crash in the 1980s. Policymakers are putting in efforts to shift corporate profits to households, increase labour bargaining power, and hence consumption and investment. The Japanese government is now also providing tax incentives for domestic savers to invest in Japanese equity markets. All these factors contribute to a bullish case for Japanese equities.

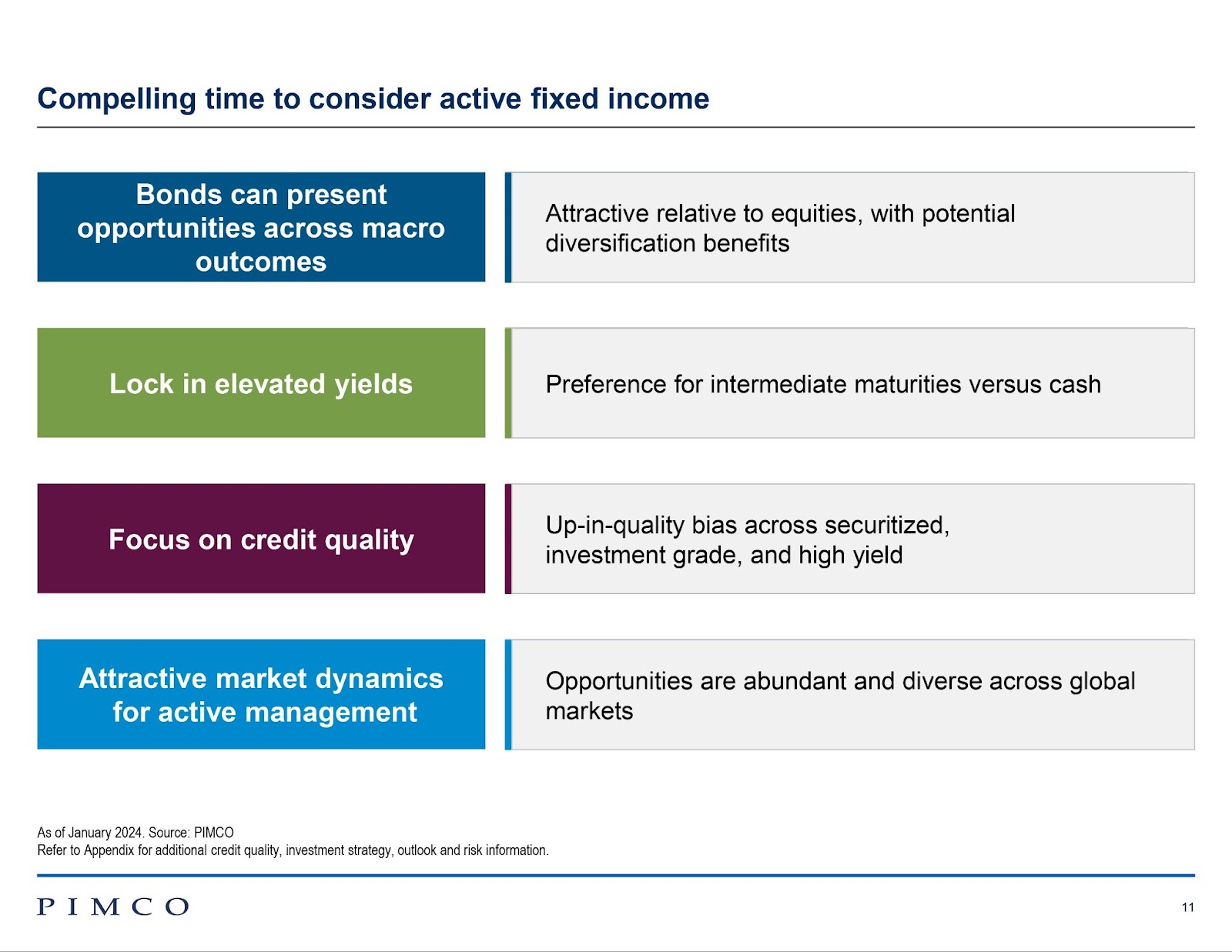

Global Fixed Income Outlook by PIMCO

Recession Risk Remains Elevated. Despite the market consensus of a soft-landing scenario in the US, PIMCO sees elevated risk of recession in the US and other developed economies. This is due to the depletion of excess savings accumulated during the pandemic, leaving US consumers with a smaller buffer against potential economic shocks.

Federal Reserve’s Interest Rate Cuts. Historically, the average Fed rate cut is 2% when the economy is not in a recession, and 5% during recessions. Currently, the bond market is pricing in a 2% cut, i.e a soft-landing scenario. However, if the economy slows more than expected, the Fed might implement more significant rate cuts, potentially increasing the upside for bond prices.

Bonds Can Offer Equity-Like Returns. In the current high-interest rate environment, bonds can potentially provide equity-like returns but with lower volatility. The S&P 500 is at an all-time high, while bond yields are near their 15-year peak since 2008, indicating high return potential going forward. PIMCO also emphasises on active management and being selective. PIMCO is particularly bullish on high-grade bonds, which offer attractive yields ranging from 4.5% to 7%.

Timing the Market: Now or Later? A common question is when the Fed will start reducing rates. The market expects the first rate cut to begin in March this year, but PIMCO predicts it may not occur until the second half of 2024.

There could be three scenarios for the Fed – immediately cut rates, pause then cut, or maintain higher rates longer. PIMCO’s analysis of past cycles shows that in these three scenarios, bonds have delivered annualised returns of 7.5% to 9.7% over three years, beating returns from holding cash in all three scenarios. This supports the case for investors to deploy excess cash now.

China Outlook by Kraneshares

US Equities Have Become a Very Crowded Trade. Since the global financial crisis, US equities have surged by 860%, while Chinese equities have increased by 106%. Due to the US market’s continuous outperformance over other markets, US equities have become crowded, with the majority of institutional investors overweighting in US equities.

Fundamentals vs. Sentiments. The fundamentals of Chinese equities remain sound. For example, Alibaba’s bond prices have been stable over the past three years, indicating a strong balance sheet. However, share prices have slumped, driven more by sentiments, underperforming bond prices by more than 40%.

Does the valuation justify? When comparing US big tech companies to their Chinese counterparts, there is a significant valuation gap. For instance, the 31 largest Chinese internet stocks hold a combined USD 276 billion in cash on their balance sheets, exceeding Amazon’s USD 50 billion and Alphabet’s USD 31 billion. Nevertheless, one could acquire all 31 Chinese internet companies for the market cap of either Amazon or Alphabet and still have USD 300 billion remaining.

How to Position for Chinese Equities? The issue with Chinese equities is not the fundamentals of the companies, but rather investors losing confidence in the government’s policies. Concerns about China have decreased as the government implements incremental stimulus. Due to the high volatility of Chinese equities, Kraneshares advises caution in positioning for Chinese equities. Instead of investing a large lump sum, dollar-cost averaging(DCA) might be a better approach.

How Syfe can help?

- If you want to invest in “mega forces” such as Digital disruption and AI, Low-carbon transition, and Demographic divergence, we offer ready-made Thematic portfolios that capitalise on these mega trends.

- To capture the attractive yields the bond market is offering, you can consider our Income+ portfolios. Income+ portfolios are designed for diversified income with PIMCO’s best-in-class active funds. Currently, Income+ portfolios offer monthly dividend payouts of 4% to 6% per annum.

- To take advantage of the attractive valuation that Chinese companies are offering, we have the China Growth Portfolio, powered by KraneShares. You can easily set up recurring transfers through our platform to execute a DCA strategy.

- If you prefer a self-directed approach to investing, you can buy your preferred stocks and ETFs through Syfe Brokerage. When you use Brokerage, you’ll get free monthly trades, low fees, and access to fractional investing.