You’re tracking your spending, meal-prepping, and diligently saving at least 20% of your income each month. But if you truly want to build wealth, you can’t just save. You also need to make sure your money is growing at a rate that at least outpaces inflation. To increase your net worth over time, here’s what to do.

#1. Invest today

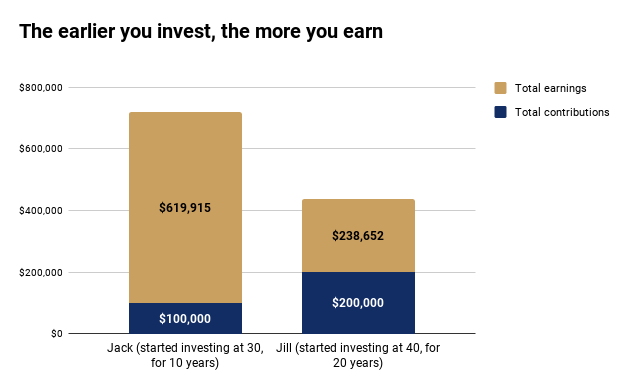

It’s often said that time in the market is more important than timing the market. Consider the example of two friends Jack and Jill below.

- Jack starts investing at age 30 and invests $10,000 every year until he turns 40. From age 40 to 60, he contributes $0.

- Jill only starts investing at age 40 and invests $10,000 every year until she turns 60.

Jill has invested $10,000 every year for 20 years – surely her deck must be stacked against Jack. Not so. Assuming a conservative 7% average annual rate of return, Jack had grown his $100,000 investment to $147,836 by the time Jill invests her first $10,000.

By the time they both turn 60, Jack’s total portfolio will be worth $719,915 whereas Jill will only have $438,652. Jack’s headstart more than offset Jill’s greater total contribution, boosted by his compound interest earned over 30 years.

Don’t wait to invest. Start investing early and maximise what you can afford to invest by saving more.

#2. Manage risk first over returns

Managing risk is at least as important as seeking returns – if not more so.

Risk can be defined as the likelihood of a significant loss. Risk management essentially seeks to limit downside risk and minimise loss. Or in the words of Warren Buffet, “The first rule of investing is don’t lose money; the second rule is don’t forget rule number 1.”

That’s not to say you should fear risk or avoid investing altogether. While all investments carry a certain amount of risk, understanding the risk / reward trade-off can help you protect your investment portfolio.

The first step is finding your comfort level with risk. Think of how you might react to large market swings. Will the amount of risk in your portfolio keep you up at night? Secondly, consider your ability to take on risk. This depends largely on your investment horizon. For instance, if you are in your 30s or 40s, your capacity for risk can be larger than someone older since you have more time to ride out the inevitable rough patches.

Your third consideration should be whether you need to take the risk. Determine the investment return you will need in order to meet your financial goals. While lower risk translates to lower returns, taking on more risk does not always equate to higher returns.

#3. Don’t put all your eggs in one basket

A diversified portfolio made up of different asset classes, such as a mixture of stocks, bonds and commodities can help you better manage your portfolio risk.

In a diversified portfolio, the assets don’t correlate with each other. This means that they tend to react differently to the same economic event (like a recession) and their performance differs from each other. Your overall portfolio risk ends up being reduced because when some of your assets perform poorly, others can bring profit.

If you want an idea of what a diversified portfolio will look like based on your personal risk profile, investment goals, and time horizon, use Syfe’s risk assessment tool to find out.

#4. Minimise investment costs

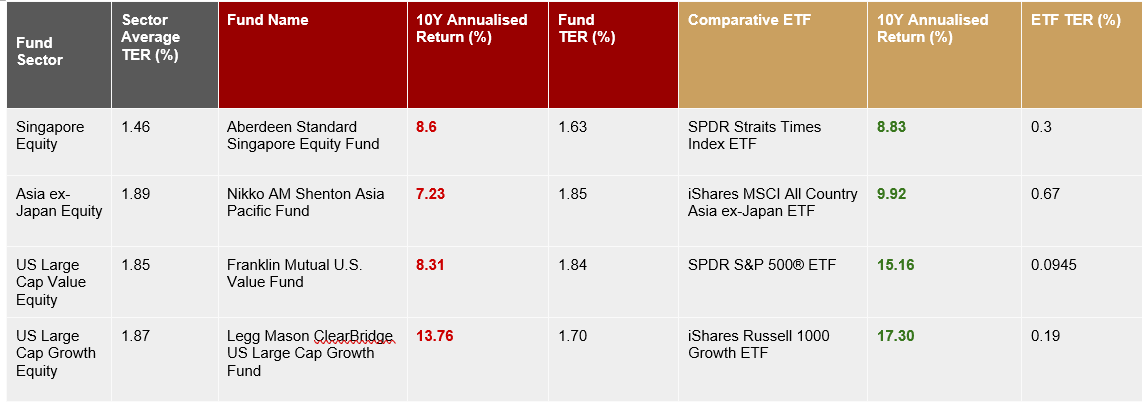

If fund costs are incurred regardless of fund performance, then it is a mathematical certainty that the lower your costs, the more you get to keep of any returns the fund makes. High fees eat away at your returns. While some investors mistakenly believe that high fees equate to high returns, that’s simply not true as well. Research has shown that higher-cost active funds such as unit trusts usually fail to beat their index targets over the long term once investment costs are factored in.

Despite their higher costs in the form of higher Total Expense Ratios (TER), the unit trusts we examined actually underperformed comparable exchange traded funds (ETFs) that cover the same sector. Clearly, investors who purchase unit trusts are faced with higher costs but not necessarily better returns than their peers who invest in ETFs tracking the same indices.

Your investment cost is one of the few variables you can directly influence. Do consider your cost of investing and evaluate if your investment returns commensurate with what you are paying for.

#5. Stay invested

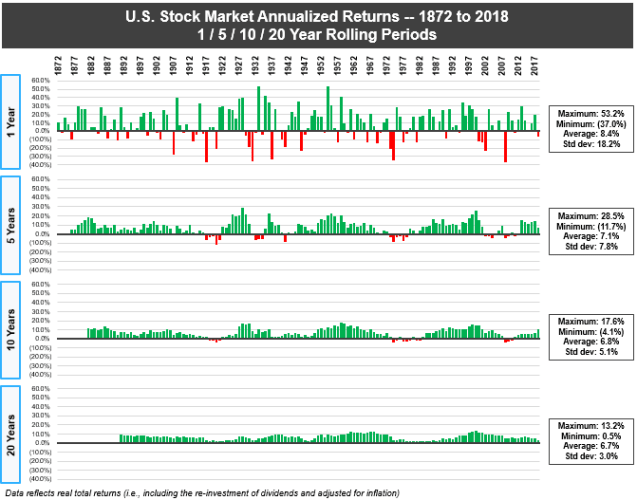

Successful investing is ultimately a matter of staying the course, even during periods of extreme volatility. History proves that panic-selling during a downturn almost always ends poorly for investors.

Over any 20-year period, the U.S. stock market has never lost money. To be sure, an investor taking a one-year view would have a higher probability of losses since there were several years (e.g. 2001, 2002, 2008) that the market went down. Over longer time horizons however, the wild swings of the market are reduced. In fact, the average annual returns over a 20-year period stands at about 6.7%.

The stock market has historically favoured investors who take a long-term approach. With average returns trending positive over longer horizons, it pays to commit to a long-term investing strategy and stay invested, even if stock market returns can vary greatly from year to year.

Adapted from Syfe’s personal finance e-book, Take Charge Of Your Wealth

You must be logged in to post a comment.