As life expectancy extends and cost of living rises, should Singaporeans plan for a more expensive and longer retirement? We explore the concept of retirement planning beyond 1M65.

For years, the concept of 1M65—accumulating S$1 million by the age of 65—has been regarded as the benchmark for a comfortable retirement.

The theory is straightforward: build up a seven-figure nest egg through disciplined saving and CPF optimisation to enjoy a comfortable retirement. Many saw this as the magic number that would pretty much guarantee financial freedom once achieved.

However, the financial landscape has changed significantly over the past decade. Singaporeans are living longer, healthcare costs are rising, and inflation continues to redefine the cost of living.

This raises a critical question: Is S$1 million still enough to retire in Singapore today?

For many people, the answer may be no. As Syfe’s Senior Wealth Advisory Lead Jason Ang explains, “S$1 million today is only about S$400K 30 years later, assuming a 3% inflation rate. With longer life expectancies, an investor should plan for various possibilities to allow them more options in life.”

That doesn’t mean retirement is now unattainable, but that retirement planning today requires a broader strategy that combines CPF with diversified investments and long-term financial discipline.

In this article, we explore what the 1M65 movement entails, why S$1 million may no longer be sufficient for retirement, and how Singaporeans can build a larger, more resilient retirement portfolio.

Table of Contents

- What is the 1M65 movement?

- Why 1M65 may not be enough for retirement

- How much do you need to retire now in Singapore?

- How much do you need to retire in 30 years’ time?

- Investment strategy for a comfortable retirement

- A structured strategy beyond 1M65

- Conclusion

What is the 1M65 Movement?

The 1M65 movement, short for “S$1 million by age 65”, was popularised by CPF advocate Loo Cheng Chuan. The strategy demonstrates how Singaporeans can use the structure of the CPF system to accumulate a million dollars by the time they reach 65.

CPF plays an important role in Singapore’s retirement system. Members earn guaranteed interest on their balances:

- Special Account (SA): 4.0% per year

- Ordinary Account (OA): 2.5% per year

- Additional 1% interest on the first S$60,000 of CPF balances

These rates, particularly the 4% in the Special Account, are notably higher than what most risk-free instruments offer at home and abroad, including fixed deposits and T-bills. (At the time of writing, most Singapore banks are offering deposit rates of less than 2%. Even in the US, where rates have been held higher for longer, they are below 4%).

The basic idea behind the 1M65 strategy is straightforward. By maximising CPF contributions, transferring funds strategically into the Special Account, and allowing compound interest to work over several decades, individuals can gradually build their CPF balances to S$1 million by retirement.

For example, if someone accumulates around S$200,000 in their CPF Special Account by their mid-30s, the compounding effect at 4% over 30 years alone can grow that sum to roughly S$650,000 by age 65, even without further contributions. With continued CPF contributions from employment, the total could eventually reach the million-dollar mark.

This approach has several advantages:

- CPF interest is government-backed and stable

- Contributions are automatic through employment

- Compounding works quietly in the background over decades

Because of these characteristics, the 1M65 movement has helped many Singaporeans see that retirement planning does not have to involve risky, speculative investing.

However, while the strategy remains sound, the assumption that S$1 million is sufficient for retirement is increasingly being called into question.

Why 1M65 May Not Be Enough For Retirement

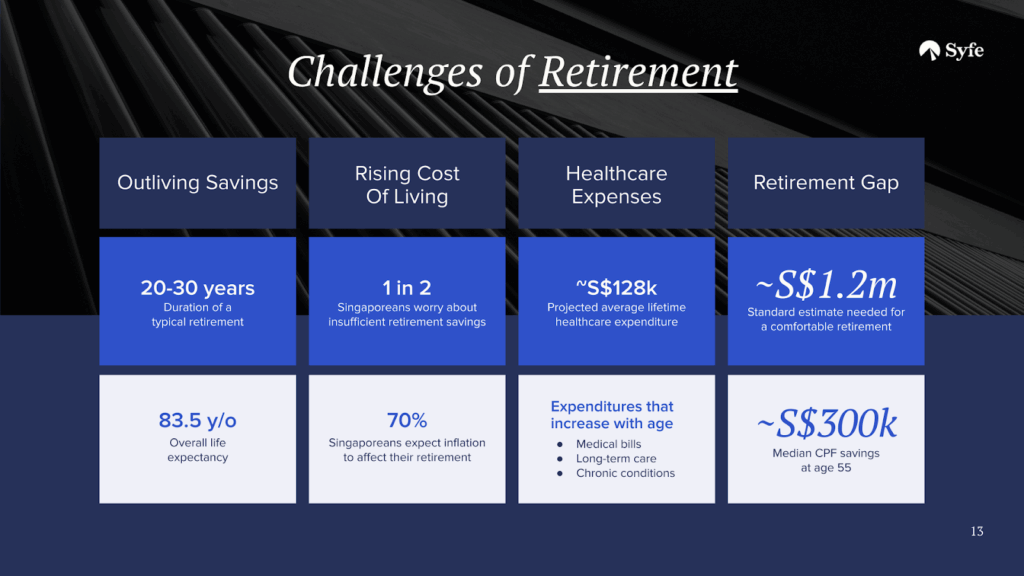

Reaching S$1 million in retirement savings is a significant milestone, for sure. However, retirement planning is not just about reaching a specific number, but about ensuring that your savings can support your desired lifestyle for two decades or more.

Several trends suggest that S$1 million may no longer stretch as far as it once did.

Longer Life Expectancy

Singapore has one of the highest life expectancies in the world. According to official statistics, life expectancy is now around 83 years (85.6 years for females and 81.2 years for males), and many Singaporeans will live well into their late 80s or even 90s.

If someone retires at 65 and lives until 90, their retirement savings must last 25 years.

Let’s look at how S$1 million translates into annual income.

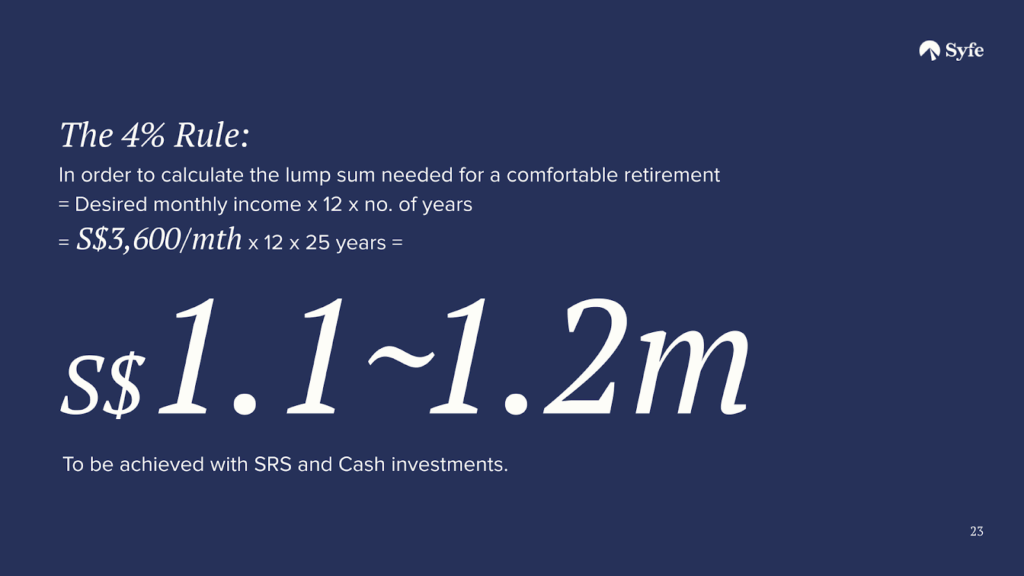

A commonly used guideline in retirement planning is the 4% withdrawal rule, which suggests withdrawing around 4% of your portfolio annually to make it last for decades.

Under this rule:

S$1,000,000 × 4% = S$40,000 per year in expenses (to last for 25 years)

That works out to about S$3,333 per month.

For some retirees with modest lifestyles who have paid off their mortgages, this may suffice. But for many households in Singapore, especially those who wish to maintain their current lifestyle, this amount may not be enough.

Rising Cost of Living

Inflation gradually erodes purchasing power over time.

Even a modest 3% inflation rate can significantly change the value of money over a long period of time. Over 25 years, prices could roughly double, which means that the lifestyle supported by S$3,000 per month today could require S$6,000 per month in the future.

Rising healthcare costs are also an important consideration. As retirees age, medical expenses typically increase, even with insurance and government support schemes. This adds to one’s monthly expenses.

Lifestyle Expectations

Retirement today looks very different from what it did decades ago. Many retirees hope for a lifestyle that involves spending more time travelling, pursuing hobbies, or supporting their children and grandchildren. Others may even want the option to dine out frequently, attend cultural activities, or pursue lifelong learning.

While these aspirations are understandable, they require greater financial resources.

As a result, the true retirement number for many Singaporeans today may be closer to S$1.5 million to S$2 million, rather than just S$1 million.

How Much Do You Need to Retire Now in Singapore?

While there is no single figure that works for everyone, we estimate using the traditional 4% rule that investors in Singapore intending to retire now would need approximately S$1.1-1.2 million now for a semi-comfortable retirement (S$3,600 per month for 25 years).

Do note that the 4% rule is an approximate guide that covers regular life expenses. However, if one requires more due to unforeseen circumstances (medical or family responsibilities), they should budget a bigger sum.

Aside from the 4% rule, another approach to retirement planning is considering your monthly expenses.

Suppose a retiree wants S$4,000 per month to cover living costs, leisure, and healthcare. That amounts to S$48,000 per year.

Using the same 4% withdrawal framework:

S$48,000 ÷ 4% = S$1.2 million

This S$1.2 million will last you 25 years into retirement.

How Much Do You Need to Retire in 30 Years’ Time?

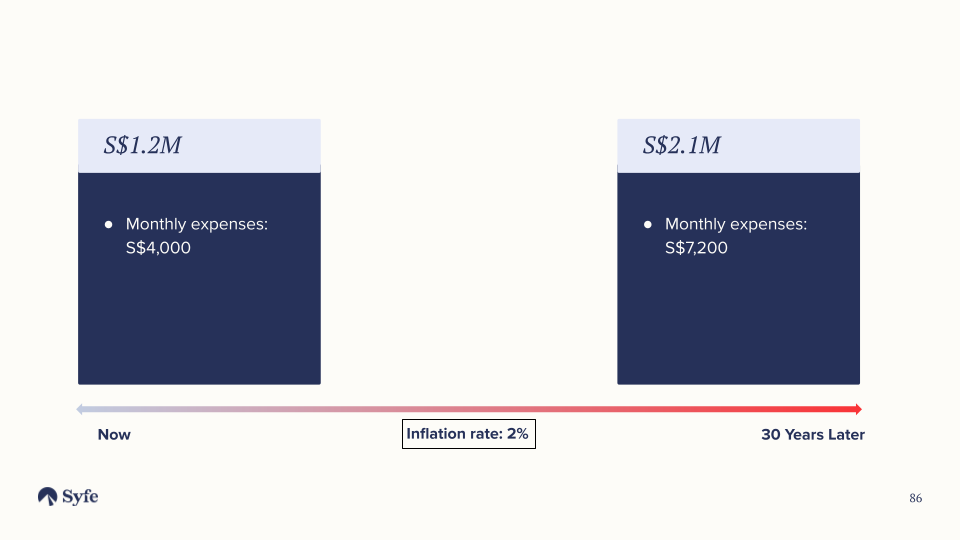

However, if you intend to retire in, say, 30 years, you might need more than S$4,000 a month as a result of inflation, in which case you’ll need more than S$1.2 million.

Retiring later means you will also need to take inflation into account.

In 30 years, given an annual 2% inflation rate, your S$4,000 monthly expenses will increase to about S$7,200.

To calculate the future cost of today’s expenses, we use the standard Future Value (FV) formula:

where:

Present Value (PV): $4,000 (your current monthly expenses)

Annual Inflation Rate (r): expressed as 0.02

Time Horizon (n): 30 years

So to calculate the monthly required sum using the formula,

With a 2% annual inflation rate, your current monthly expenses of S$4,000 will increase to S$7,245.45 in 30 years.

If the desired monthly income rises to S$7,200, the required retirement portfolio then rises to about S$2.16 million.

These numbers can seem intimidating at first glance. But the key takeaway should not be that retirement has become unattainable, but that having multiple sources of retirement income can help to close the gap.

Investment Strategy for a Comfortable Retirement

If S$1 million may no longer be enough to retire, then how can Singaporeans build a larger retirement fund?

The answer does not lie in timing the market or taking speculative bets. For a more sustainable approach, you may wish to consider a structured portfolio that complements CPF.

CPF provides a strong, stable foundation through guaranteed interest and lifelong payouts via CPF LIFE. But to keep pace with inflation and meet your retirement needs, you will need a multi-layer portfolio, where each component plays a different role: growth, income, stability, and liquidity.

Read Also: CPF Changes in 2026: What They Mean for Your Retirement — and Why CPF Alone May Not Be Enough

Growth Engine: Global Equities

A key driver of long-term wealth is exposure to global equity markets.

Historically, equities have delivered higher long-term returns than many other asset classes as investors participate in the growth of businesses around the world. Over long investment horizons, global equities have often produced average returns ranging around 6–8% annually, although actual returns may vary year to year.

Globally diversified portfolios such as Syfe’s Core portfolios can help investors capture this growth potential. They invest across thousands of companies globally, and some of them include a mix of bonds and commodities for diversification. This can serve as your primary growth engine in a retirement strategy.

Suppose an investor contributes S$500 per month into a diversified growth portfolio that averages 6% annual returns over the long term.

After 30 years, that portfolio could grow to a little more than S$477,000, where most of the final value comes from compounding investment returns over time. This means that even individuals who start with modest monthly investments can gradually build a substantial portfolio, especially if they begin early.

When paired with CPF savings, a global equity portfolio can supercharge the growth in retirement funds and beat inflation over the decades.

Income Stability: Global Bonds

While equities are essential for growth, retirement portfolios also benefit from more stable assets that provide more predictable income.

This is where fixed-income investments, such as bonds, come in.

A globally diversified bond portfolio like Syfe Income+ invests across a wide range of bond markets, including government bonds, corporate bonds, and other income-generating instruments.

Because they come with lower risks, bonds typically offer lower returns than equities. But they provide several key benefits for long-term investors:

- They tend to be less volatile than stocks

- They generate regular income through coupon payments

- Seen as safer than stocks, they are often in demand during equity market downturns. Their presence can help stabilise your portfolio

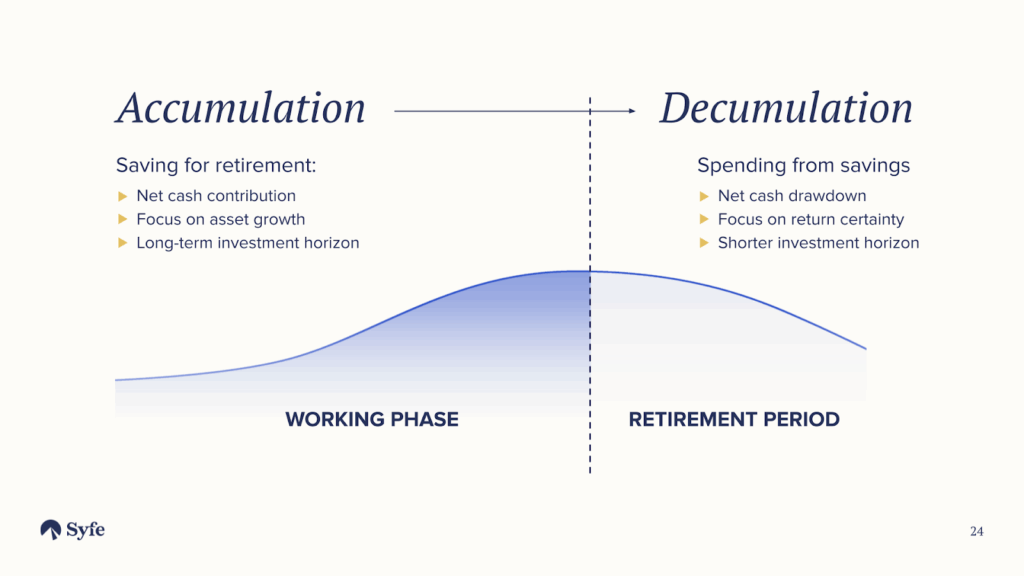

As you approach retirement, what we call the decumulation phase, you would want to gradually increase your allocation to bonds to protect the wealth you have already accumulated.

For instance, someone in their 20s to early 40s might focus heavily on growth portfolios. But as retirement draws closer, slowly shifting part of the portfolio toward bonds can help create a steady stream of income to complement CPF LIFE payouts.

Income Generation: REITs

Another asset class that many Singaporean investors appreciate is real estate investment trusts (REITs).

REITs allow investors to get a piece of property assets such as office buildings, shopping malls, logistics facilities, and data centres, without needing to purchase physical real estate. REITs are special in that they behave both like equities and bonds – investors buy shares in a “trust” vehicle that holds the real estate, and that trust makes regular payments to investors. Historically they have been known for their relatively attractive dividend yields compared to bonds.

Singapore has the largest REIT market in Asia (ex-Japan), with 38 traded Singapore REITs (S-REITs) and Property Trusts and a total market capitalisation of approximately S$100 billion.

A portfolio like Syfe REIT+ focuses specifically on Singapore-listed REITs, providing exposure to the local real estate sector and the potential for consistent income distributions. For retirement planning, REITs can serve as an additional income-generating component alongside bonds.

Liquidity and Inflation Protection: Cash Management

Apart from growth and stability, every retirement plan needs flexibility and liquidity.

A cash management solution such as Syfe Cash+ can help address this need. By allocating funds into diversified cash and short-term fixed-income instruments, it aims to generate potentially higher yields than traditional savings accounts while keeping risk relatively low.

Cash management portfolios aren’t the most exciting assets in an investment portfolio, but they serve several purposes in a retirement strategy:

- Provide a buffer for short-term needs, such as emergency expenses or upcoming major purchases.

- Serve as a temporary holding place for funds before they are invested into longer-term portfolios through dollar-cost averaging, or even deployed to take advantage of market dislocations.

- For retirees, cash allocation can help cover short-term spending needs without requiring withdrawals from your investments. This helps you stay invested during market downturns, which is the key to generating long-term wealth.

A Structured Strategy Beyond 1M65

When CPF and long-term investments work in tandem, they can form a comprehensive retirement strategy that goes beyond the traditional 1M65 framework.

CPF remains the foundation, providing guaranteed interest and lifelong income through CPF LIFE. On top of that, diversified investments help to grow wealth and generate additional income streams. It can even offer additional flexibility for discretionary expenses (such as travel) and unexpected costs while managing risks such as inflation and market volatility.

For instance, someone who accumulates S$700,000 in CPF balances and S$1 million in an investment portfolio would have a retirement pool of S$1.7 million.

A possible long-term structure might look something like this:

- CPF savings providing lifelong monthly payouts

- Core portfolios driving long-term growth through global equities

- Income+ portfolios generating stable income from bonds

- REIT+ exposure delivering property-related dividend income and growth

- Cash+ reserves offering liquidity and inflation protection

This structure reframes retirement planning—away from a prescriptive goal like 1M65 and toward a more sustainable strategy that supports decades of retirement living.

Conclusion

The 1M65 movement has played an important role in getting Singaporeans to think deeper about retirement planning and their retirement needs. It also shows how disciplined saving and the power of compounding can build a solid foundation for retirement.

But the reality is that in 30 years S$1 million may no longer be enough for many retirees, especially after accounting for longer lifespans, inflation, and healthcare costs.

Instead of asking “How do I earn $1 million by 65?”, asking “How much will my desired lifestyle cost in 30 years?” may help you develop a more comprehensive retirement strategy.

By combining CPF with diversified investments and consistent long-term contributions, you can build a sustainable retirement portfolio that not only exceeds the 1M65 target, but also allows you to live the life you want for decades.

Explore how Syfe can help you in your retirement planning today.

Read More:

- Can You Earn S$1 Million By 65? A Deep Dive Into Singapore’s 1M65 Movement

- Your Retirement Planning Checklist: Are You on Track?

- How and Where to Invest Your First $100K in Singapore – Your Step-by-Step Guide

- How Much Do You Need to Retire in Singapore?

- 5 Things Singaporeans In Their 50s Should Be Doing For A More Secure Retirement

- Top SRS Investment Options to Grow Your Retirement Savings

You must be logged in to post a comment.