Bond markets have been anything but calm. Long-term yields have surged, headlines scream volatility, yet Syfe’s Income+ portfolios have quietly held their ground. While popular bond ETFs like TLT fell sharply, Income+ Preserve and Enhance portfolios delivered steady income and positive returns. In this update, we break down what’s driving bond market moves, why it’s not a meltdown, and how Income+ portfolios continues to offer stability and opportunity in today’s environment.

Table of Contents

- Why Are Long-Term Yields Rising

- How Worried Should Investors Be

- Not All Rates Are Equal

- Where to Invest in Bonds Now

- Why Bonds Still Have a Role

- Income+ vs Bond ETFs

- Compared to Buying the Funds Directly

Why Are Long-Term Yields Rising

Long-term government bond yields have climbed sharply due to a mix of structural and cyclical pressures. First, fiscal concerns: ballooning government deficits, especially in the US and Japan, have spooked investors. Second, lower demand from traditional buyers like central banks, foreign investors and insurers has weighed on bond prices. Lastly, investors are demanding more risk premium, which has been historically suppressed. Together, these forces are pushing long-term yields higher, even as short-term rates plateau.

How Worried Should Investors Be

This is not a bond market meltdown, but more of a wake-up call. While headlines may sound alarming, it’s important to keep perspective. Unlike emerging markets, both the US and Japan issue debt in their own currencies, which gives them far more flexibility. This makes a sovereign default extremely unlikely, as they retain the ability to service their obligations through monetary tools.

What we’re seeing now is an orderly repricing of long-term risk, not a collapse. The sell-off has been concentrated mainly in long-term government bonds, while other segments like investment-grade credit have held up well.

Markets are demanding higher yields to compensate for fiscal uncertainty and shifting supply-demand dynamics. But bond sentiment can turn quickly. If governments show signs of restoring fiscal discipline, or if economic growth starts to moderate, yields could stabilise or even fall.

Not All Rates Are Created Equal

It’s also crucial to distinguish between short-term and long-term interest rates. Short-term interest rates are shaped by central bank policy, while long-term interest rates reflect concerns around fiscal health and inflation risk.

Even as long-term rates rise, short-term rates are anchored and likely to decline. Markets are expecting two to three Fed cuts by early 2026. This means the front-end of the yield curve could stay anchored. In the current environment, short-to-intermediate bonds are preferred as they offer attractive yields and lower volatility.

Where to Invest in Bonds Now

Focus on high-quality bonds with intermediate duration. Investment-grade corporates and agency mortgage backed securities (MBS) offer yields above 5% with relatively low credit risk.

Meanwhile, intermediate-duration bonds (5 to 7 years) hit the sweet spot, offering most of the yield with less price volatility than long-duration bonds. These segments benefit from both carry income and potential price appreciation if rates ease. It’s about earning steady income while keeping duration risk in check.

Why Bonds Still Have a Role

Bonds are no longer just the “safe” part of a portfolio — they’ve become a powerful income engine in their own right. Over $60 trillion in global bonds now yield above 4%, a dramatic shift from just a few years ago when yields were near zero.

In fact, high-quality investment-grade bonds today offer more than four times the income of the S&P 500 dividend yield, which currently stands at around 1.3%.

Beyond attractive income, bonds provide four key benefits for investors:

- Consistent Cash Flow: Regular coupon payments support steady income, especially valuable in uncertain markets.

- Capital Preservation: High-grade bonds can help protect your capital when equities sell off.

- Diversification: Bonds typically behave differently from stocks, helping to reduce overall portfolio volatility.

- Potential Price Gains: If interest rates decline, bond prices usually rise — offering a source of capital appreciation in addition to income.

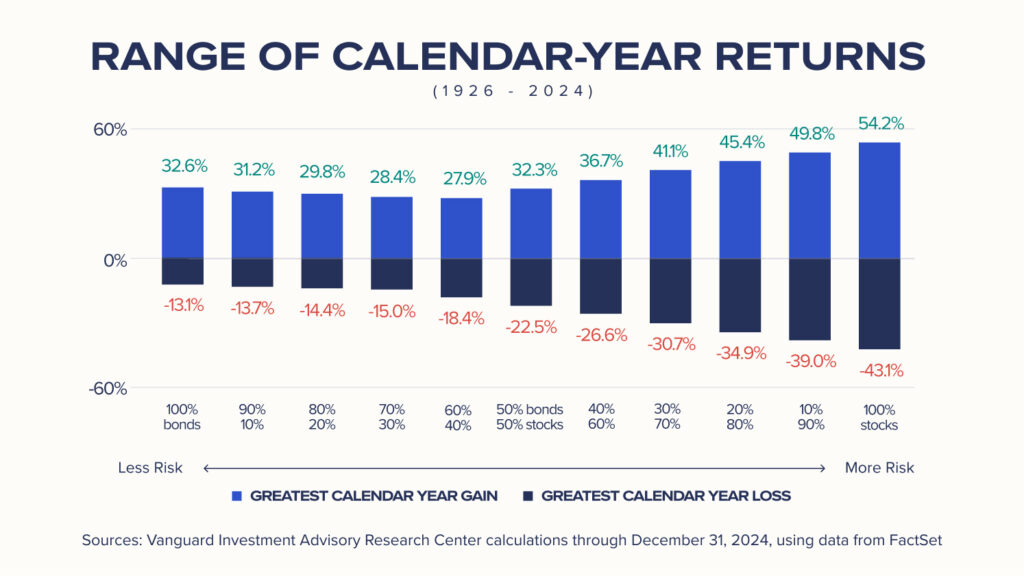

Historically, balanced portfolios that include bonds have delivered better risk-adjusted returns than those relying solely on equities. For instance, a 60/40 equity-bond mix has often matched much of the upside of stocks, while greatly lowering the downside risk of the portfolio.

Why Income+ ?

Syfe’s Income+ portfolios are built for this environment. Powered by PIMCO, they offer exposure to diversified, high-quality global bonds — with active management that responds to market shifts.

- Preserve targets monthly payout yield of 5.0% – 5.5% p.a., average credit rating of A+, and has 5.9-year duration.

- Enhance targets monthly payout yield of 5.5% – 6.0% p.a., average credit rating of A- rating, and has 5.0-year duration.

Income+ vs Bond ETFs

Income+ has several advantages over bond ETFs, making it a better option for income-focused investors.

- Actively Managed: Income+ uses PIMCO funds that are actively managed. This means experts choose from a wide range of bonds to help get steady income with less risk. Most ETFs are passive and can’t adjust easily to market changes or income needs.

- Lower Taxes: Dividends are a big part of income. The funds in Income+ are based in Ireland, which helps Singapore investors save up to 30% on dividend taxes compared to US-based ETFs.

- SGD-Hedged for Stability: Income+ invests in SGD-hedged funds to reduce currency risk. In contrast, USD ETFs without hedging can lead to ups and downs in your SGD income.

Compared to Buying the Funds Directly

With Income+, you get access to top-quality institutional funds at a much lower cost. Investors can save up to 60% in fund fees compared to buying the same funds on their own as retail investors.

Start Earning Smarter Income Today. Enjoy institutional-quality bond strategies, lower fees, and more stable payouts with Income+. Invest now or speak to our team to learn more.

Read More:

You must be logged in to post a comment.