For many people, becoming a millionaire feels increasingly out of reach.

The rising cost of living, property prices, and everyday expenses can make wealth-building seem reserved for ultra-high earners or those who got lucky investing early in the right assets.

But in reality, most millionaires don’t build wealth overnight—they do it gradually through consistent investing, disciplined financial habits, and giving their money enough time to compound.

You don’t necessarily need a high salary to get to $1 million. Starting early, staying consistently, and letting compounding do the heavy lifting can take you to the same destination.

Time in the Market Matters More Than Timing the Market

One of the biggest misconceptions about investing is that perfectly timing the market will achieve better outcomes.

However, historical data has proven that time in the market matters more. This is because investing benefits from compounding, where your returns begin generating returns of their own. Over time, this creates a snowball effect that can significantly accelerate portfolio growth.

The following example illustrates how much you need to invest monthly to reach $1M, given an 8% annualised return:

| Investment Period | Monthly Investment Needed to Reach $1M |

| 35 years | ~$450 |

| 30 years | ~$670 |

| 25 years | ~$1,050 |

| 20 years | ~$1,700 |

| 15 years | ~$3,200 |

| 10 years | ~$5,500 |

Illustrative estimates only. Returns are not guaranteed and actual outcomes will vary.

This means that someone who starts investing at 35 will need to invest more monthly than someone who started at 25 in order to reach the same goal. This is the advantage of starting early and staying invested for the long term.

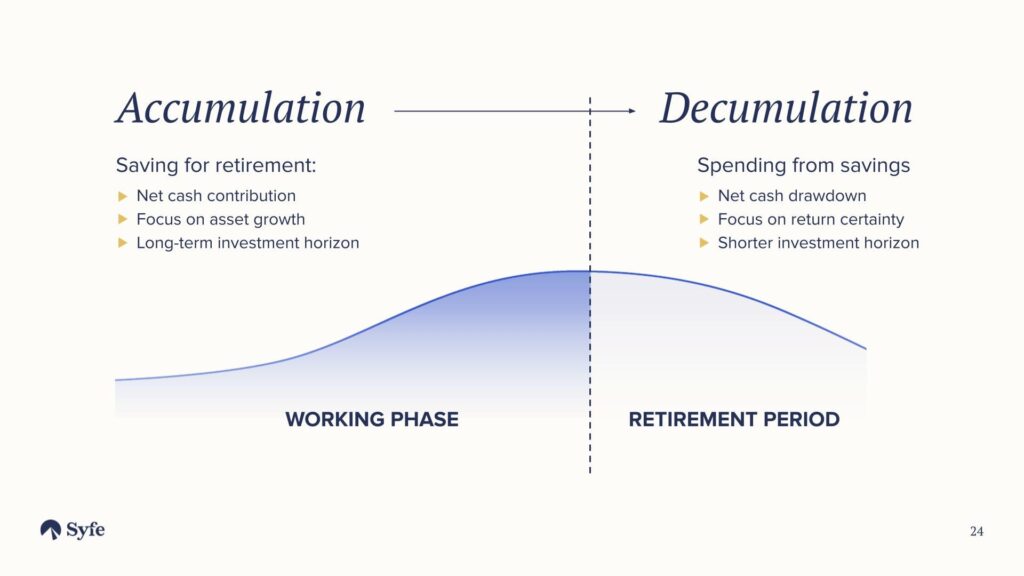

The Three Stages of Wealth Building

Building long-term wealth often evolves through three distinct phases.

1. The Accumulation Phase

This is the starting point for most investors, who are often beginning their careers.

At this stage, your portfolio growth is driven primarily by contributions rather than investment returns. The focus should be on building healthy financial habits like living below your means, investing consistently, avoiding unnecessary debt, and staying invested through market cycles.

For younger investors, time is your greatest asset. This means your portfolio can afford to lean more heavily toward growth-oriented assets like equities.

2. The Compounding Phase

As your portfolio grows over your working phase, investment returns begin contributing more meaningfully to overall wealth accumulation.

This is where compounding becomes increasingly powerful. At a certain point, your portfolio may even begin generating more annual growth than your yearly contributions, and wealth accumulation starts to feel noticeably easier as your money gains traction.

3. The Decumulation/Preservation Phase

As investors approach major life milestones like retirement, financial independence, or wealth transfer, their portfolio strategy would shift towards capital preservation and income generation.

This may involve diversifying income streams, reducing portfolio volatility, increasing bond exposure, prioritising liquidity and downside protection. The right allocation depends on individual goals, timelines, and risk tolerance.

Why Asset Allocation Matters

When people think about investing, they often focus on individual stocks. But research has consistently shown that asset allocation is more effective for long-term portfolio performance than stock picking.

Put simply, how you divide your portfolio across different asset classes matters more than finding the next winning stock.

A well-diversified portfolio typically spreads exposure across:

- Global equities

- Bonds and fixed income

- Cash or cash management solutions

- Alternative assets (where necessary)

Each asset class serves a different purpose.

| Asset Class | Purpose | Characteristics |

| Equities | Long-term growth | Higher return potential, higher volatility |

| Bonds | Stability and income | Lower volatility, defensive characteristics |

| Cash | Liquidity | Stability and flexibility |

| Alternatives | Diversification | May reduce portfolio correlation |

For long-term investors with decades ahead of them, equities have historically delivered the strongest returns over time. But they also experience periods of significant short-term volatility.

This is why diversification is important. A diversified portfolio helps reduce concentration risk and smooths returns across different market environments.

The Importance of Staying Invested

One of the biggest risks to long-term wealth building isn’t market volatility, but investor behaviour. Many investors panic during market downturns and sell at precisely the wrong time.

Historically, some of the market’s strongest recovery days have occurred shortly after major selloffs. Missing just a handful of these days can significantly impact long-term returns.

This is what often happens during market corrections: markets decline sharply, investor sentiment weaken, and panic selling ensues. But long-term investors who stay invested would benefit during recovery.

While volatility can feel uncomfortable, it is also a normal part of long-term investing. The key is building a portfolio aligned with your risk tolerance so you can remain invested through market cycles.

A Practical Framework for Building Wealth

For investors looking to build long-term wealth systematically, the process doesn’t need to be overly complicated.

Here’s a practical framework that many successful investors follow.

Step 1: Build an Emergency Fund

Before investing, ensure that you have sufficient liquid savings.

A common guideline is:

- 3–6 months of essential expenses for employees with regular salary

- 6–12 months for freelancers or variable-income earners

This creates a financial buffer and reduces the likelihood of needing to liquidate investments during emergencies.

Step 2: Automate Your Investments

It’s easier to stay consistent when your decisions are automated.

Setting up recurring monthly investments helps investors build discipline, reduce emotional decision-making, and benefit from dollar-cost averaging (DCA).

DCA is a tried-and-tested strategy that involves investing consistently regardless of market conditions. This helps to smooth purchase prices over time. For many investors, this is one of the simplest, hands-free ways to stay invested consistently.

To learn more about how DCA can help you build long-term wealth, read our guide here.

Step 3: Diversify

Rather than concentrating heavily in a few stocks or sectors, diversifying your portfolio provides exposure across global markets, reducing reliance on the performance of any single company, country, or industry.

Globally diversified investing also allows your portfolio to participate in growth opportunities beyond domestic markets.

Step 4: Increase Contributions Over Time

One of the most effective ways to accelerate wealth building is increasing investments as income grows. This reduces the time you need to achieve $1M. Even relatively small increases in monthly investing can meaningfully shorten the timeline to major financial goals.

Growing Wealth Through Long-Term Investing

At Syfe, we believe wealth management should be both structured and accessible. More investors increasingly recognise that successful investing is less about chasing trends and more about building resilient, diversified portfolios that grow over the long term.

That’s why many investors choose globally diversified portfolios like Core Equity100, which provides exposure to equities across developed and emerging markets. For more active investors, Equity Alpha (powered by J.P. Morgan Asset Management) is a better fit.

Rather than requiring investors to constantly monitor individual stocks, diversified portfolios help simplify long-term investing through:

- Broad global exposure

- Automatic portfolio management

- Dividend reinvestment

- Periodic rebalancing

For investors with long investment horizons and higher risk tolerance, equity-focused portfolios may offer stronger long-term growth potential, while more balanced portfolios (such as Syfe’s range of Core portfolios with their varying allocations to global equities, bonds, and commodities) can help manage volatility.

The important thing is choosing a strategy you can remain committed to through changing market conditions.

Wealth Building Is Rarely Linear

Investing journeys are rarely smooth. There will be periods where markets decline, portfolios fluctuate, and headlines create uncertainty. But historically, long-term investors who stayed disciplined through multiple market cycles were often rewarded over time.

Instead of predicting every market move or timing your entry, building a sustainable system—earning consistent income, saving and investing regularly, staying diversified and invested—and letting those habits compound over time is a more effective way of building wealth.

And while $1 million may once have sounded like an impossible milestone, long-term investing has made it increasingly attainable for ordinary investors willing to stay consistent.

The hardest part is often simply starting. The next most important part is staying invested long enough for compounding to do its work.

Read More:

How Dollar-Cost Averaging Builds Wealth Over Time

How and Where to Invest Your First $100K in Singapore – Your Step-by-Step Guide

The Best Passive Income Investments in Singapore

You must be logged in to post a comment.