Singapore Savings Bonds (SSB) have continued to provide returns pretty handsomely over the past year, thanks to persisting high interest rates.

If you had bought an SSB issue in September 2022, your average annual return would have been 2.8%. However, if you purchased the September 2023 issue, you would be enjoying an average annual return of 3.06%. The only downside in this kind of scenario is that to get higher returns, you would need to spend time and effort again on buying these bonds. Not to mention the risk of not even getting full allotment due to oversubscription. That’s what the investors of the April 2023 tranche faced.

Are the Singapore Savings Bonds a good place for your spare cash? What are some alternatives to SSB to consider? We’ve got you covered.

Singapore Savings Bonds: Worth buying?

Singapore Savings Bonds are one way to earn a better return on your cash savings, as compared to bank deposits. SSB have a maximum tenure of 10 years, and interest rates go up for each year that you remain invested.

As details from the current October 2023 tranche show, you’ll receive 3.05% in average returns if you hold the bond for one year, but 3.16% in average annual returns overall if you stay invested for 10 years.

| Year from the issue date | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Interest | 3.05% | 3.05% | 3.05% | 3.05% | 3.05% | 3.05% | 3.10% | 3.36% | 3.48% | 3.48% |

| Avg return per year | 3.05% | 3.05% | 3.05% | 3.05% | 3.05% | 3.05% | 3.06% | 3.09% | 3.13% | 3.16% |

That said, you can sell your SSB at any time, without penalties for exiting early. You’ll get a pro-rated interest on your withdrawal amount. However, do note that your proceeds will only be credited to you on the 2nd business day of the following month. So it’s best to plan ahead if you need urgent access to your cash.

Another restriction is that you need to invest a minimum of $500 and can only buy SSB in multiples of $500. Likewise, you can only redeem your SSB in multiples of $500. For each redemption request, you’ll be charged a $2 transaction fee by the bank.

An alternative to Singapore Savings Bonds

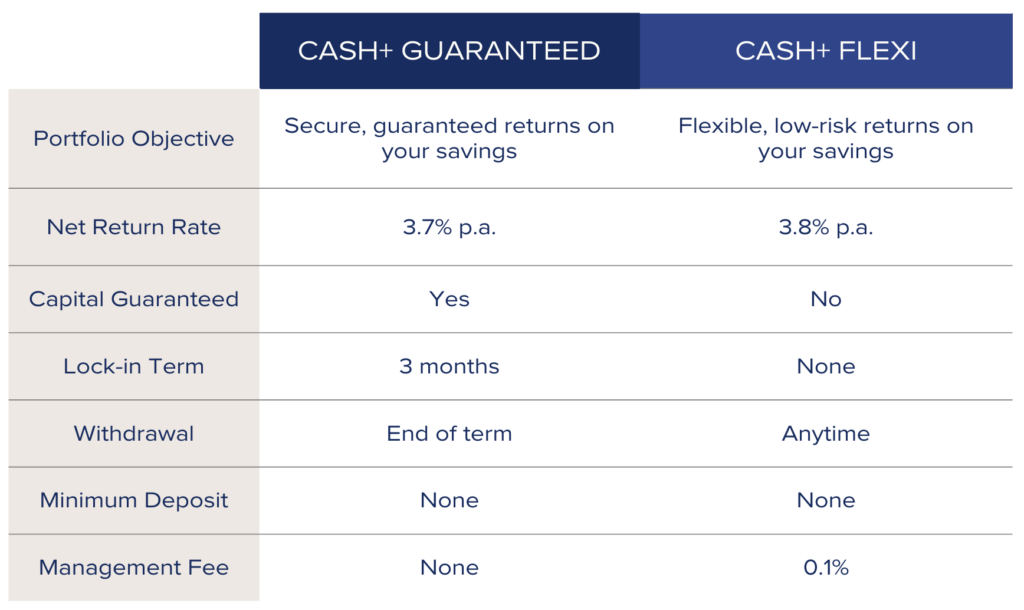

Singapore Savings Bonds are not the only way to make the most of your savings. Cash management solutions like Syfe Cash+ Flexi and Cash+ Guaranteed can be an attractive alternative to SSB.

While Syfe Cash+ Flexi currently offers a projected return of 3.7% p.a.with high liquidity, Syfe’s latest launch, Cash+ Guaranteed, can get you guaranteed returns of 3.8% p.a. on your idle cash for a 3-month lock-in period.

The best part? At a time when interest rates remain on the high side, the projected yield will be updated to reflect the general interest rate environment.

For instance, the projected return for Cash+ Flexi was changed from 2.4% p.a. to 3.7% p.a. over the last 12 months.

| Cash+ Flexi | H1 2022 | H2 2022 | Q1 2023 | Q2 2023 | Q3 2023 |

| Projected Net Returns (p.a.) | 1.2% | 2.1% | 3.1% | 3.5% | 3.7% |

| Actual Net Returns (p.a.) | 1.3% | 1.9% | 1.7% | 3.1% | 3.5% (QTD as of end Aug’23) |

Similarly, Cash+ Guaranteed will give you optimised returns at competitive fixed rates on your cash by collaborating with MAS-regulated banks so that you don’t have to move your money around.

There is also no minimum investment needed for either Syfe Cash+ Flexi or Cash+ Guaranteed, unlike Singapore Savings Bonds.

If you prefer to maintain liquidity, Cash+ Flexi is a more flexible option. Most importantly, withdrawals are quick and free. You can receive your proceeds just the next day and there are no fees for making a withdrawal.

But if you are more risk averse and want your capital guaranteed, and you have no problem with a short lock-in period of three months, Cash+ Guaranteed is an apt choice. Here’s a quick overview of Syfe Cash+ Flexi and Cash+ Guaranteed and a comparison with SSB.

Here’s a quick overview of Syfe Cash+ Flexi and Cash+ Guaranteed and a comparison with SSB.

Make the most of your idle cash

Though the inflation is now cooling down, the interest rates are expected to remain high till the second quarter of next year.

In a high-interest regime, Singapore Savings Bonds and alternatives like Syfe Cash+ Flexi and Cash+ Guaranteed can be a smarter choice to earn high returns for your spare cash.

For SSB, you’ll first need to have a bank account with DBS/POSB, OCBC or UOB, as well as a CDP account. Thereafter, you can apply for SSB issues via ATM or internet banking. Take note that a $2 transaction fee will be levied on each application. Finally, check for your SSB allotment on the 3rd last business day of the month.

Want a faster and easier option? You can consider Syfe Cash+ Flexi or Cash+ Guaranteed.

You don’t need a CDP account and there are no transaction fees involved for either of them. In fact, they have zero fees.

Within 1 – 2 business days, your money will be invested in your Cash+ Flexi or Cash+ Guaranteed portfolio and you can start earning returns daily.

Unlike Singapore Savings Bonds, there’s no risk of an oversubscription too. Your funds will be fully invested each time you add to your portfolio.

You must be logged in to post a comment.