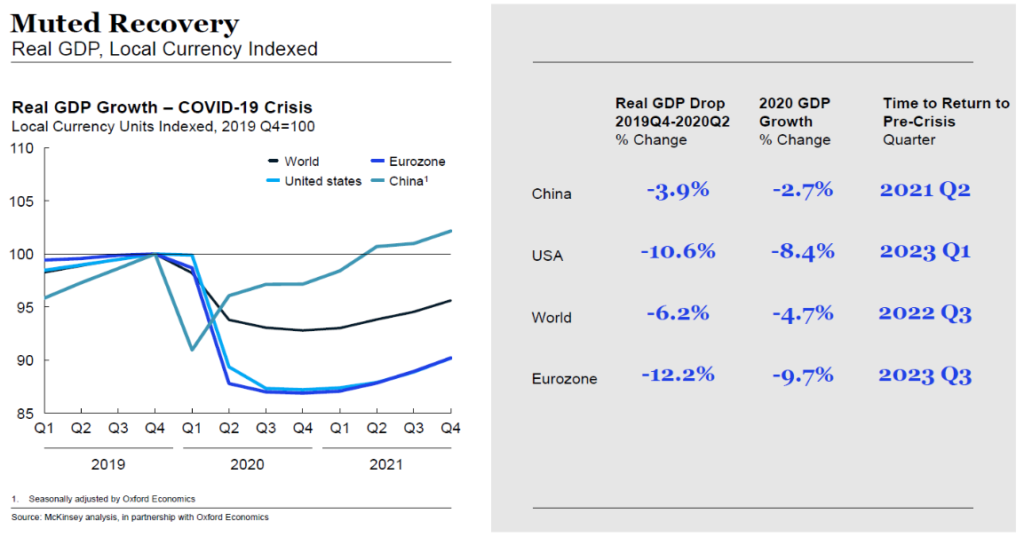

The coronavirus pandemic has sent the global economy into a tailspin. Millions of people have lost their jobs, financial markets have been hit hard, and supply chains have faced major disruptions as factories worldwide shut down.

In the US, the world’s largest economy, the record-long bull run is over after almost 11 years. In its place, a recession is well underway as the US economy shrank at a 4.8% annualised pace in the first quarter, its biggest slump since 2008.

Economists are anticipating a U-shaped recovery, a change from the rapid V-shaped recovery that was initially expected. Many are predicting a significant Gross Domestic Product (GDP) decline for at least the next two quarters of 2020, and possibly extending into 2021 and beyond if the world recovery proves muted.

Paradoxically, despite dismal economic data and first quarter corporate earnings reports, the stock market has rallied over the past weeks as investors become increasingly optimistic about a potential COVID-19 treatment and the reopening of the economy.

But bear in mind that sentiment can turn on a dime. If the reopening of the economy fails to materialise, we may very well see stocks pulling back again.

VIX levels remain elevated

One thing is clear: It will likely take months for investors to get a clearer sense of the full economic impact of the pandemic. Amid this uncertainty, the Chicago Board Options Exchange’s Volatility Index (or the ‘VIX’ as it is better known), remains high at a level of 36.52 at this time of writing, well above its historic average of 18 to 20.

Often referred to as Wall Street’s fear gauge, the VIX is designed to reflect investors’ future view of US stock market volatility based on the option prices of the S&P 500 index – in other words, how much they think the index will fluctuate in the next 30 days. When the VIX level surges, it means that traders in the S&P 500 options market expect market volatility to increase.

Data source: Bloomberg

As shown in the chart above, the VIX typically trades inversely with stock prices. Fuelled by the pandemic and global oil price rout, the VIX (represented by the blue line) soared to record highs through March while the S&P 500 (yellow line) recorded historic plunges.

Volatility is here to stay

While VIX levels may have moderated since March, we are not out of the woods yet from a market volatility standpoint. The VIX is still comparatively high. It is more than double the level it was at prior to the spread of the coronavirus; the VIX closed at 14 on February 19, as the S&P 500 hit its all-time high.

If the VIX is a gauge of market volatility, then the VIX futures market is a prediction for where the VIX will be in the future. Despite the rally we saw in April and May, VIX index futures have been trading higher over the past month, a clear sign that investors expect markets to remain volatile through the year.

Such longer-term volatility would be more consistent with past economic crises when markets faced multiple sell-offs over a prolonged number of months. Potential aggravators include a resurgence in coronavirus infections in China and South Korea, and fresh US-China trade war uncertainty. Meanwhile, the upcoming US presidential election also stands to push volatility higher. In short, we may be in a new volatility regime for the foreseeable future.

What does the sustained high volatility mean for your portfolio?

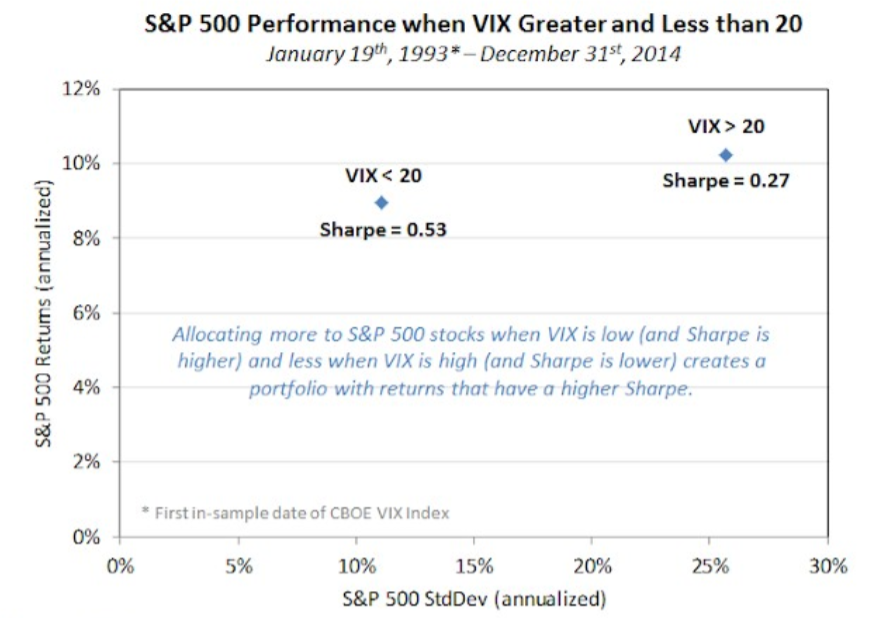

Statistically, high market volatility tends to be associated with lower or negative returns. Historically, when the VIX has exceeded 20, the Sharpe ratio is around 0.27. The Sharpe ratio is a metric investors use to measure the risk-adjusted returns of an investment. The higher the Sharpe ratio, the better the risk-adjusted return.

When the VIX dips below 20, the Sharpe ratio increases to around 0.53. Simply put, we can see that low market volatility usually results in higher risk-adjusted returns.

Source:

Econompic Data

The compounding effect of losses

It is also important to note that higher portfolio volatility lowers potential portfolio returns in the long run due to compounding. This is because the negative effect of volatility on portfolio performance gets compounded over time. When a portfolio loses value, it means that positive returns are earned on less money when the markets recover.

Moreover, the returns needed to recoup the initial losses grow substantially. A 33% loss requires a 50% portfolio gain just to break even. Even if stocks return to their pre-crisis performance, regaining those losses could take several years.

What can investors do?

Amid the continued uncertainty in the markets right now, investors must be prepared for volatility to remain at elevated levels for the foreseeable future. One way to limit the impact of higher volatility on portfolio returns is to adopt a risk management strategy.

For instance, Syfe’s ARITM algorithm automatically shifts portfolio asset allocation towards lower risk bonds and commodities in response to a sustained increase in market volatility. Our objective is to reduce total portfolio risk and ensure that it remains within an investor’s chosen downside risk level. With this strategy, we help investors avoid big losses in down markets while delivering better risk-adjusted returns for them over time, with fewer significant drawdowns along the way. Case in point: We have been consistently outperforming the broader market and our benchmarks throughout the current downturn.

The right risk management strategy can shield investors from significant losses, preserve the strength of their portfolios, and position them to capture the upside as the market makes its eventual recovery. Indeed, when volatility recedes, Syfe’s ARI algorithm will again increase the proportion of equities across portfolios so investors can capture the market upside.

This article first appeared on Finance.sg as a guest article by Richard Yeh, Head of Portfolio Construction and Risk Management at Syfe.

You must be logged in to post a comment.