Riding the wave of strong earnings and a post-election market surge, Singapore’s banking giants – DBS (SGX:D05), OCBC (SGX:O39) and UOB (SGX:U11) – are making headlines with their record-breaking stock prices. But is this the right time to buy? And if so, which bank offers the most compelling opportunity?

To answer this, let’s dive into their latest quarterly results to understand more about the health and potential of these banking behemoths.

Total Income and Net Profit Growth (Winner: DBS)

When examining the growth prospects, DBS stands out with its impressive performance. For the quarter, DBS’s total income surged by 11%, while its net profit jumped by an impressive 15%. The bank’s diverse businesses are firing on all cylinders, with strong growth across net interest income, trading, and wealth management.

While UOB and OCBC also reported robust growth, DBS emerged as the clear leader in this metric. One notable area of strength this quarter for all three banks was trading income, which saw year-over-year growth ranging from 70% to 135%. This highlights the banks’ ability to capitalise on market opportunities and diversify their income streams.

Asset Quality (Winner: OCBC)

The non-performing loan (NPL) ratio is a key indicator of a bank’s asset quality, measuring the proportion of loans that are likely to go bad. Lower NPL ratios generally indicate a healthier loan portfolio and stronger financial health.

In this regard, all three Singapore banks continue to demonstrate robust asset quality. DBS’s NPL ratio improved from 1.1% to 1.0%, signaling resilient asset quality. UOB maintained a stable NPL ratio of 1.5%, while OCBC’s NPL ratio showed further improvement, declining to 0.9%, the lowest among the three.

These figures suggest that all three banks have effectively managed their credit risk and maintained strong underwriting standards.

Return on Equity (Winner: DBS)

Return on equity (ROE) is a crucial measure of a bank’s profitability, indicating how effectively it generates profits from its shareholders’ investments. A higher ROE signifies not only a more efficient use of capital, but also stronger returns for investors.

In this area, DBS shines. With an impressive ROE of 18.8%, it boasts the highest among the three banks. This performance represents a significant improvement from its 18.2% ROE in the previous quarter and highlights the bank’s continued focus on maximising shareholder value.

UOB also demonstrated strong performance, achieving a notable jump in its ROE. OCBC, meanwhile, maintained a respectable ROE of 14.1%.

Valuations (Winner: OCBC)

To gauge how expensively a bank is valued, a common metric is the price-to-book (P/B) ratio, which compares a company’s market valuation to its book value. Currently, all three banks’ valuations are above their historical averages, indicating that they may be slightly expensive.

However, comparing them to each other reveals some differences. OCBC, with a P/B of 1.27x, appears more attractively valued than UOB at 1.33x and DBS at 1.81x.

Dividend yield (Winner: OCBC)

If you’re an income investor who buys bank stocks primarily for their dividends, dividend yield is a crucial metric to consider. It measures the annual dividend payment relative to the current share price.

Looking at the trailing 12-month dividend yield (the total dividends announced over the past year divided by the current price), OCBC stands out with the highest dividend yield at 5.3%. DBS and UOB offer dividend yields around 4.7% and 4.9% respectively.

Beyond dividends, these banks also return capital to shareholders through share buybacks. DBS has established a S$3 billion share buyback program, and UOB has also indicated its intention to repurchase shares. This commitment to returning value to shareholders further enhances their appeal for income-focused investors.

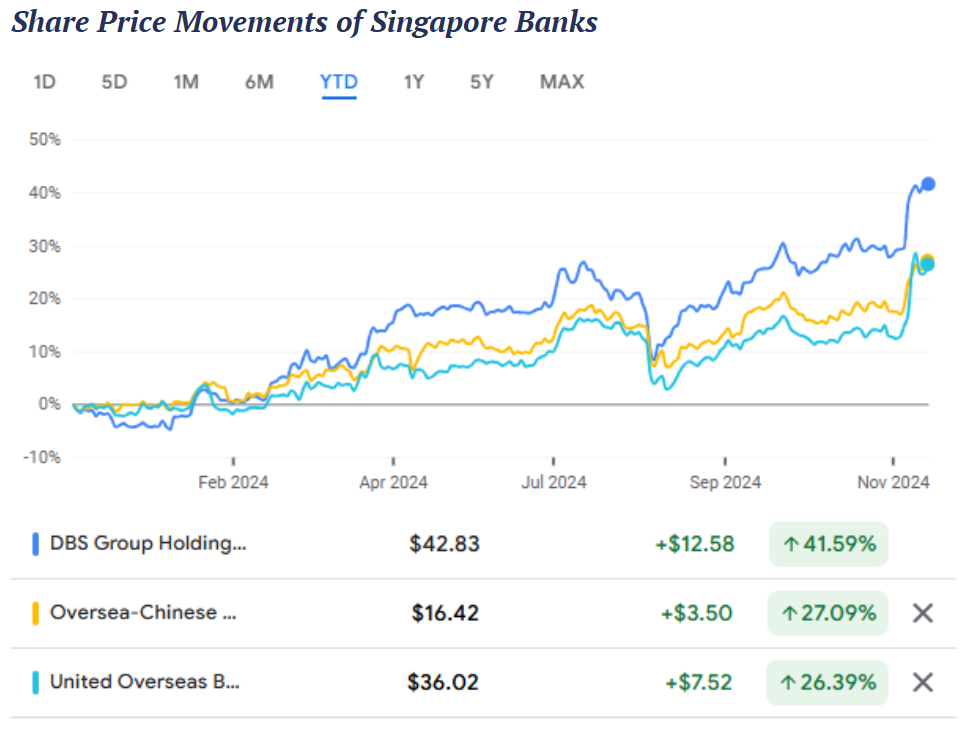

Price laggard YTD (Winner: UOB)

The three local banks have delivered strong returns year-to-date. Looking at price returns alone (excluding dividends), DBS leads the pack with a +41.6% gain, while OCBC and UOB trail slightly behind at +27.1% and +26.4%, respectively. This performance gap could suggest that there’s some room for OCBC and UOB to catch up.

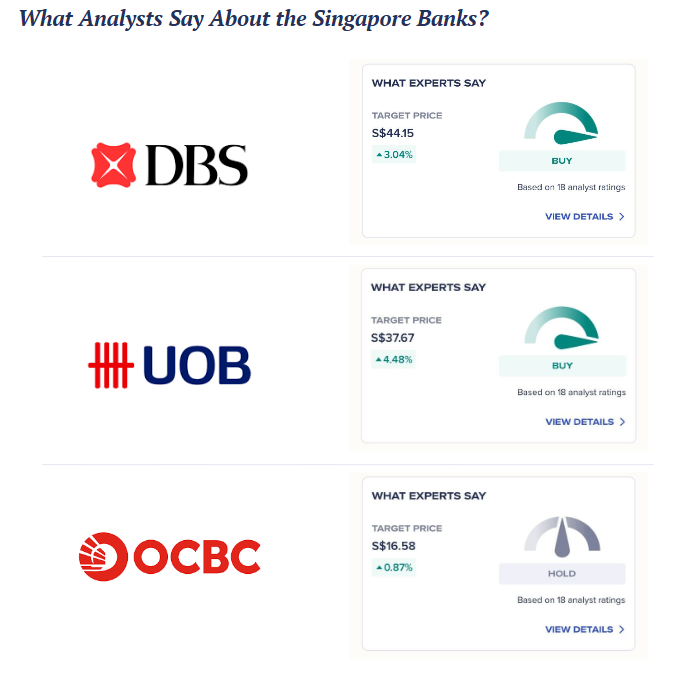

What do analysts say?

As you can see, picking a clear winner among the three banks is no easy task. Different metrics paint different pictures, with each bank excelling in certain areas. To gain further perspective, let’s take a look at what analysts are saying about these banks and their average target prices. Currently, among 18 analysts, the average rating for DBS and UOB is a “Buy,” while OCBC receives a “Hold” rating.

To gain more insights into these banks and conduct your own research, consider exploring Syfe Brokerage. Our platform puts key data at your fingertips, including analyst ratings, historical valuations, and more.

How to invest in DBS, OCBC and UOB

If you’re keen to gain exposure to Singapore banks, you can invest in them through a brokerage platform like Syfe Brokerage which offers access to both Singapore and US markets.

Syfe Brokerage is an easy and low-cost option for Singapore stock investing. Pricing for SGX stocks is just 0.06% of traded value (minimum S$1.98), and there are no platform and withdrawal fees.

Disclaimer: This article is for informational purposes only and should not be viewed as financial advice. It is not meant to market any specific investment, or offer or recommend the purchase or sale of any specific security. All forms of investments carry risks, including the risk of losing all of the invested amount. Such activities may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

You must be logged in to post a comment.