In this video, Ritesh Ganeriwal, Head of Investment and Advisory at Syfe, delivers a comprehensive ‘Investment Outlook for 2024’, examining the evolving landscape of investing in the year. As we navigate potential shifts in global financial trends, we delve into the key question: ‘Where to Invest in 2024?’

To access full report of Syfe Investor Trends and Outlook 2024 , please download it here.

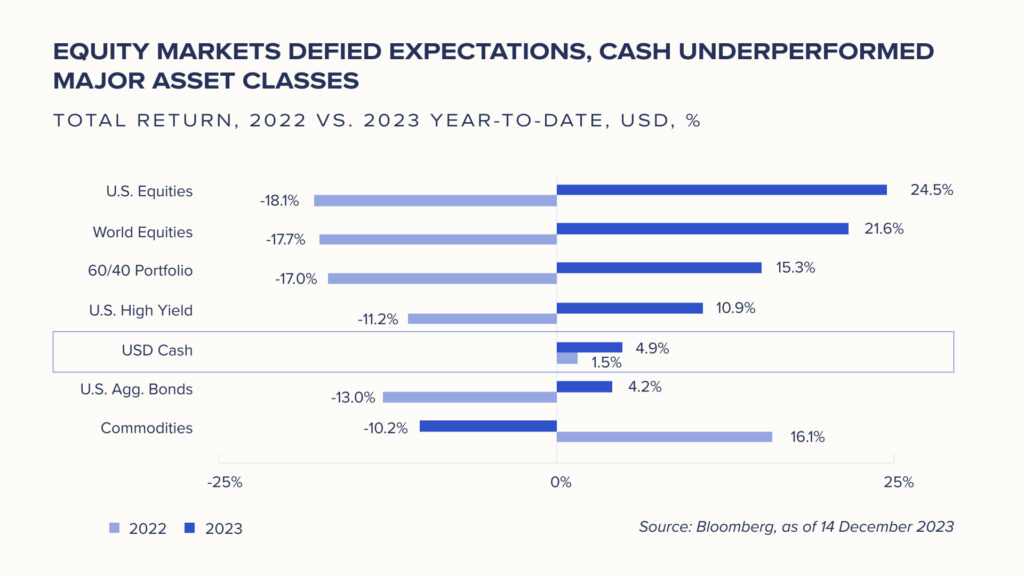

2023 proved to be a year that defied everyone’s expectations. We saw a surprisingly robust US economy in the face of soaring bond yields, the stock markets closed near all-time highs propelled by the rise of generative AI and disinflation firmly took hold leading to a sharp drop in treasury yields by the end of the year as the FED finally turned dovish.

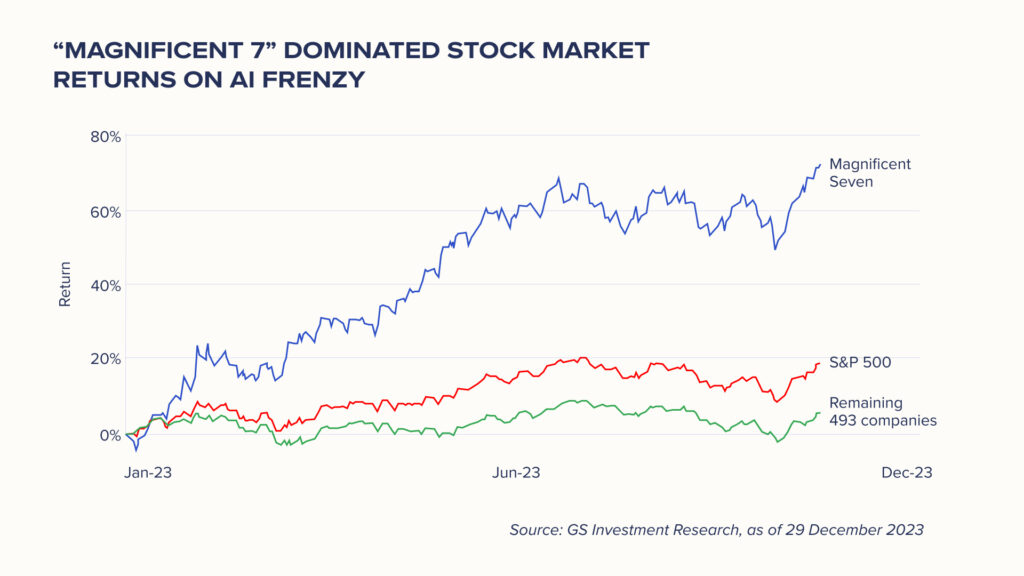

On the equities side, the S&P 500 bounced back by more than 24% in 2023 while the tech-heavy Nasdaq rose by 43%, one of its strongest performances in over two decades. However, the bulk of stock market gains was dominated by a handful of Mega-cap tech stocks on the back of an AI boom with the “Magnificent 7” contributing to over 70% of S&P 500 returns.

Notably, cash underperformed many asset classes. Most investors who held onto excess cash missed the opportunity to capitalise on the market rally as they remained cautiously underweight in risky assets in anticipation of an impending recession that never really materialised.

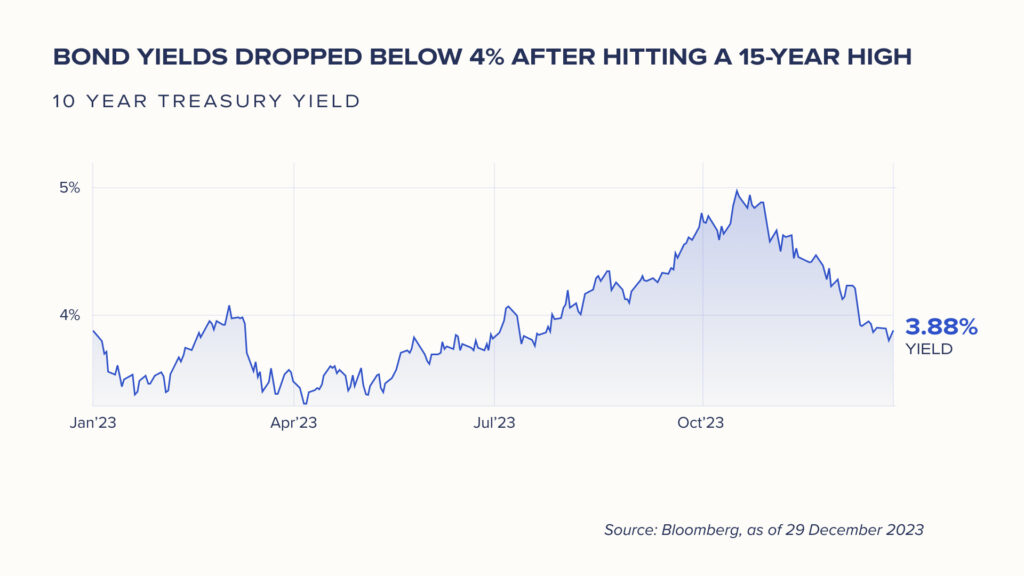

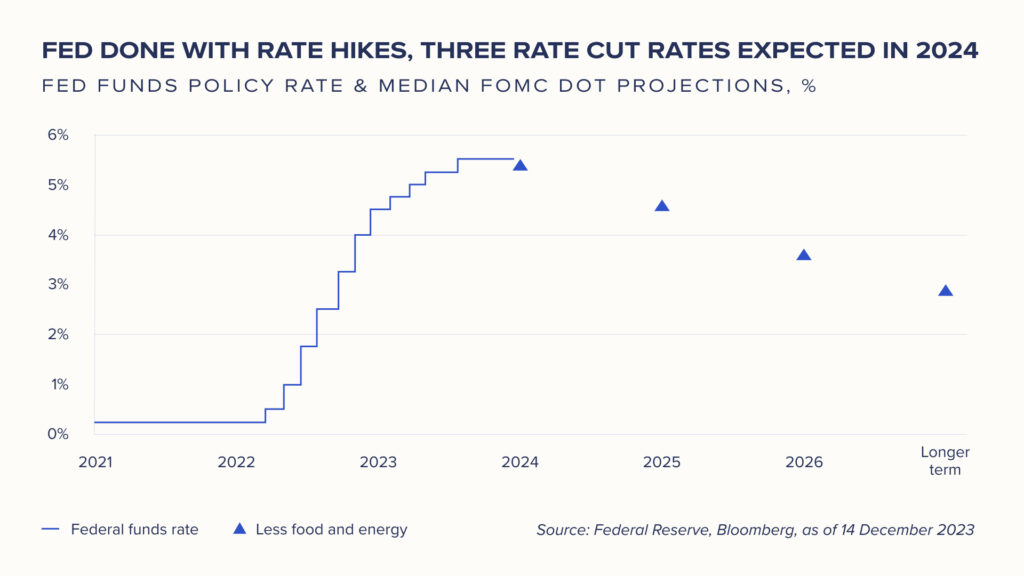

On the rates front, the FED finally halted its rate hiking spree and signaled rate cuts in 2024 as more consistent disinflationary trends emerged. This led to a whipsaw effect in interest rates with the 10-year US treasury yield moving from 3.5% to a high of 5% by October and then subsequently dropping to 3.9% towards the end of the year with the FED dovish pivot.

Looking ahead, while the global economic growth is expected to slow down in 2024, the possibility of a deep recession looks unlikely as inflation continues to moderate and the FED looks set to cut rates in the second half of this year.

We see the following key themes for 2024:

1. Holding excess cash exposes you to reinvestment risk

Currently, cash still offers attractive yields. However, as central banks begin to cut rates, reinvestment will yield lower returns. We encourage investors to consider allocating excess cash to bonds, REITs and equities, which could potentially offer higher returns above inflation in the long term.

2. The bond market offers compelling opportunities

Yields on USD core Investment Grade bonds have reached around 6%, a peak not witnessed since 2009. With the expectation of stabilising and then decreasing rates, these bonds offer an attractive mix of potential gains and lower volatility compared to High Yield.

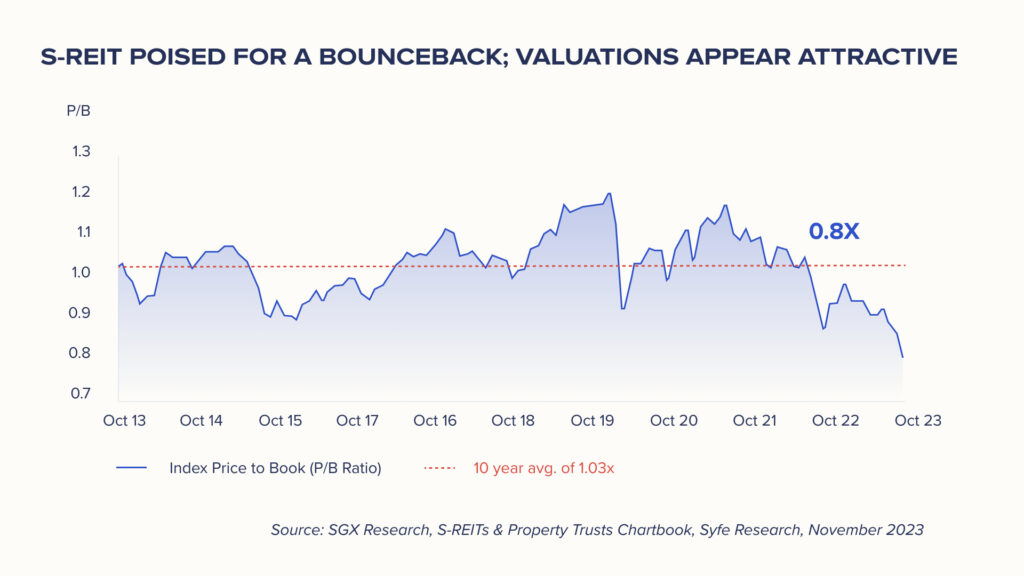

3. S-REITs stand poised for a bounce back

Singapore REITs stand to benefit from falling interest rates through reduced financing costs. Currently, S-REITs are trading at an attractive valuation with a price-to-book ratio of 0.8X, close to a 10-year low.

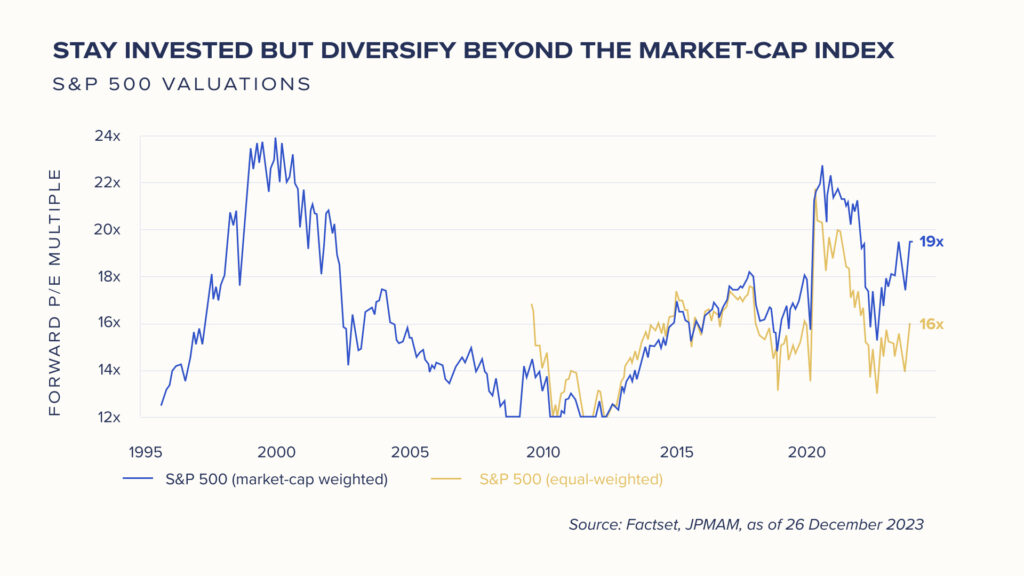

4. Stay invested but diversify

On the equities front, we favor a more diversified approach in 2024. The US small-cap and equal-weight indices posted one of their biggest monthly gains in December in the last three years, after lagging the market-cap index most of the year. By diversifying into equal-weight ETFs as well as quality and defensive equity sectors, investors can more effectively manage a level of concentration risk in the S&P 500 that hasn’t been observed in 50 years.

5. Be opportunistic on Chinese equity markets

We encourage investors to remain opportunistic on Chinese equity markets. China’s overall economic growth is expected to remain soft, but the “new economy” sectors might offer pockets of opportunity, as their valuations appear attractive and they receive policy support.

As we transition into 2024, we are positioned at a critical juncture in monetary policy. With interest rates likely to moderate, the investment landscape is brimming with new opportunities. This year is anticipated to herald a transition from cash to a more diversified investment portfolio, including income offerings such as bonds and S-REITs as well as quality and defensive equity sectors.

You must be logged in to post a comment.