Thought Of The Week

Fed Minutes, OPEC+ Stalemate, China’s Clampdown

After Federal Reserve surprised markets with a hawkish pivot last month, investors were anxiously scrutinizing the meeting minutes this week for any possible clues regarding the timing of the tapering of asset purchases. While monetary policy signals were clear – target range for benchmark policy rate unchanged at 0-0.25%, it remains vague in communicating a timeline for scaling back asset purchases as “the committee’s standard of substantial further progress was generally seen as not having yet been met.” The benchmark 10-year Treasury yield fell as low as 1.25%, its lowest point since February. Oil prices fell for a third day on Thursday with Saudi Arabia and UAE still at impasse, while Russia steps in to mediate and hoping to rescue the OPEC+ deal. However, oil market is looking beyond the oil supply deficit in August and expecting the OPEC+ agreement to fall apart well before April 2022 when the agreement expires as other member countries will ask for further concessions to secure more market share.

Meanwhile, tighter regulations from Beijing to rein in the tech giants and restrictions on Chinese listings in the U.S continue to weigh on Chinese stocks. Hang Seng Tech index has fallen more than 30% since its February high as concerns continue to linger on how China will implement a crackdown. From the latest scrutiny on Didi’s IPO, it is evident that the Chinese Communist Party wants to exert stronger control over offshore listings and the data held by these technology firms.

Developed and Emerging Country Divide

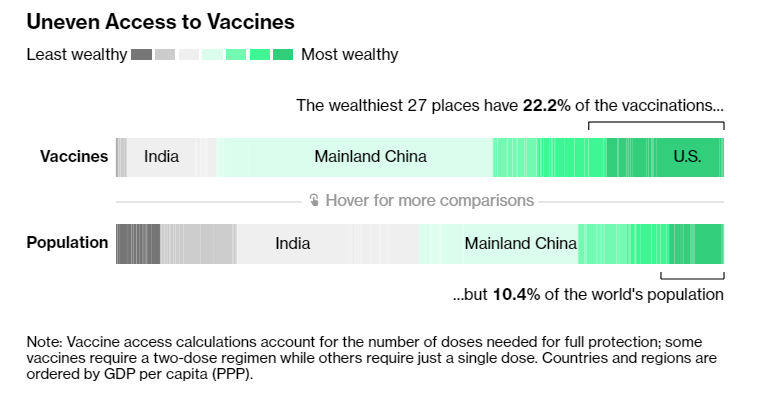

Just as Covid-19 has caused division between the Wall Street and Main Street, distinguishing companies that are winners or losers, the unequal access to vaccines and varying degrees of efficiency is now widening the divide between developed and emerging countries. Although more than 3.33 billion doses have been administered till date (enough to fully vaccinate 21.7% of the global population), less-wealthy countries are finding themselves getting the short end of the stick as they struggle to get access while their richer counterparts have three times the coronavirus vaccine stocks, they need for their own populations.

Although Latin America accounts for 8% of the world’s population, it has suffered nearly a third of global deaths from the pandemic and its worst recession in 120 years. Government debt in the region has risen from 68.9% to 79.3% of GDP between 2019 and 2020, making Latin America and the Caribbean the most indebted territories in the developing world.

Chart Of The Week

Important Information and Disclosure

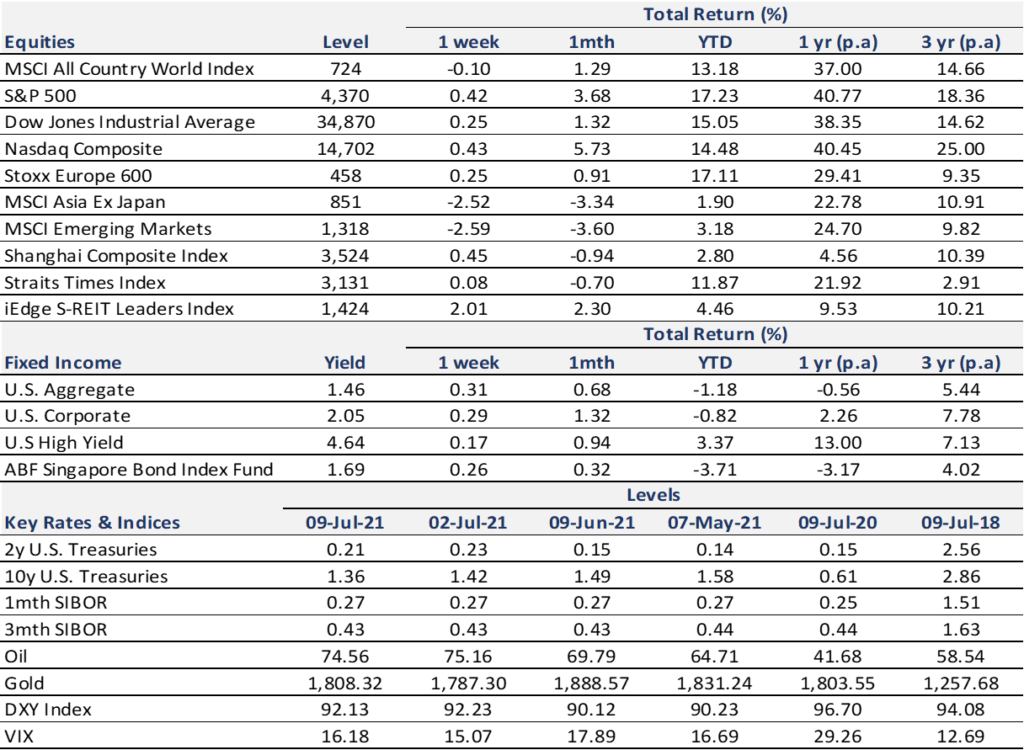

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.