Despite a soft start of the quarter, global equities and bonds ended the quarter on a strong note. The quarter began with a sell-off in stocks as recession fears weighed on investors. Between 1 July and 5 August, the S&P 500 dropped by -7.5%. However, in the September 2024 FOMC meeting, the Fed shifted its focus towards supporting growth by cutting its key interest rate by 50 basis points (0.50%). This not only erased the losses but also propelled the S&P 500 to new all-time highs. In the final two weeks of the quarter, Chinese equities also surged, driven by optimism around potential policy support from the government.

This quarter highlighted the dynamic nature of markets and reinforced the importance of staying agile in response to changing conditions. It also underscored the need to adjust our portfolios periodically to align with evolving market trends.

In this quarter, our managed portfolios delivered strong performance across the board. Notably, we made significant enhancements to our Core Portfolios to improve long-term returns. We also re-optimised our Income+ and REIT+ portfolios.

Key performance highlights for Syfe Portfolios in Q3 2024:

Syfe Core Portfolios: Outperforming & Upgraded for Better Long-term Growth

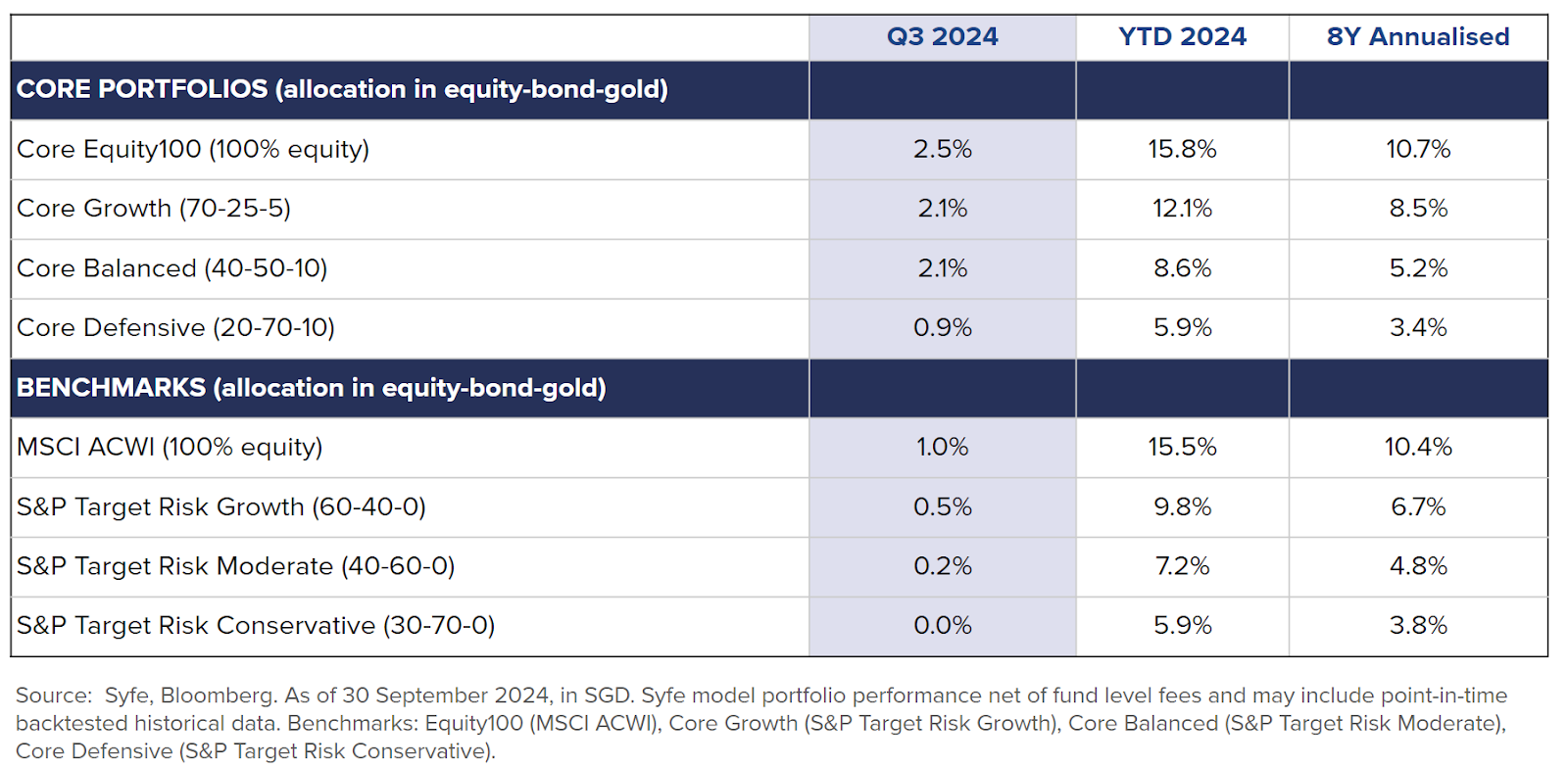

Performance Spotlight: Core Portfolios delivered another strong quarter of performance. Core Equity100 returned +2.5% in Q3, outperforming its benchmark, the MSCI All Country World Index, by an impressive 1.5%. This brings the Portfolio’s YTD return to +15.8%. The Growth, Balanced, and Defensive portfolios posted quarterly returns of +2.1%, +2.1%, and +0.9% respectively, all outperforming their benchmarks, bringing their YTD returns to +12.6%, +8.6%, and +5.9%.

The main driver of outperformance was the allocation to emerging market equities, particularly Chinese stocks. Following a bold 50 bps rate cut by the Fed in mid-September, China’s policymakers introduced a series of monetary and fiscal easing measures. As a result, Chinese equities saw a double-digit jump in the last two weeks of September.

Strategic allocation to gold also provided a boost to Core Portfolios. With increasing global uncertainty, gold acted as a safe haven, helping our Growth, Balanced, and Defensive portfolios stay strong. This demonstrates the value of diversifying investments across different asset classes for long-term success.

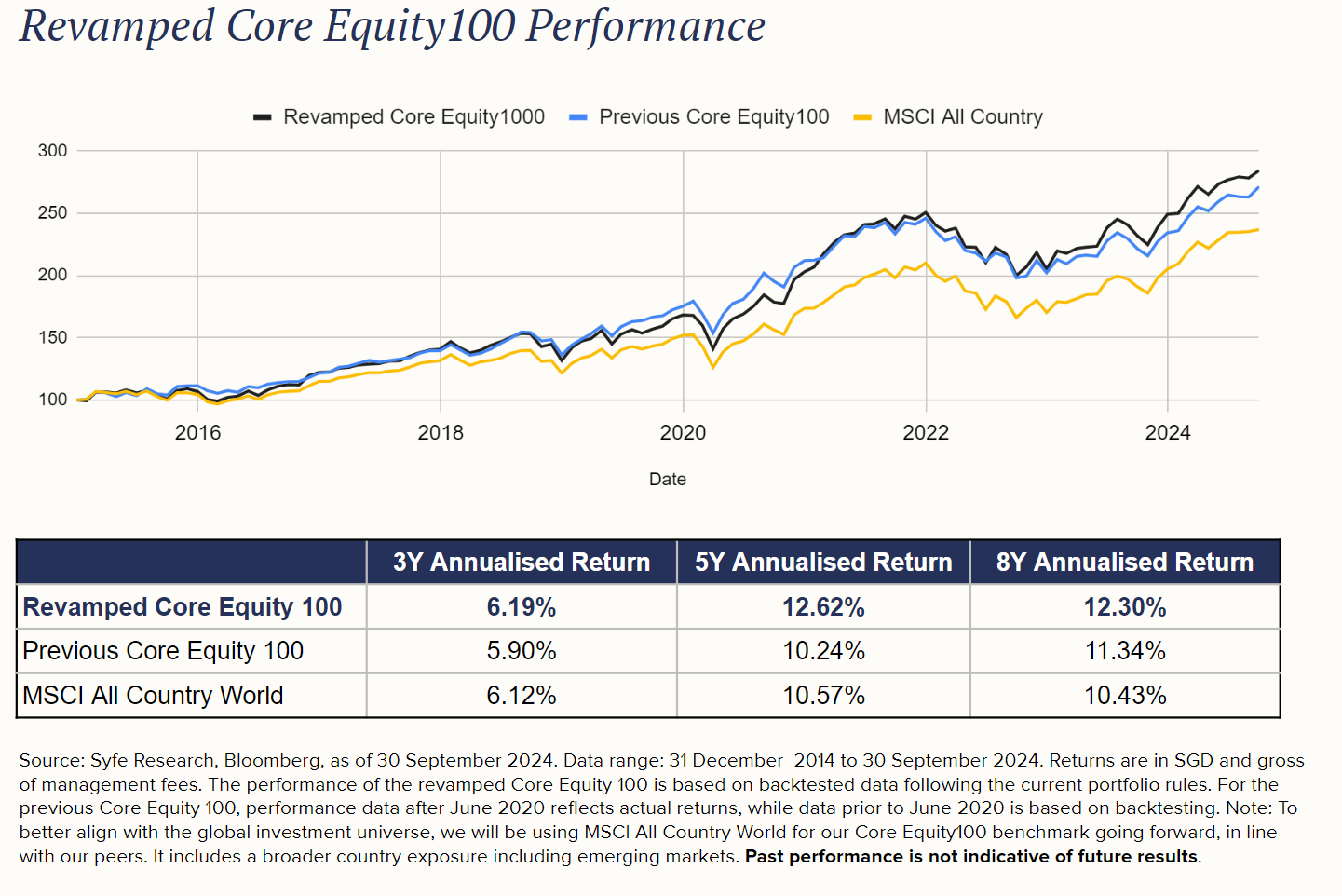

Major Enhancements for Improved Long-Term Performance: We carried out major upgrades to the Core Portfolios from the last week of September to the first week of October. These include enhancing factor strategies to boost long-term performance, optimising bond allocations for higher yields, and improving tax efficiency by shifting to UCITS ETFs. You can find the details of these enhancements and the updated allocations here.

As a result of these upgrades, the revamped Core Equity100 Portfolio is expected to deliver a notable improvement in long-term returns. Below is a comparison of the new Core Equity100 Portfolio versus the previous version and the benchmark.

Looking ahead: Fed rate cutting cycles typically lead to rotations in stock performance, favouring certain characteristics over others. Based on past cycles, value stocks tend to outperform growth stocks, and mid-to-small cap stocks often do well.

In our latest revamp, we’ve enhanced the Core Portfolios to include value and quality factors, as well as small and mid-cap stocks. These upgrades aim to drive superior long-term returns by integrating key strategic factors, improving diversification, and pursuing more sustainable performance. The upgraded Core Portfolios are also better aligned with the current market environment, which is expected to favour these factors.

Syfe REIT+ : A Long-Awaited Turning Point is Here

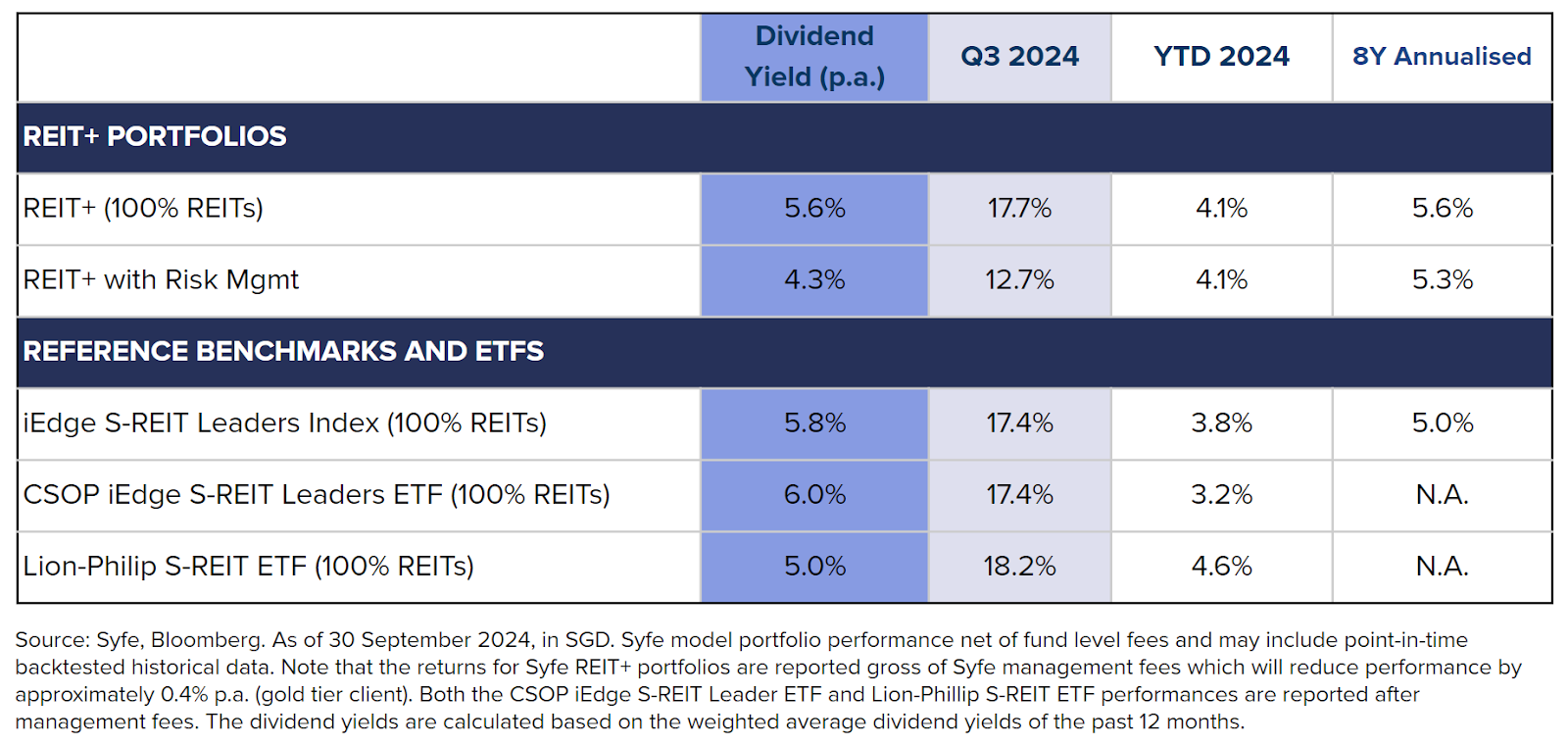

Performance Spotlight: S-REITs made a strong comeback in Q3, driven by the Fed’s decisive rate cut. The REIT+ (100% REITs) Portfolio surged by +17.7% in Q3, bringing its YTD return to +4.1%. It’s impressive to note that REIT+ has consistently outperformed its benchmark, the iEdge S-REIT Leaders Index, both during challenging market conditions in 2022 and 2023, and in favourable markets like Q3 2024. This consistent outperformance has demonstrated the effectiveness of our optimisation process

The REIT+ Portfolio has been re-optimised in September, in line with the semi-annual rebalancing for the iEdge S-REIT Leaders Index. You can view the updated portfolio allocation here

Looking ahead: We believe S-REITs have reached a long-awaited turning point. We remain optimistic about the sector’s outlook as we are at the beginning of a rate-cutting cycle. Lower interest rates can ease the elevated borrowing costs many S-REITs have been facing. While it may take a few quarters for the positive impact to be fully reflected in their financial results, we believe patience will be rewarded.

In addition to lower interest rates, Singapore’s economy has remained resilient, with Q2 GDP growth of 2.9% in 2024. This strong economic backdrop can support positive rental reversions for S-REITs.

There are also signs that institutional investors are returning to the S-REIT sector. In the first half of 2024, S-REITs saw net institutional outflows of S$1.07 billion. Since then, 16% of these outflows have reversed, with net inflows recorded in the second half of 2024, up to mid-Oct.

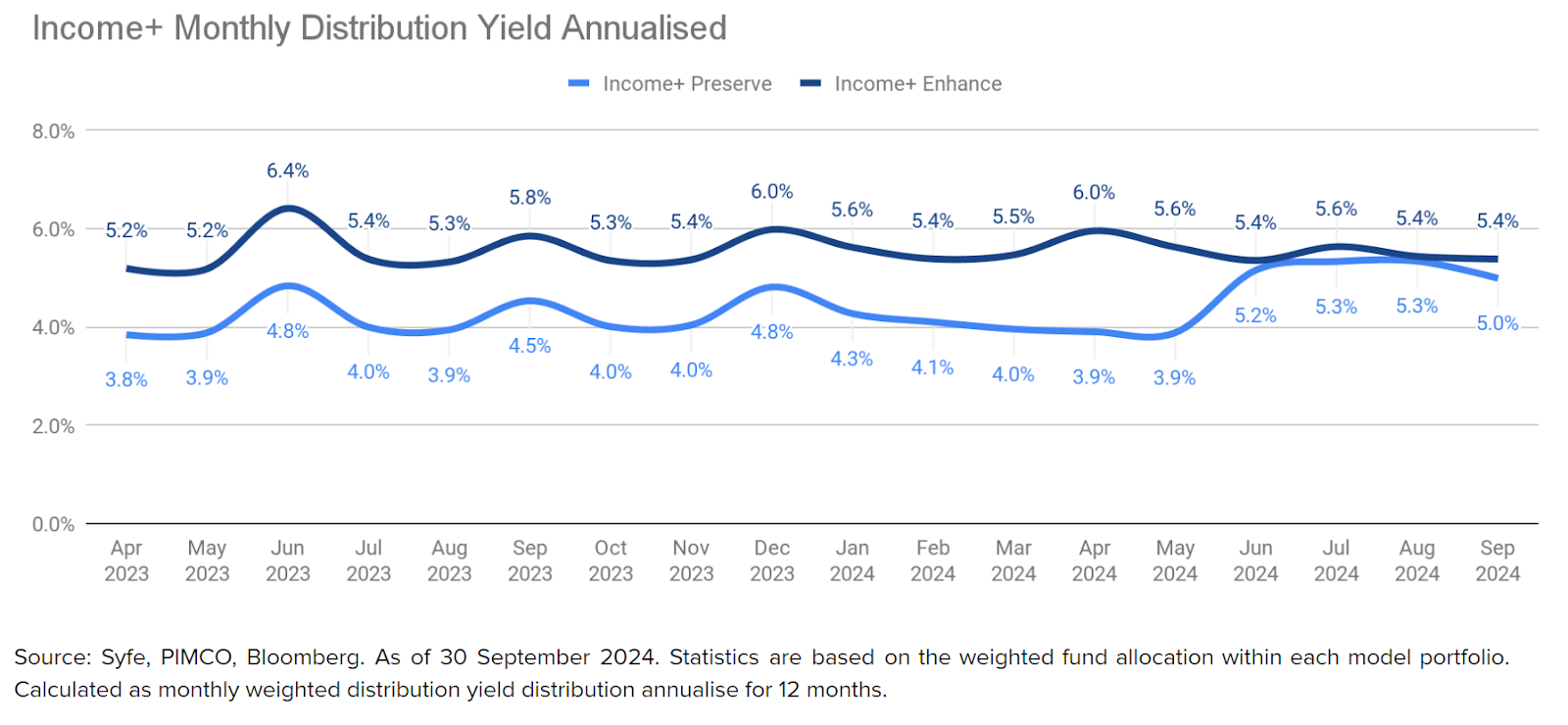

Syfe Income+: Outshined in a Shifting Bond Market

Performance Spotlight: The Fed’s rate cut in the third quarter pushed bond yields lower, with short-term Treasury yields experiencing the most significant declines. This decline in yields helped broad bond markets achieve solid gains.

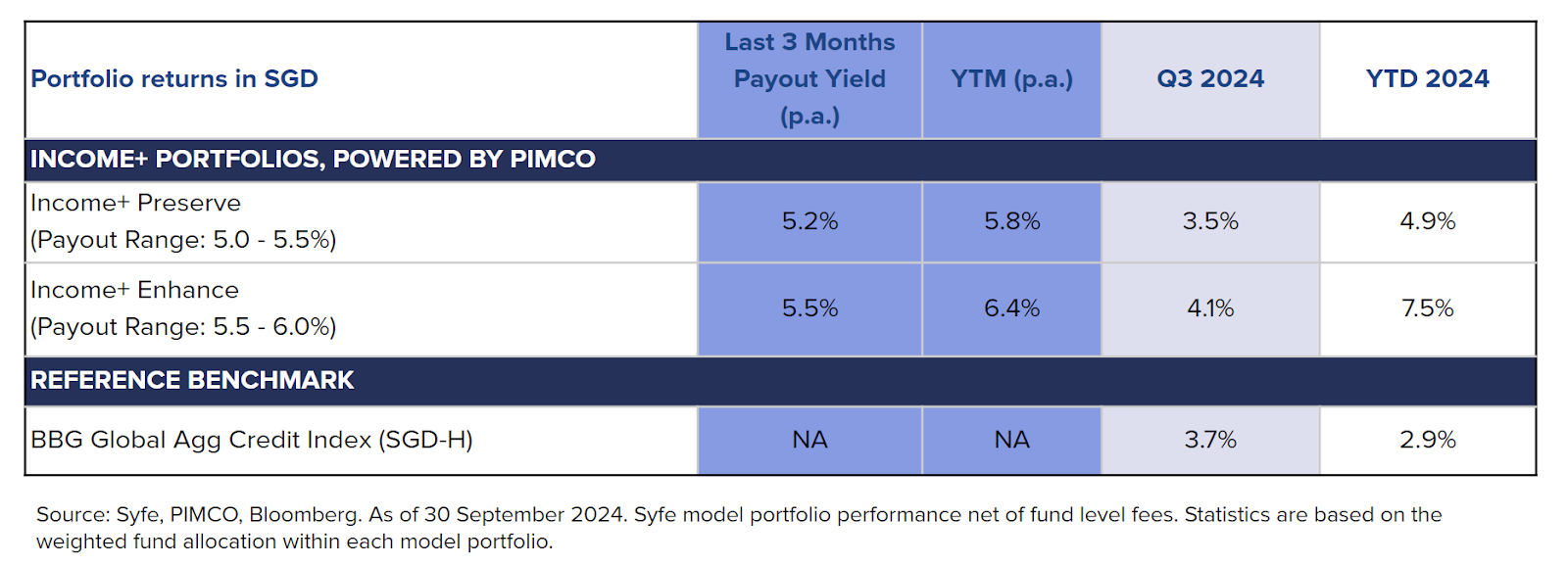

Our Income+ Preserve and Enhance portfolios delivered strong returns of +3.5% and +4.1% respectively, bringing their YTD performance to +4.9% and +7.5%. This YTD performance significantly outperforms the broad bond market, driven largely by PIMCO’ active management of duration, credit, currency, and country exposure.

Monthly Payout: Income+ has delivered on its promise of attractive payout yields. Following a portfolio re-optimisation in July aimed at increasing monthly payouts, the annualised distribution yield for Income+ Preserve rose from 3.9% in Q2 to 5.2% in Q3. As a result of this significant improvement in yield, we’ve raised the target distribution yield from a range of 4.0% to 4.5% to a new target of 5.0% to 5.5%. Income+ Enhance also continues to deliver, with an annualised distribution yield within its target range of 5.5% to 6.0%.

Looking ahead: Global bonds remain attractive even after the recent rally, with yields continuing to offer compelling value. As of 30 September, the yield on global investment-grade credit stands at 4.7%, significantly above the 10-year average yield of 3.4%. Economic indicators are also normalising—Core PCE inflation dropped to 2.7% in August, nearing the Fed’s 2% target.

With inflation easing, the Fed has room to lower interest rates further, which is good news for bond investors. This presents an opportunity for capital appreciation for bond investors, in addition to the attractive yields.

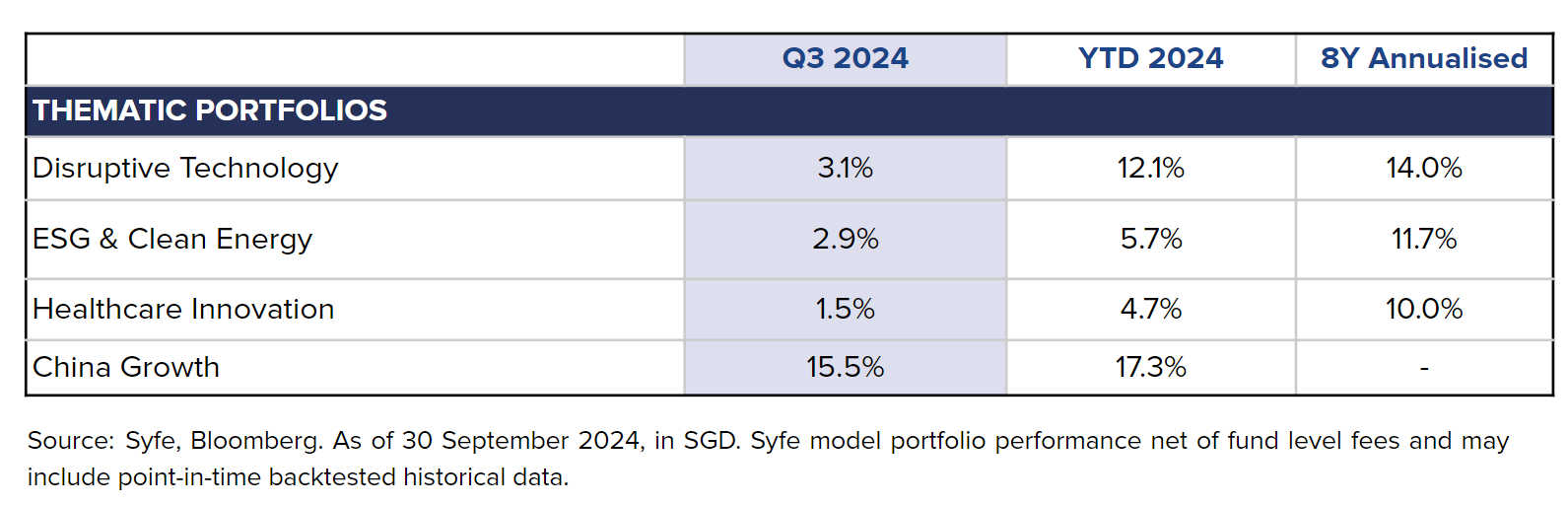

Specialised Portfolios: China Growth Portfolio Surged

Chinese equities captured investor attention in Q3, particularly towards the end of September. Government pledges for increased monetary and fiscal support sparked a dramatic market surge in the last two weeks of the month. Our China Growth portfolio, positioned in A-shares, internet sectors, and those sectors likely to benefit from policy support, performed exceptionally well, achieving a +15.5% return in Q3. This brings China Growth portfolio’s YTD return to +17.3%.

However, October saw some of those gains reversed as sentiment shifted. This raises the question: is China’s equity bull market sustainable? We believe there’s further upside potential, given attractive valuations and the fact that global fund managers remain significantly underweight in Chinese equities. However, investors should be aware that this market is often volatile, characterised by rapid upswings and downswings. Uncertainties remain, including the effectiveness of policy measures and the upcoming US elections. Therefore, investors should carefully consider their position sizes in this market.

The other three themes in our portfolio — Disruptive Technology, ESG & Clean Energy, and Healthcare Innovation — all delivered positive returns, keeping pace with the broader equity market. Disruptive Technology, in particular, continues to be a key area of focus for long-term investors.

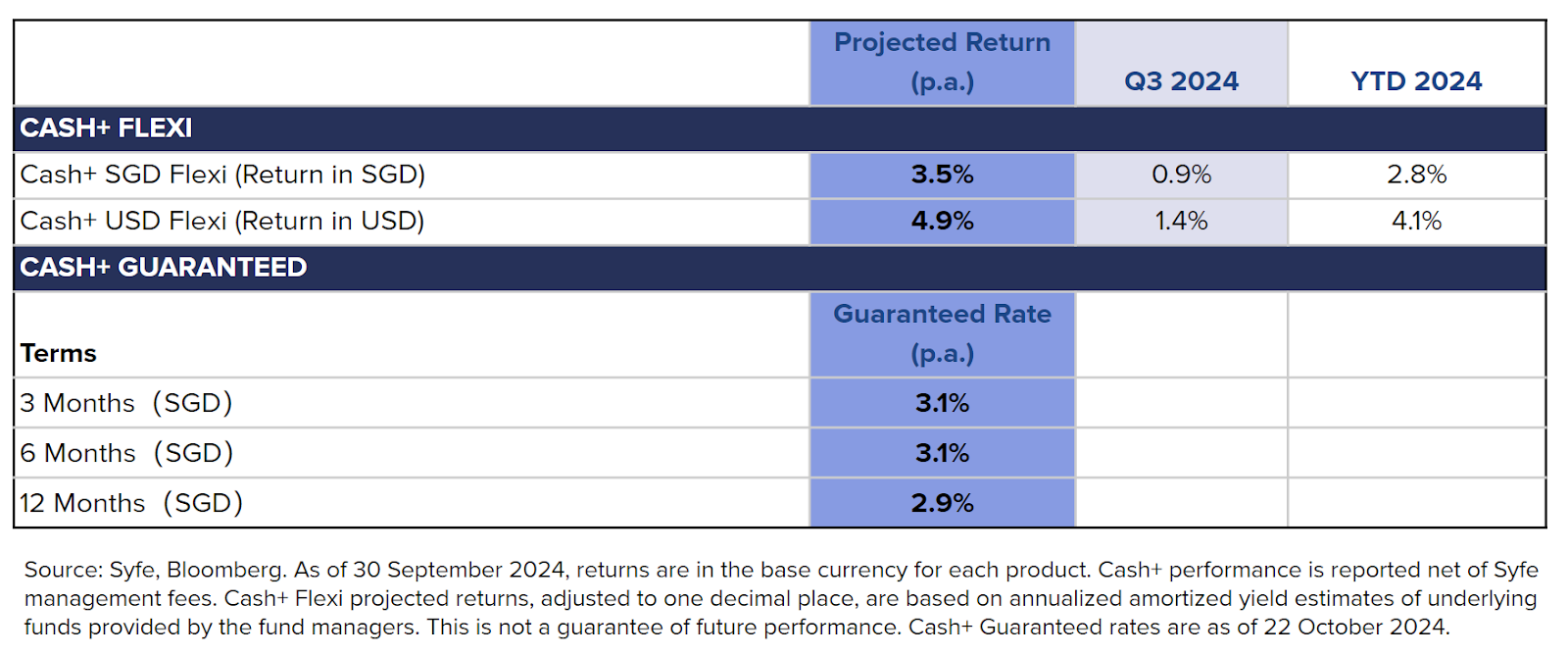

Syfe Cash+ : Put Your Extra Cash to Work

Cash+ Flexi:Our Cash+ Flexi portfolios delivered steady and positive returns in the third quarter of 2024. The Cash+ SGD Flexi portfolio generated +0.9% in Q2, bringing the YTD return to +2.8%. The Cash+ USD Flexi portfolio generated +1.4% in Q2, bringing the YTD return to +4.1%. Both portfolios are on track to meet their projected returns.

As some local banks begin lowering deposit interest rates, Cash+ Flexi offers a compelling alternative for parking emergency funds or short-term cash needs. These portfolios invest in highly liquid, low-risk money market funds, allowing withdrawals within 1 to 2 working days.

Cash+ Guaranteed: In response to the current lower interest rate environment, Cash+ Guaranteed rates have been adjusted for Q3, now ranging from 2.9% p.a. for a 12-month term to 3.1% p.a. for a 6-month term. These rates remain competitive, surpassing those offered by traditional fixed deposit accounts and other cash products like Singapore T-bills, which have also seen their yields fall to 3.1% for 6 months and 2.7% for 12 months.

If you have funds you can set aside for a short period, Cash+ Guaranteed offers a compelling combination of attractive returns and peace of mind.

Time to invest your extra cash: Beyond your emergency savings and short-term needs, now is the perfect time to consider investing for the long term. With the Federal Reserve expected to cut interest rates further in 2024 and beyond, today’s attractive yields on cash may not last. History shows that various asset classes tend to perform well during periods of monetary easing, such as the one we’re entering now. To make the most of this potential opportunity and enhance your returns, consider reallocating some of your cash into investments like bonds, S-REITs, or equities.

Our Thoughts For Q4 2024

With the US election approaching on 5th November, the race between Trump and Harris remains too close to call, as polls show both candidates running neck and neck. One potential outcome, a “Republican Sweep” where Trump wins the presidency and the Republican Party takes control of both the Senate and the House, could bring significant changes. Notably, Trump’s stance on tariffs may lead to global trade disruptions if enacted.

However, when looking beyond the short-term election risks, historical data from the past 75 years suggests that US elections typically have minimal long-term impact on financial markets. Market performance tends to be more closely tied to broader economic trends than to election outcomes.

Read More:

A New Chapter in Interest Rates – What Does This Mean for You?

You must be logged in to post a comment.