Key Takeaways

- 2024 showcased surprising resilience, defying recession fears and delivering robust returns across various asset classes.

- However, investors should brace for potentially volatile markets in 2025 as President Trump’s re-election and subsequent policy shifts introduce both opportunities and uncertainties.

- Despite the potential bumps ahead, we encourage investors to remain invested. The Fed’s flexibility and ability to respond swiftly to changing conditions, combined with the ongoing AI revolution, are expected to support continued economic growth and create compelling investment opportunities. At the same time, diversifying your portfolio remains crucial to enhancing its resilience in the face of shifting market dynamics.

Table of Contents

2025: Four Key Trends Shaping the Market

Trumponomics 2.0 – Present Dual Effects on the Economy and Market

Fed Actions – The “Fed put” is Still in Place

China – Navigate Both Internal and External Challenges

AI Evolution – Capex Goes Strong

A Surprisingly Resilient 2024

As we close the chapter on 2024, it is evident that the past year surpassed many expectations. At the start of 2024, some economists were preparing for the possibility of a US recession. However, we took a more optimistic stance, confident that the rapid advancements and growing investments in Artificial Intelligence (AI) would serve as a significant driver of growth. Even so, the resilience of the US economy exceeded expectations. Consumer spending held strong, while inflation eased as anticipated and the Federal Reserve (Fed) initiated a pivot toward lowering interest rates.

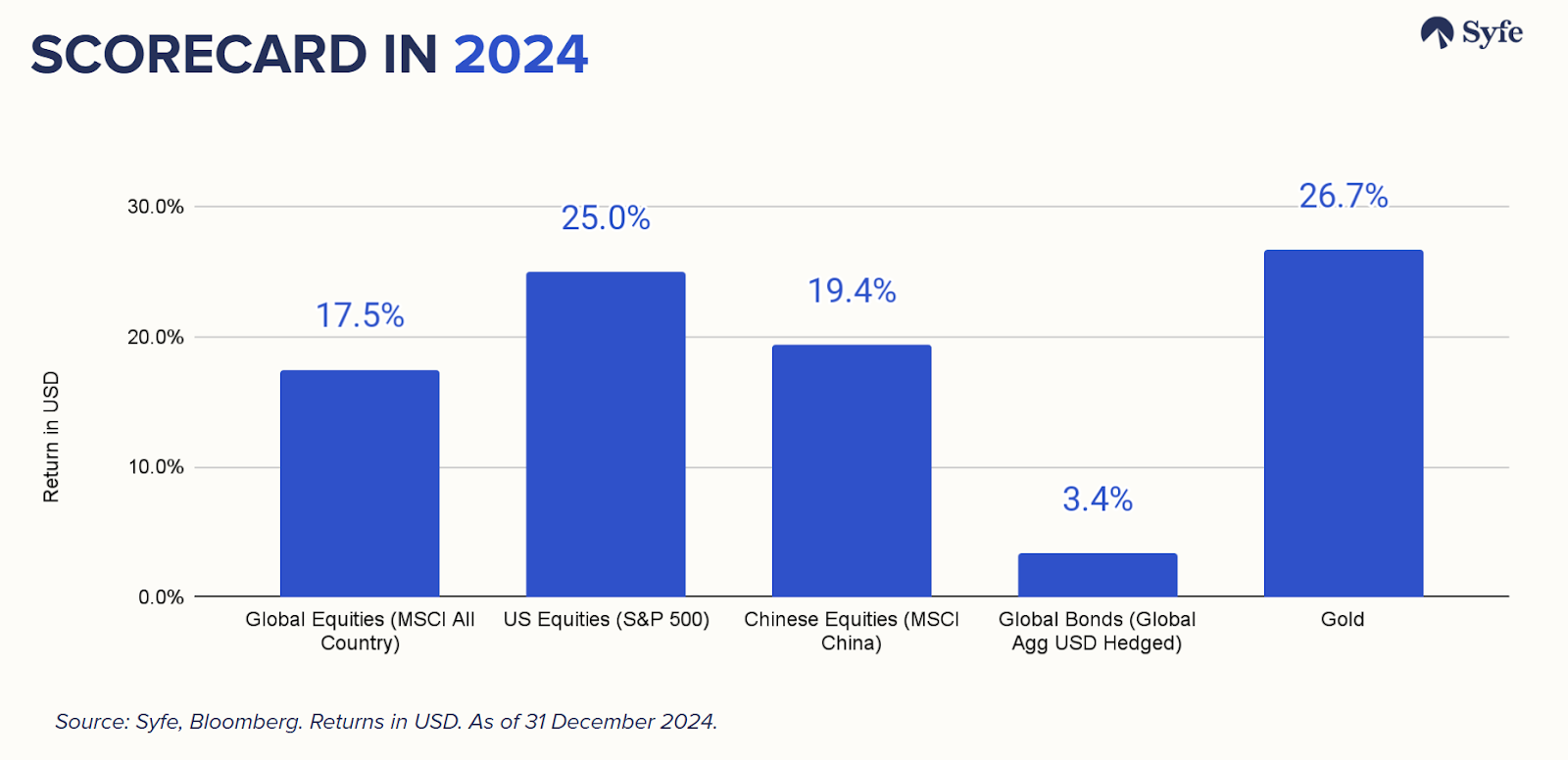

The outcome? A truly remarkable year across various asset classes. Global equities delivered impressive gains, with the MSCI All Country Index returning +17.5%. US equities, represented by the S&P 500, let with +25.0%, fueled by strong corporate earnings and breakthroughs in technological innovation. Even in the face of economic headwinds, Chinese equities, as measured by MSCI China, rebounded with a solid +19.4%.

It wasn’t just equities that stole the spotlight. Gold shone with a +26.7% gain as investors sought safe-haven assets amid geopolitical uncertainties. Global bonds delivered a moderate return of +3.4%. Although the Fed began cutting interest rates, long-term US Treasury yields moved higher following Trump’s re-election. Meanwhile, Bitcoin skyrocketed by an astonishing +122.5%, fueled by regulatory changes that boosted investor confidence.

It is a year that richly rewarded investors who not only stayed invested but also diversified strategically across a range of asset classes.

2025: Four Key Trends Shaping the Market

As we embark on 2025, the investment landscape is undergoing a transformation. We believe four key trends and their interplay will exert significant influence on market direction:

- Trumponomics 2.0: How will the return of Trump-era policies affect US growth and inflation, and what ripple effects might we see globally?

- Fed actions: Will the Fed maintain its easing stance, or will economic shifts prompt a change in direction?

- China’s policies and risks: Will Chinese policymakers adopt aggressive easing measures to stimulate growth amidst external risks like trade tariffs, or will they take a more cautious approach?

- The ongoing wave of AI investment: Will ongoing AI advancements continue to drive growth, or could new hurdles emerge in regulation and adoption?

We will delve deeper into these factors and their implications in the sections that follow.

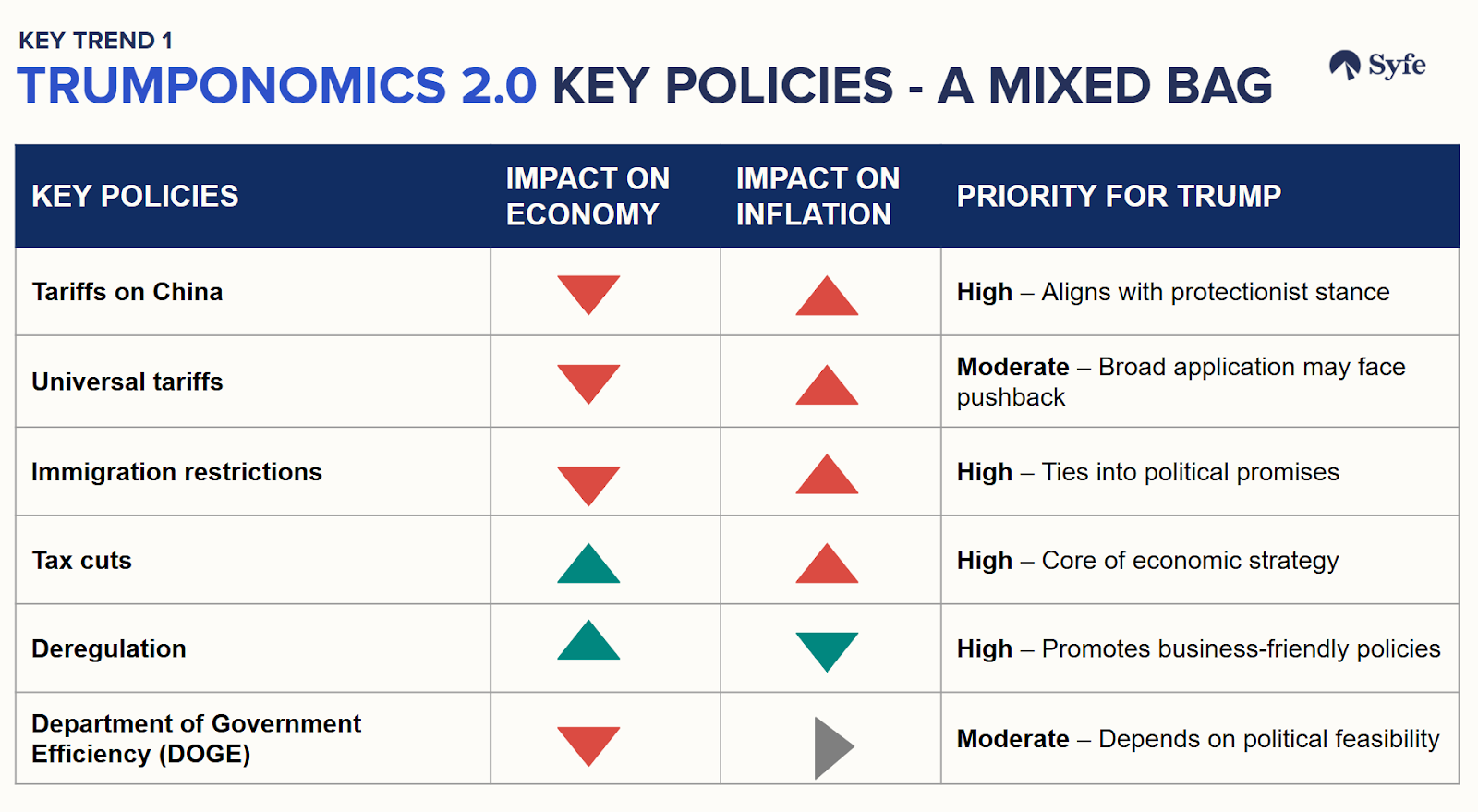

Trumponomics 2.0 – Present Dual Effects on the Economy and Market

Investors are keenly focused on the economic policies of Trump’s second administration. With Trump back in office for another four years and the Republican Party controlling both houses of Congress, implementing his policy agenda is expected to be far smoother this time around.

The table below outlines key potential policy measures and their anticipated impact on economic growth and inflation.

Trade policies: More trade tariffs and frictions are almost certain under Trump’s new term, though the specifics remain uncertain. Proposed measures include universal tariffs of 10–20%, steep tariffs of up to 60% on Chinese goods, and even 100% tariffs on countries moving away from the US dollar. These proposals underscore Trump’s broad and aggressive stance on trade.

A trade deal with China appears increasingly unlikely, as the US continues to use tariffs as a tool to curb China’s global influence and encourage supply chain diversification. Tariffs on Chinese goods could rise by an additional 20 percentage points, with non-consumer goods potentially facing even higher rates.

However, the likelihood of a universal tariff across all imports is considerably lower. In his first term, Trump has used bold tariff proposals more as a negotiating tactic than as concrete policy measures. The talk of a 10% universal tariff is more likely to be aimed at pressuring trade partners back to the negotiating table rather than signaling a firm intention to implement it.

| Tariffs and trade policy uncertainty could Reduce US GDP growth in 2025 by -0.6%Baseline US GDP growth forecast in 2025 of 2.2%. Reduce World GDP growth in 2025 by-0.3% Baseline World GDP growth forecast in 2025 of 3.2%. Source: International Monetary Fund World Economic Outlook, as of 11/6/2024. IMF trade war scenario assumes a 10% across the board tariff on all U.S. imports and full-scale retaliation by all countries. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. |

Immigration Restrictions: Trump’s strict immigration policy proposals are another significant concern, likely to take effect sooner than fiscal policy changes. These policies could have negative implications for US GDP growth by reducing the labor force. The inflationary impact is less certain; large-scale deportations could shrink the workforce, increasing demand for remaining workers and potentially driving up wages and inflation.

Tax cuts and deregulation: Despite the growth concerns introduced by trade policies and immigration, the tax cuts and deregulation could provide a strong stimulus to economic growth. There is potential that the combination of tax cuts and deregulation would boost the animal spirits in the US, driving higher investment and consumption.

IMPLICATIONS: The bottom line is that Trump’s potential policies present dual effects, offering both upside and downside risks to the economy and inflation, thereby adding significant uncertainty to the forecast. Throughout 2025, the news flow about Trump’s policies is likely to dominate the headlines and could swing sentiments, leading to a much bumpier ride than in 2024.

Fed Actions – The “Fed put” is Still in Place

As Trump’s potential policies could drive up inflation, the key question becomes how the Fed might respond to the changing economic forecast.

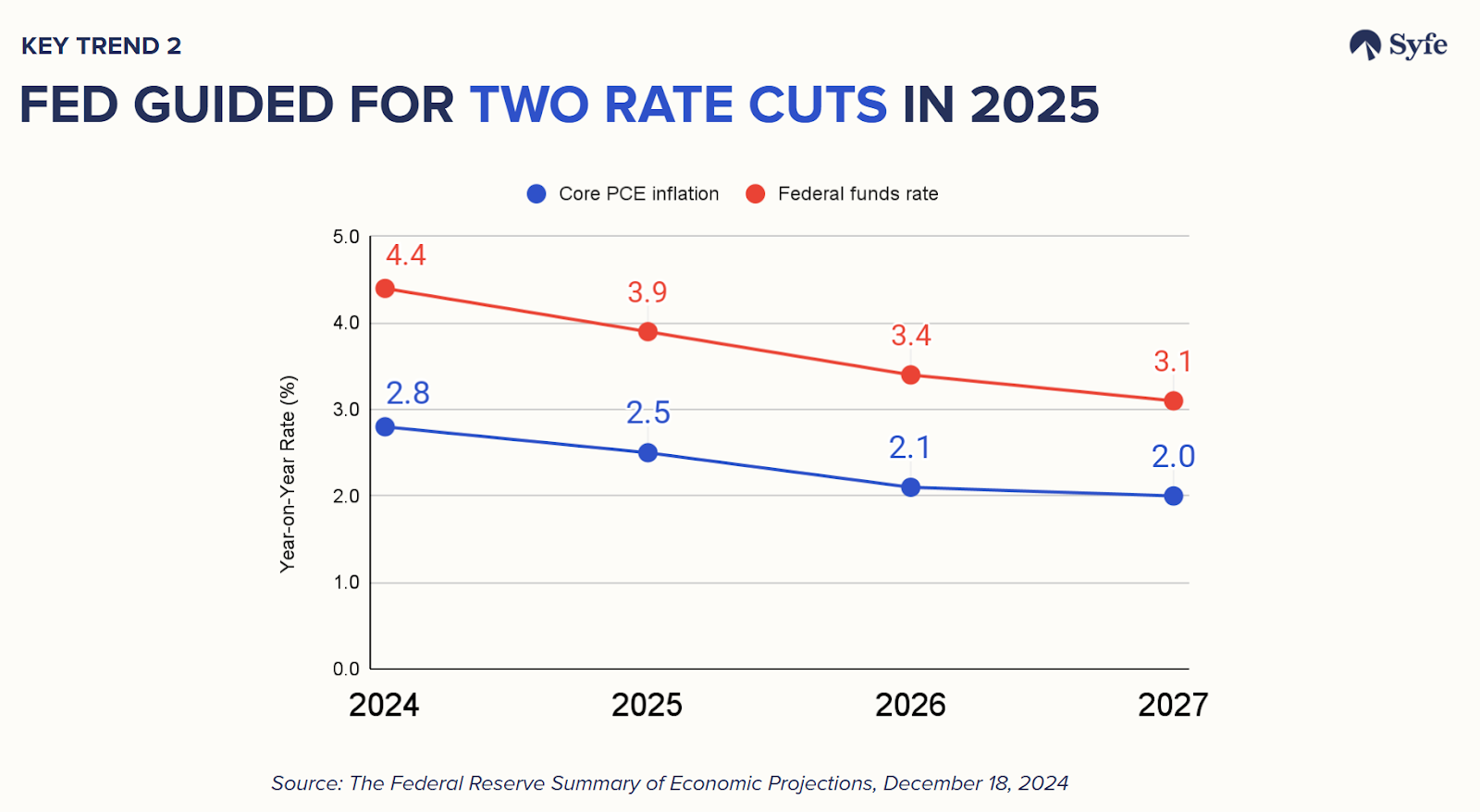

In 2018, when Trump enacted tariffs on Chinese goods, the Fed refrained from reacting directly to the tariffs. Policymakers expressed a willingness to “look through” temporary tariff-induced inflation spikes, viewing them as one-time changes rather than persistent pressures. For 2025, we expect the Fed to adopt a similar stance regarding tariff-led inflation.

It’s important to emphasize that the slowdown in rate cuts does not mean the Fed is pivoting its policy toward hiking rates. Fed Chair Powell compared the current situation to “driving on a foggy night… you slow down“. In the December 2024 FOMC meeting, the Fed’s dot plot indicated two additional 25 bps cuts in 2025. Looking ahead to 2025, we anticipate the Fed is likely to make one more cut around mid-year before pausing to assess economic growth and the impact of policy changes in H2 2025.

IMPLICATIONS: The bar for the Fed to hike rates again is very high. We remain confident in the Fed’s flexibility and ability to respond swiftly to changing conditions, as it demonstrated in Q4 2024. Should there be any economic slowdown in 2025, the Fed is well-positioned to act quickly to support growth.

China – Navigate Both Internal and External Challenges

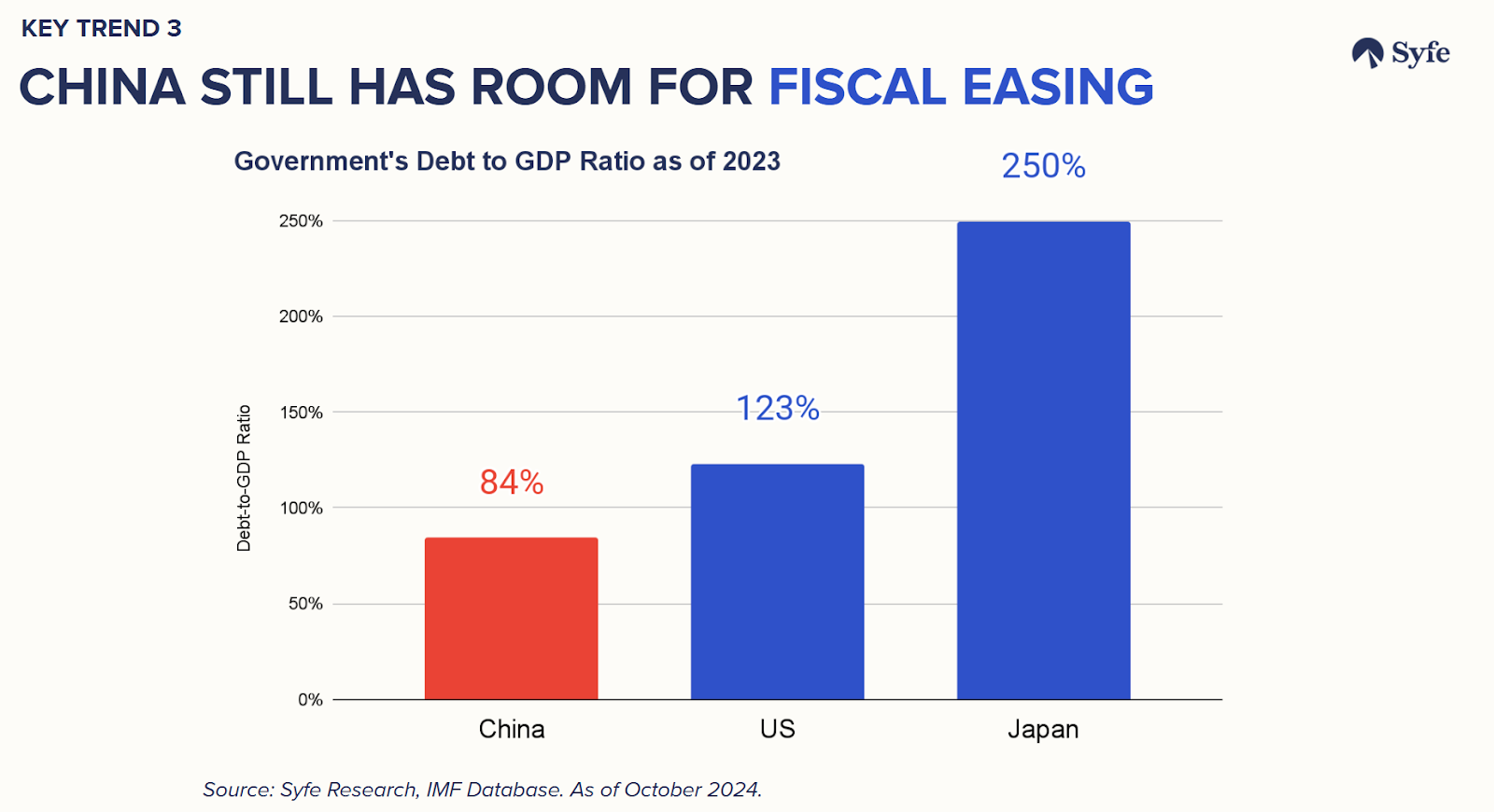

China continues to grapple with structural challenges on multiple fronts: rising local government debt, a slumping property market, an aging population, and weak consumer and business confidence. A notable shift in 2024 was the central government’s apparent recognition that slower growth has reached a point they can no longer tolerate. Adding to the challenges are the looming tariffs threatened by Trump, with broad consensus suggesting these hikes on Chinese goods are likely to proceed.

That said, the current sentiment around China’s economic outlook may be overly pessimistic. On the tariff front, Chinese policymakers appear prepared, with reports indicating a ready playbook to counter Trump’s moves if necessary.

IMPLICATIONS: The Chinese government is expected to rely heavily on fiscal and monetary measures in 2025 to stabilise the economy. While challenges remain, China’s proactive stance and readiness for decisive action could help mitigate the headwinds and lay a foundation for stabilisation.

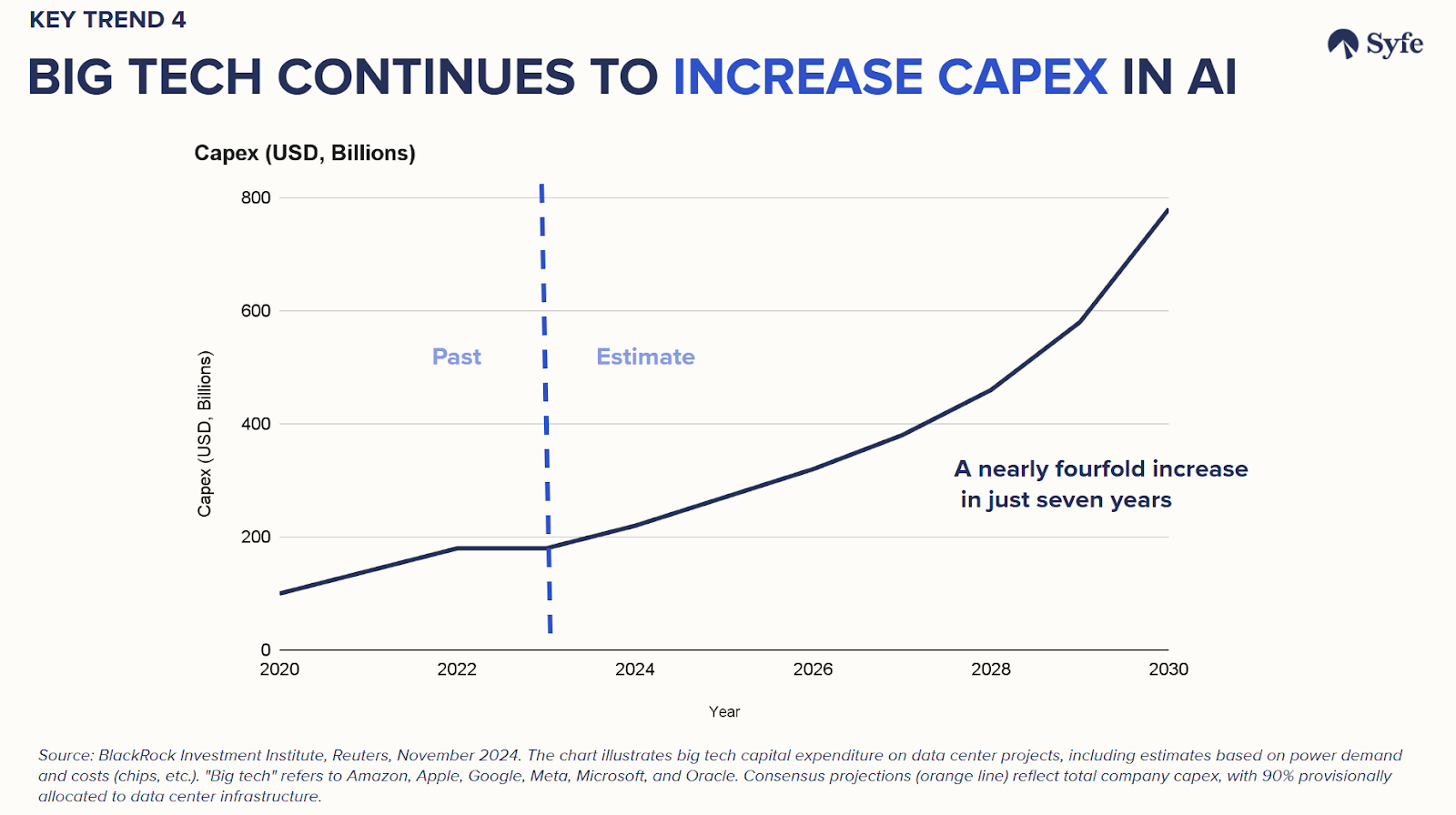

AI Evolution – Capex Goes Strong

According to BlackRock, the evolution of AI can be broken into three key phases:

Buildout: Laying down the essential infrastructure.

Adoption: Accelerating as AI applications become more refined and widely used.

Transformation: Realizing the full potential of AI, with productivity gains and entirely new business models emerging.

Right now, we’re firmly in the Buildout phase, and the scale of investment reflects this. Companies are pouring resources into building data centers, enhancing power systems, and advancing AI technologies. Spending on AI-related data centers alone has hit USD 220 billion in 2024, a 50% jump from 2023. Looking ahead, this figure is projected to soar close to USD 800 billion by 2030, nearly four times the level in 2023.

IMPLICATIONS: AI continues to solidify its position as a transformative megatrend, offering far more than fleeting hype. The ongoing investment in AI infrastructure, adoption, and innovation is poised to provide structural support to global economic growth, even in the face of potential headwinds such as global trade wars and geopolitical uncertainties. This argues why investors should stay invested despite potential volatility stemming from trade frictions.

Top Risks in 2025

Navigating the investment landscape demands a keen awareness of potential risks. Here are three key risks we’re closely monitoring as we head into 2025:

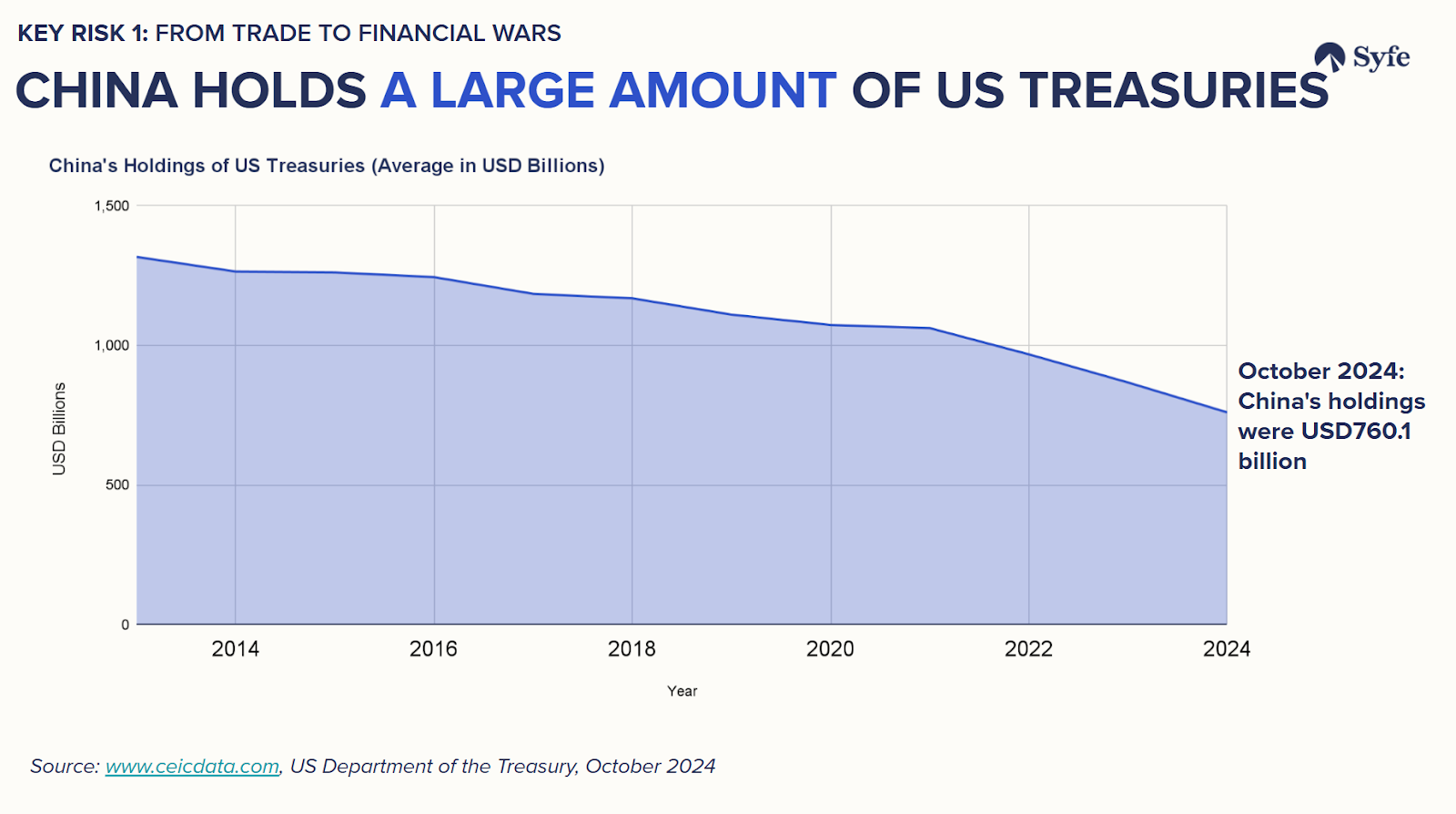

- US-China trade war escalates to financial wars

Low probability, high impact

Key triggers: New tariffs, restrictions on capital flows, or technology trade bans

US-China bilateral relations remain rocky and fluid, with the two nations increasingly at odds over trade, technology, Taiwan, and a host of other issues. Trump’s threats to impose sweeping tariffs have led to a continued souring of relations.

While financial markets have largely anticipated trade conflicts between the two countries, a potential wild card lies in the escalation from a trade war to a currency or financial war. Such a scenario could involve weaponizing financial systems, with severe implications.

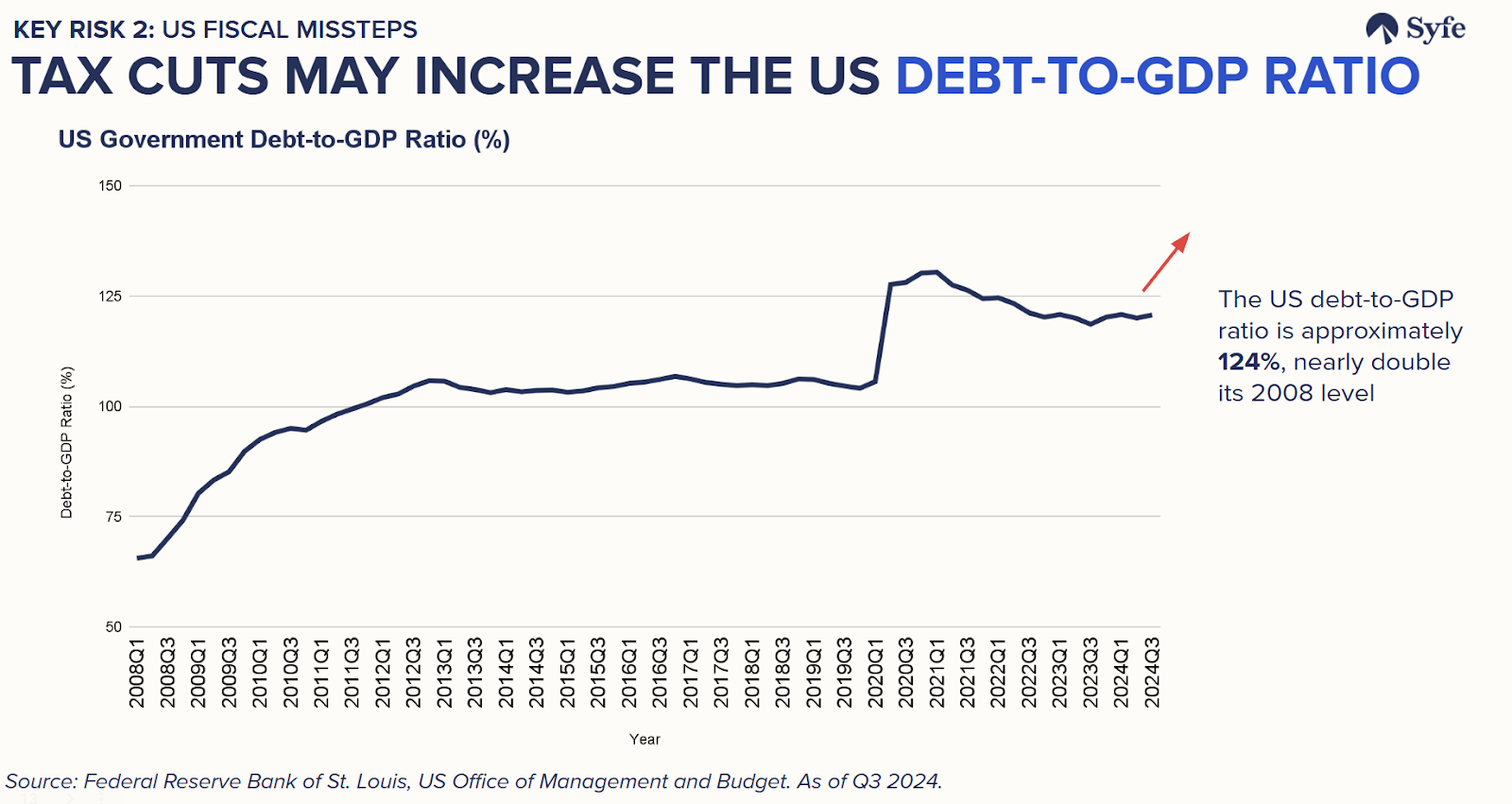

- US government fiscal missteps

Low probability, high impact

Key triggers: Excessive government spending, Inability to control fiscal deficits, Loss of investor confidence in US Treasury securities

The US government’s escalating debt poses a significant long-term economic risk. As this debt balloons, investors may demand higher returns on US bonds, effectively raising borrowing costs for the entire economy. This could stifle economic growth and make it more expensive for businesses and individuals to finance their activities. While not an immediate crisis, this issue demands careful monitoring and responsible fiscal policy to prevent future economic consequences.

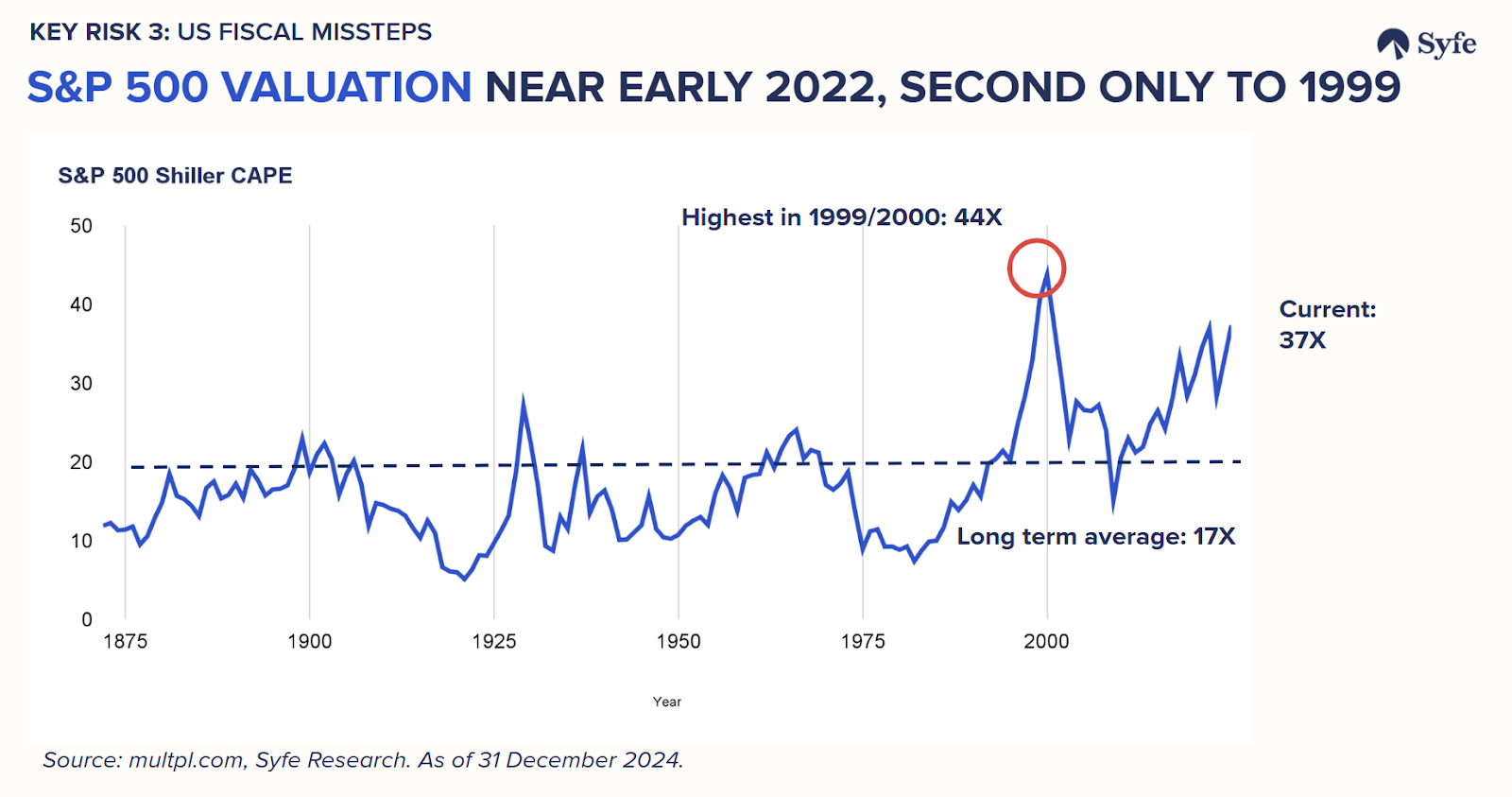

- High valuations and concentration in US equities

High probability, low impact

Key triggers: Big tech earnings below expectations, evidence of slowing AI investments

US stocks are relatively expensive by many standards. For instance, the S&P 500 Shiller CAPE ratio, also known as the Cyclically Adjusted Price-to-Earnings ratio, is calculated by dividing the current price of the S&P 500 by the 10-year moving average of its inflation-adjusted earnings. This metric is at 37X, as expensive as it was at the start of 2022, and second only to the peak in 1999.

Elevated valuations in certain sectors, particularly technology, could result in sharp corrections if earnings growth expectations falter. Crowded trades and over-leveraged positions could amplify sell-offs during periods of stress.

Conclusion

As we look ahead to 2025, market volatility is expected to rise, fueled by policy shifts following President Trump’s re-election. Yet, this shifting landscape offers unique opportunities for investors willing to adapt and stay the course.

With the Fed’s responsive policies and the transformative growth of AI, the foundation for economic expansion remains strong. A diversified approach will be key to navigating uncertainties while capitalising on the opportunities created by evolving market trends.

Dive into our top themes and strategies to position your portfolio for success in 2025. Read more: Top 5 investment themes for 2025

You must be logged in to post a comment.