Retirement may feel like a distant goal, especially if you’re still young. But with rising living costs and longer life expectancies, planning early has never been more important.

Retirement may feel like a distant goal, especially if you’re still young. But with rising living costs and longer life expectancies, planning early has never been more important.

A solid retirement plan should be holistic and realistic, one that aligns with your life goals, accounts for evolving needs, and taps into the right investment tools to grow your wealth over time.

Whether you’re just starting out or entering your golden years, this guide will walk you through key checkpoints to ensure your retirement is on track.

Why You Shouldn’t Leave Retirement Planning for “Someday”

Many Singaporeans believe that they will need over S$1 million to retire comfortably. The good news? You don’t need to save it all at once. Thanks to the power of compounding, starting early—even with small monthly amounts—gives your money more time to grow.

Benefits of starting early:

- Maximise long-term market returns through dollar-cost averaging

- Build flexibility to adjust your investment strategy over time

- Enjoy peace of mind knowing your future income streams are being secured

A head-start can potentially double your returns from the same initial investment. The earlier you begin, the less you need to catch up later.

Your Retirement Planning Checklist

A sound retirement strategy involves balancing long-term goals with short- and mid-term priorities, such as mortgage payments, children’s education, and travel plans.

Here’s a checklist and action plan for you to gauge your performance and stay on track.

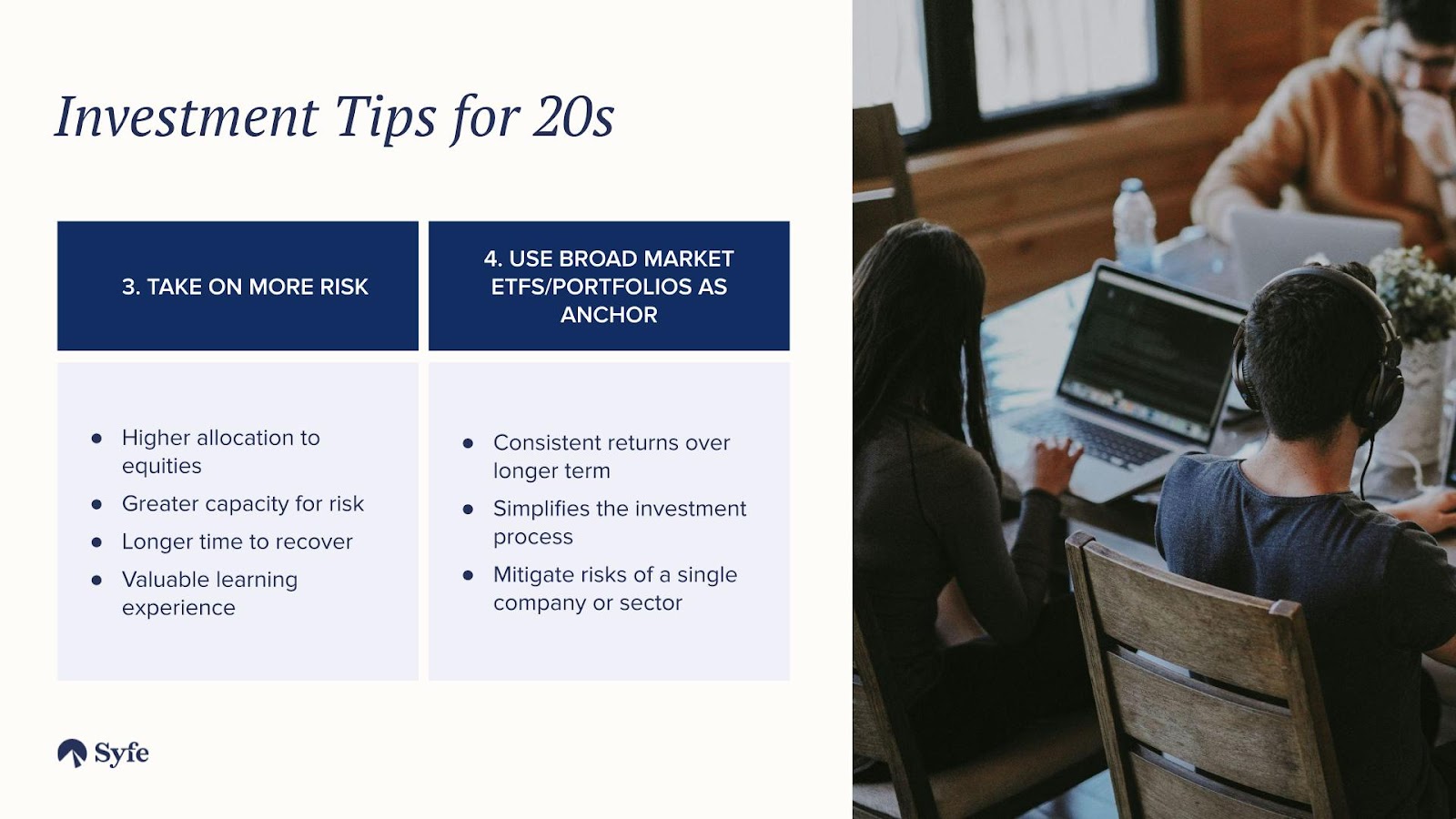

How to Start Retirement Planning in Your 20s and 30s

At this stage, you’re likely focused on laying the groundwork for your future, be it advancing in your career, paying off education loans, saving for a home, or building an emergency fund. Retirement might not seem urgent when you’re juggling present-day needs, but this stage is critical for setting strong foundations for your financial life.

This is what your checklist may look like:

In Your 20s–30s: Build Strong Foundations

| Category | Checklist |

| CPF | Understand CPF structure (OA, SA, MA) Start voluntary top-ups to SA (enjoy tax relief + compounding) |

| Emergency Fund | Build 6–12 months of essential expenses in savings |

| Insurance | Get adequate insurance (Integrated Shield Plan) Consider term life insurance if you have dependents |

| Investing | Start investing early (e.g. ETFs, REITs, robo-advisors, SRS) Learn basics of diversification and risk |

| Career | Focus on skills upgrading and salary growth |

| Housing | Plan early for BTO/Resale HDB Understand CPF housing usage limits |

| Mindset | Set retirement as a long-term goal Automate monthly savings and investments |

The greatest advantage you have right now is time. The earlier you start, the more time your money has to grow. Even modest amounts invested consistently over many years can grow into a substantial retirement nest egg due to the power of compounding.

Starting early also means you won’t have to contribute as much later or take on as much risk to reach the same goal.

Your action plan

- Define a retirement goal: Think in terms of when you want to retire and what lifestyle you envision. A rough savings target can help you work backwards.

- Start investing early: Time in the market beats timing the market.

- Build good habits: Set up automatic transfers into a long-term investment portfolio monthly.

- Keep learning: Understand basic investment concepts like compounding, risk tolerance, and asset allocation.

Building the habit of saving and investing regularly now creates financial discipline that will benefit you at every stage of life.

A diversified, equity-based portfolio is often ideal for long-term investors at this age, since you have time to ride out market volatility.

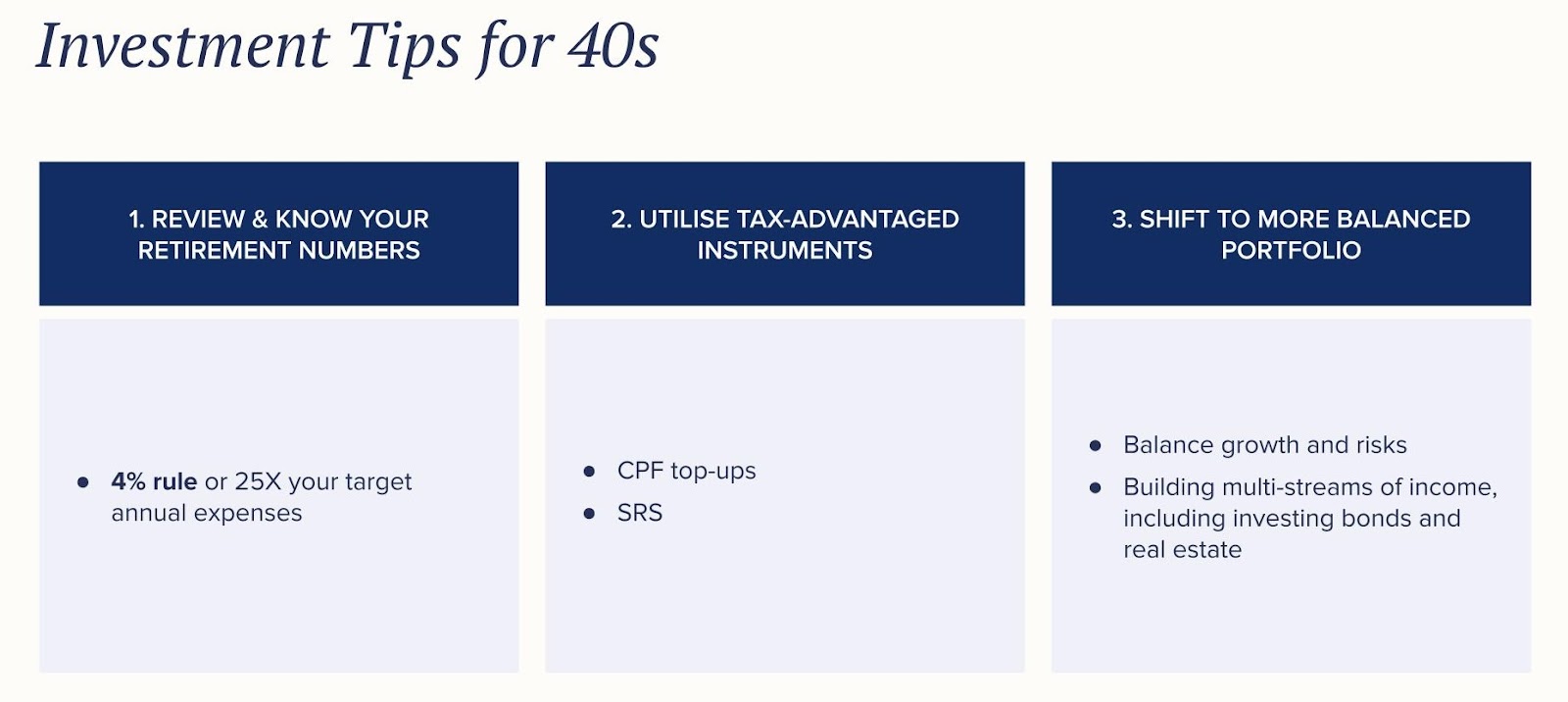

Retirement Planning Strategies in Your 40s

At this stage, you’re likely in your prime earning years and juggling multiple responsibilities—raising children, paying down a mortgage, caring for ageing parents, or supporting a dual-income household.

Competing priorities can make it hard to dedicate resources toward retirement. Still, your financial decisions now will have a significant impact on your quality of life in later years.

In Your 40s: Accelerate and Protect

| Category | Checklist |

| CPF | Track CPF balances vs Retirement Sum Consider top-ups to SA/RA and parents’ CPF (for tax relief) |

| Insurance | Review coverage for life, critical illness, and dependents |

| Kids / Education | Plan for children’s education without compromising your retirement |

| Investments | Shift to a balanced portfolio (some risk but growing stability) Maximise SRS contributions (up to $15.3K/year for tax relief) |

| Housing | Clear mortgage progressively Consider future right-sizing if appropriate |

| Estate Planning | Make CPF nominations and write a will |

Time is still on your side, but the window to maximise your retirement savings is narrowing. This is the stage where you can accelerate your investments, course-correct if you started late, and take a more strategic approach to your financial planning.

It’s also a good time to reassess your risk tolerance and begin balancing growth with stability. The actions you take now—increasing your savings rate, diversifying your portfolio, and reviewing your financial goals—can help close any gaps and set you up for a more secure retirement.

Your action plan

- Reassess your goals: Update your retirement timeline and target based on current circumstances.

- Diversify your investment strategy: Consider a mix of growth and income-focused assets to strike a balance between building wealth and protecting it.

- Boost your savings rate: If your income has increased, aim to contribute a higher percentage to your long-term investments.

- Plan around other goals: Consider how your children’s education or housing needs might affect your retirement timeline.

How to Prepare for Retirement in Your 50s

Now, you may be thinking about when to retire, how much you’ll need, and whether you’re financially ready. If you have children, their education costs might still be ongoing, and you could be planning for healthcare, downsizing your home, or exploring lifestyle changes. Your risk appetite may be shifting as the margin for recovery from market downturns shortens.

In Your 50s: Consolidate and Prepare for Payouts

| Category | Checklist |

| CPF | Aim to meet Full Retirement Sum (FRS) Explore CPF LIFE options (Standard vs Escalating) |

| Healthcare | Ensure MediSave has sufficient balance Purchase CareShield Life supplements if needed |

| Investments | Review portfolio for income generation (dividends, bonds, annuities) Gradually reduce exposure to high-risk assets |

| Housing | Consider downsizing or monetising HDB via Lease Buyback Scheme (LBS) |

| Retirement Budget | Project monthly expenses and identify reliable income sources |

| Withdrawal Plan | Strategise when and how to draw from SRS, CPF LIFE, and other assets |

| Legacy Planning | Finalise will, CPF nomination, and LPA (Lasting Power of Attorney) |

This is the decade to sharpen your plan. You’ll want to start estimating your retirement expenses, testing your portfolio’s readiness, and exploring ways to turn your savings into sustainable income.

The emphasis moves from aggressive growth to a more balanced approach that includes income generation and capital preservation. Strategic adjustments now—like reallocating assets, reducing unnecessary debt, and reviewing insurance—can go a long way in securing your retirement income later.

Your action plan

- Calculate your income needs: Start estimating how much you’ll need monthly in retirement and for how many years.

- Shift to a more balanced portfolio: While growth is still important, reducing risk becomes a priority.

- Test your plan: Create a mock retirement budget to check if your savings and investments can support your desired lifestyle.

- Explore income-generating investments: Portfolios that offer monthly payouts or dividend income can help bridge the transition from salary to retirement income.

Be sure to keep some flexibility in your plan, as you may retire earlier (or later) than expected due to personal or economic reasons.

How to Manage Your Money After Retirement

You’ve either retired or are about to. Your priorities have shifted from building wealth to managing withdrawals and ensuring your money lasts. With more free time and fewer work-related obligations, lifestyle considerations (travel, part-time work, volunteering, or spending more time with family) become front and centre. However, you might still have financial concerns around healthcare costs, inflation, and market volatility.

Retirement and Beyond: Maintain, Withdraw, and Preserve

| Category | Checklist |

| Income Strategy | Set up regular withdrawals from CPF LIFE, SRS, and other income sources |

| Cash Flow | Maintain liquid reserves for unexpected expenses Monitor your spending to stay within budget |

| Healthcare | Keep health insurance and CareShield Life up to date Plan for long-term care needs and medical inflation |

| Investments | Keep a conservative portfolio with some exposure to low-risk growth |

| Estate Planning | Review and update your will, CPF nomination, and LPA periodically |

| Family & Legacy | Communicate your wishes to loved ones |

Your portfolio is now your main source of income, not your salary. That means your focus should shift to ensuring financial sustainability while preserving capital. Without a proper withdrawal strategy, you risk depleting your savings too quickly.

At the same time, leaving everything in cash could lead to your wealth losing value over time. Finding the right balance between income generation, liquidity, and low-risk growth is essential to maintain your lifestyle and keep pace with inflation. This stage also requires thoughtful planning around estate matters, healthcare coverage, and your legacy.

Your action plan

- Structure your withdrawals: Allocate funds across short-, medium-, and long-term horizon buckets to manage liquidity and risk.

- Take note of inflation: Even in retirement, your money needs to continue growing in order to maintain its purchasing power over time.

- Maintain an emergency fund: Having readily accessible savings can prevent you from needing to sell investments during downturns.

- Review your estate plans: Make sure your will, nominations, and other documents are up to date.

Investing doesn’t stop when you retire; your strategy just changes. Aim for a balance of income, safety, and slow growth.

Common Retirement Planning Mistakes to Avoid

- Delaying your investment journey: The longer you wait, the more you’ll need to save later to catch up.

- Underestimating inflation: Leaving too much in cash can reduce your future purchasing power.

- Ignoring healthcare planning: Unexpected medical costs are one of the biggest retirement risks.

- Not reviewing your plan regularly: Life circumstances change. Your plan should evolve too.

- Focusing only on returns: A high return doesn’t help if it comes with volatility you’re not prepared to manage.

Final Thoughts: A Retirement Plan That Works for You

There’s no one-size-fits-all solution to retirement planning. But wherever you are in life, the core principles remain the same:

- Start as early as possible

- Invest consistently and wisely

- Adjust your strategy as your needs change

The good news is: You don’t have to figure it out alone. Syfe offers a suite of managed portfolios that can support your retirement goals, whether you’re looking for growth, income, or a mix of both. From building long-term wealth to generating steady payouts, we’re here to help you make confident financial decisions at every stage of your journey.

Ready to take the next step? Explore our retirement investing guide or speak with one of our wealth advisors to craft a plan that works for you.

Read More:

- How and Where to Invest Your First $100K in Singapore – Your Step-by-Step Guide

- How Much Do You Need to Retire in Singapore

- 5 Things Singaporeans In Their 50s Should Be Doing For A More Secure Retirement

- Top SRS Investment Options to Grow Your Retirement Savings

- Guide to Supplementary Retirement Scheme (SRS) in Singapore: What It Is and How to Maximise It

- CPF vs SRS Top-Ups: Which to Choose and What’s the Difference?

- Income Tax Relief: 5 Ideas to Lower Your Payable Tax in Singapore

You must be logged in to post a comment.