As a foreigner (or expat) in Singapore navigating financial planning can feel like a journey full of unknowns.

For myself, living in Singapore has been quite a journey—I moved here from the UK shortly before the pandemic. (Talk about poor market timing!) Not long after, I met my now-wife, who’s from México. We’ve built a life together in this vibrant country and, like many of our friends who are far from home, have no immediate plans to leave.

Even with an uncertain timeline for exactly how long we’ll stay, we’ve found the Supplementary Retirement Scheme (SRS) to be one of the most effective ways to invest for the future whilst reducing and postponing taxes – whether we stay a few more years or decades.

See below for four key scenarios in which you should seriously consider investing in your SRS today!

What is the Supplementary Retirement Scheme (SRS)?

You can check out our full guide here. Essentially, SRS is a voluntary savings programme introduced by the government to encourage individuals to save for retirement while enjoying tax benefits.

What makes SRS particularly appealing for foreigners is the high maximum contribution limit, a limit of up to S$35,700 can be used per year to reduce your tax bill.

How is an Expat’s Tax Calculated in Singapore?

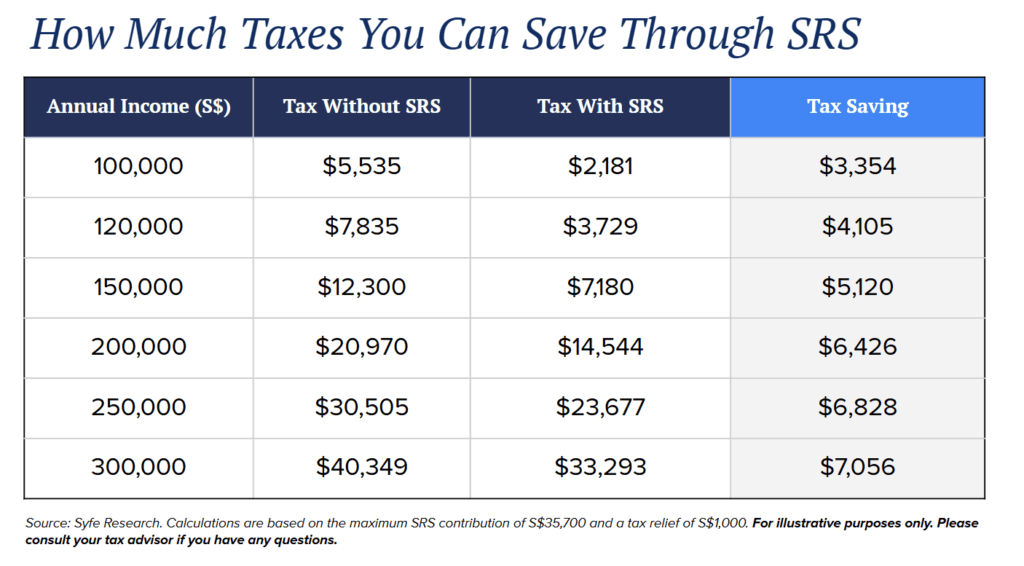

Singapore’s tax system is progressive and highly attractive for expats, with no capital gains tax and competitive income tax rates. Contributions to SRS directly reduce your chargeable income, lowering the tax you pay.

For example, at an income level of S$150,000, contributing the maximum S$35,700 to SRS could reduce your tax bill by over S$5,000. These savings are immediate and tangible, making SRS an easy choice for tax optimisation while working in Singapore.

Withdrawing Your SRS Funds as a Foreigner

Typically, if you withdraw before reaching Singapore’s statutory retirement age (currently 63), a 5% penalty applies, and the withdrawn amount is taxed as income. However, expats have a unique advantage: you can make a one-time, penalty-free withdrawal after holding the SRS account for 10 years, provided the entire balance is withdrawn in one go. In this case, only 50% of the withdrawn sum is taxable, making it a highly tax-efficient option.

The ability to optimise your SRS withdrawals depends on various factors, including your tax residency status, retirement timeline, and projected income needs.

While detailed planning varies for everyone, here are some scenarios where contributing to SRS makes immediate sense. If any (not necessarily all) of these apply to you, it’s worth seriously considering investing now:

- You are investing from the 11.5% tax bracket or higher.

OR - You will withdraw the funds in less than 30 years and are investing from the 7% tax bracket or higher.

OR - You plan to retire as a tax resident in Singapore and are investing from the 2% tax bracket or higher.

OR

- You plan to retire as a tax resident in Singapore and your SRS account will not breach $400,000.

In each of these examples, based on current tax rates, the tax rate saved now will highly likely be greater than the eventual tax rate paid at withdrawal (given the 50% discount), regardless of how big your retirement nest egg grows.

Planning your SRS withdrawal strategy is crucial, as it can significantly impact both your tax liability and long-term financial goals. If you’d like a dedicated article exploring SRS withdrawal strategies and other scenarios in greater detail, email us at [email protected] to share your interest.

How Should You Invest Your SRS Money?

Contributing to SRS is only part of the equation; investing those funds wisely is where the real growth happens since the SRS bank account earns a mere 0.05% in interest. In fact, nearly 20% of all SRS monies are just sitting in cash, slowly getting eroded by inflation!

One standout option for SRS investments is Syfe’s Core Equity100 portfolio, which is designed for long-term growth through equity-focused investments.

Core Equity100 has historically delivered an 8-year annualised return of 11.5%, significantly outperforming the 6–8% average returns of actively managed funds during the same period. Its factor-based strategy tilts towards value, quality, and size while minimising concentration risks, ensuring diversified exposure to global equity markets.

Explore how to make the most of SRS investing with Syfe.

Is SRS Worth It for Foreigners?

Absolutely. The combination of immediate tax relief and additional withdrawal options makes SRS a powerful tool for foreigners working in Singapore.

For me, contributing to SRS and investing in Syfe’s Equity100 portfolio has been a straightforward way to lower taxes and grow wealth. Even with an uncertain timeline in Singapore, the benefits of SRS are clear.

Final Thoughts

Whether you’re in Singapore for a few years or a decade and beyond, the SRS offers a simple yet effective way to optimise your finances. Take advantage of the higher contribution limits for foreigners – it’s a smart strategy for building wealth while reducing your tax burden – one that works no matter where life takes you next.

Disclaimer: This article is for informational purposes only and does not constitute tax advice. Please consult a qualified tax advisor for advice tailored to your specific circumstances and consult https://www.iras.gov.sg/ where necessary.

Read more:

You must be logged in to post a comment.