Diversification has been called the only free lunch in investing. Beyond diversifying across asset classes and sectors, geographic diversification is also important when it comes to managing investment risk and getting better returns. While investing beyond Singapore’s borders has its advantages, fluctuations in exchange rates can affect your portfolio – especially in the short term.

So what should you know about currency impact, and how does it impact your portfolio?

Why Exchange Rates Fluctuate

Currencies are always fluctuating in price against one another as they are traded on the foreign exchange (forex) market. A currency’s forex value depends on a confluence of factors, including:

Central bank interest rates. Higher interest rates set by a country’s central bank tend to increase that currency’s value. Higher rates attract more foreign capital as investors will get a better return by holding assets in the country’s currency. The currency thus tends to increase in value due to the rise in demand.

Economic growth. A country with strong economic growth and financial stability tends to attract more foreign capital. This increased demand for the country’s assets can lead to a stronger currency. On the other hand, slower growth or rising uncertainties—such as geopolitical tensions or global trade disruptions—can put downward pressure on the country’s currency.

Inflation. Countries with high inflation rates tend to have lower currency values. As the prices of goods and services increase at a faster rate relative to other countries, demand for the country’s exports falls, bringing about less demand for the country’s currency as well.

Political stability. Political shifts can trigger swift currency movements. The UK’s Brexit vote in 2016 is a classic example – the pound fell 20% before making a partial recovery.

Currency Movements and Your Portfolio

If you’re investing in ETFs, stocks, funds, bonds, or fixed deposits that are in USD (or any other foreign currency) while your base currency is SGD, you’ll be exposed to currency impact. In simple terms, your returns may go up or down depending on exchange rate movements.

You’ll notice that your total profit or loss comprises two components:

Portfolio impact – The change in value based on the performance of your investment assets.

Currency impact – The change in value resulting from movements in exchange rates.

Let’s say your investment is in USD. If the USD strengthens against the SGD (i.e., the SGD weakens), your investment will deliver a higher return when converted back to Singapore dollars.

Conversely, if the USD weakens against the SGD, your US-denominated investments will convert into fewer Singapore dollars, reducing your overall return.

Example: How Currency Fluctuations Affect Your Returns

Let’s say you invest USD 10,000 in a US ETF.

- At the time of your investment, the exchange rate is 1 USD = 1.35 SGD.

- So, your investment is worth SGD 13,500.

A year later, your ETF has not changed in value — it’s still worth USD 10,000. That means the portfolio impact is flat.

Scenario A: USD strengthens against SGD

- New exchange rate: 1 USD = 1.40 SGD

- Your investment is now worth SGD 14,000

- Gain from currency impact: SGD 500

Scenario B: USD weakens against SGD

- New exchange rate: 1 USD = 1.30 SGD

- Your investment is now worth SGD 13,000

- Loss from currency impact: SGD 500

This shows that even if the investment itself doesn’t move, currency fluctuations can affect your returns in SGD.

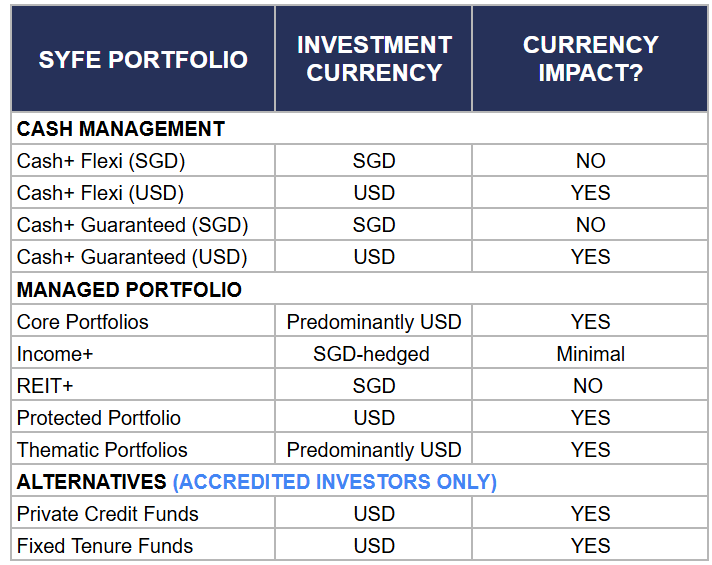

Understanding the Currency Impact of Syfe Portfolios

As Syfe provides access to global investments, some portfolios hold assets denominated in USD. If you fund your account in SGD, forex fluctuations may impact your returns.

Source: Syfe Research, 6 May 2025

- For portfolios like REIT+, Cash+ Flexi SGD and Cash+ Guaranteed SGD, your funds are invested in SGD-denominated assets, so there is no currency impact.

- Income+ portfolios invest in fixed income instruments globally. However, the portfolios are SGD-hedged, which means any currency movements are largely offset. As a result, any currency impact on your returns is kept minimal.

- Core, Thematic, Protected, Custom and Cash+ Flexi USD portfolios are invested in USD-denominated assets, so your returns may be affected by USD/SGD exchange rate movements.

- Cash+ Guaranteed USD guarantees both your capital and returns in USD. Just keep in mind that if you fund your investment in SGD, there may still be some currency impact due to exchange rate fluctuations.

The Mechanics of Investing Internationally

For USD-denominated portfolios (e.g. Core Portfolios, Thematic Portfolios, Protected Portfolio, Custom Portfolios, Cash+ Flexi USD, Cash+ Guaranteed USD), investors have the option of funding their account in SGD or USD. For the latter, there is a minimum investment of USD 10,000 per transaction.

Many Singaporean investors prefer to use SGD to fund their accounts since they don’t hold USD. If you choose to do so, the first thing we do is convert your money into USD. Your portfolio assets are then purchased with the USD we’ve converted. When you wish to withdraw your funds, we receive USD when we help you sell your investments. We will then convert these USD back into SGD before depositing them into your bank account.

Our broker charges Syfe customers a very low currency conversion fee between 0.09% to 0.12% to place trades from their SGD-denominated accounts. Retail investors generally pay much more (between 0.5% to 0.7%) in currency conversion fees.

Should You Invest in USD-Denominated Assets

As a Singapore-based investor, you may be wondering whether it makes sense to invest in USD-denominated assets. Here are a few key points to consider.

- Broader Investment Opportunities

Many top global companies and high-quality bonds are listed in the US. Investing in USD-denominated assets gives you access to a wider range of sectors and markets that may not be available in Singapore.

- Potential for Higher Returns

USD assets, especially US equities and private credits, have historically delivered strong long-term returns. Exposure to these asset classes can enhance your portfolio’s growth potential.

- Natural Currency Diversification

Holding assets in USD helps diversify your currency exposure. This can be useful if the USD strengthens, as your USD holdings may gain in SGD terms. On the other hand, a weaker USD relative to SGD could reduce the value of your investment when converted back. For long-term investors, short-term currency fluctuations often balance out over time. The key is to stay invested and avoid trying to time the forex market.

Bottom Line – Are You Investing for the Short Term or Long Term?

It’s important to be aware of the potential currency impact in your portfolio and consider how much exposure you have. Ask yourself: Why am I investing in USD-denominated assets? Is it for short-term gains or long-term growth?

While exchange rate movements can affect your returns in the short term, strong portfolio performance over the long run typically outweighs currency impact. A globally diversified portfolio remains one of the best ways to manage risk and enhance potential returns.

You must be logged in to post a comment.