Thought Of The Week

U.S Consumer Price Index (CPI), Retail Sales Data

The August U.S Consumer Price Index (CPI) showed a surprising cooling of price pressures and inflation was lower than expected. CPI rose 0.3% from July which was slightly below economists’ forecast of 0.4%, indicating that the pace may be abating. Some of the categories that saw a spike due to the economy restart (used car prices and airfares) have started to slow. Economists have long argued that consumer prices reflect temporary surges in demand and companies are simply counteracting with price increases. The inflation data confirmed that these demand surges do not last although it is still difficult to anticipate month-on-month swings given the unique nature of the restart dynamics. Ultimately, the volatility in prices should subside as supply-demand mismatches ease.

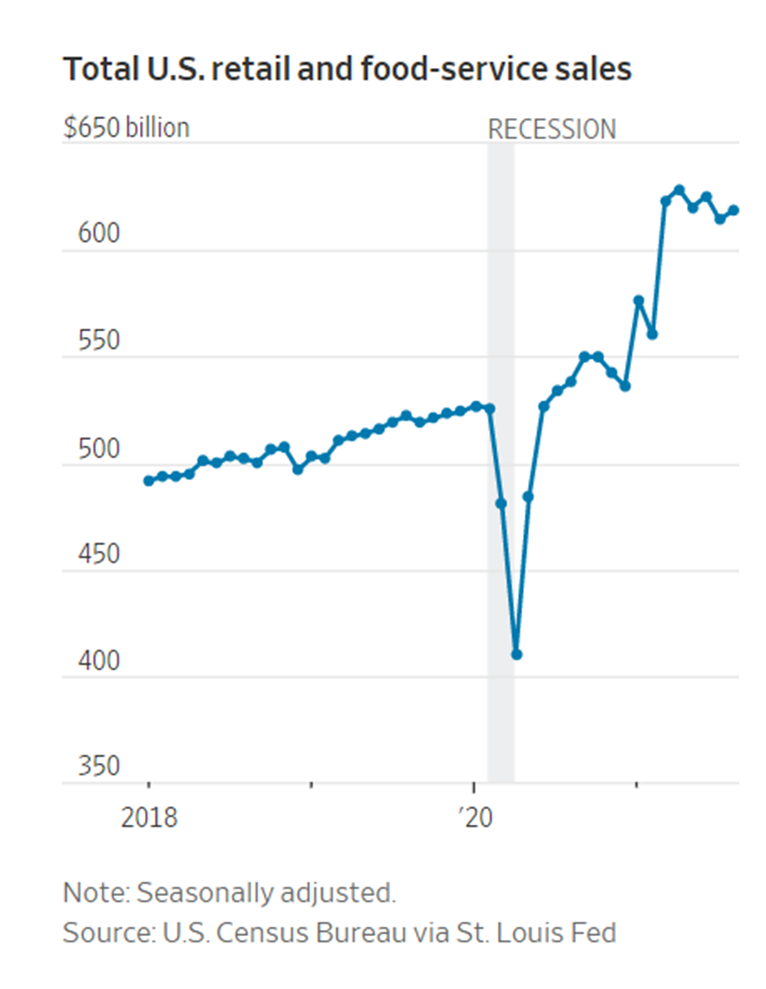

Despite the Delta surge and headlines about inflation, U.S consumers remain well and alive as they increase spending in retail and food service sales with schools and offices reopening. While production shortages and shipping bottlenecks may limit economic growth in the third quarter, economists believe that retail sales will continue to drive consumer spending as more Americans become vaccinated and as product shortages ease. Major U.S stock indices closed the week lower with concerns such as slowdown in economic growth, supply-chain issues and rising pandemic-related deaths added to the volatility.

China’s Next Target: Casinos

Shares of casino operators in Macau plunged on Wednesday after China amended its gambling laws ahead of the expiration of licenses in 2022. Plans to introduce representatives for “direct supervising” on casino operators directly sent shockwaves through related markets and raised fears of tighter control of the industry, similar to the crackdown on the internet and education. Wynn Macau fell 29% while Sands China lost 33% on the news. If Beijing is focusing on eradicating social ills to promote its “common prosperity” mantra, gambling could also be a potential target.

Other notable aspects in the consultation report include social responsibility (which may force future operators to devote more resources to the community), getting government approval before distributing profits to shareholders, and cutting the number of licenses or reducing their lengths. Markets have seen the abrupt regulatory clampdowns on various industries repeated continuously this summer and foreign investors have grown more sceptical about putting money into some parts of China’s economy. Bank of America on Tuesday cut its forecast for China’s gross domestic product growth to 8% and 5.3% in 2021 and 2022, down from 8.3% and 6.2% previously, citing reasons including tightened credit conditions and the risk that Beijing could mishandle the problems at Evergrande.

Chart Of The Week

Important Information and Disclosure

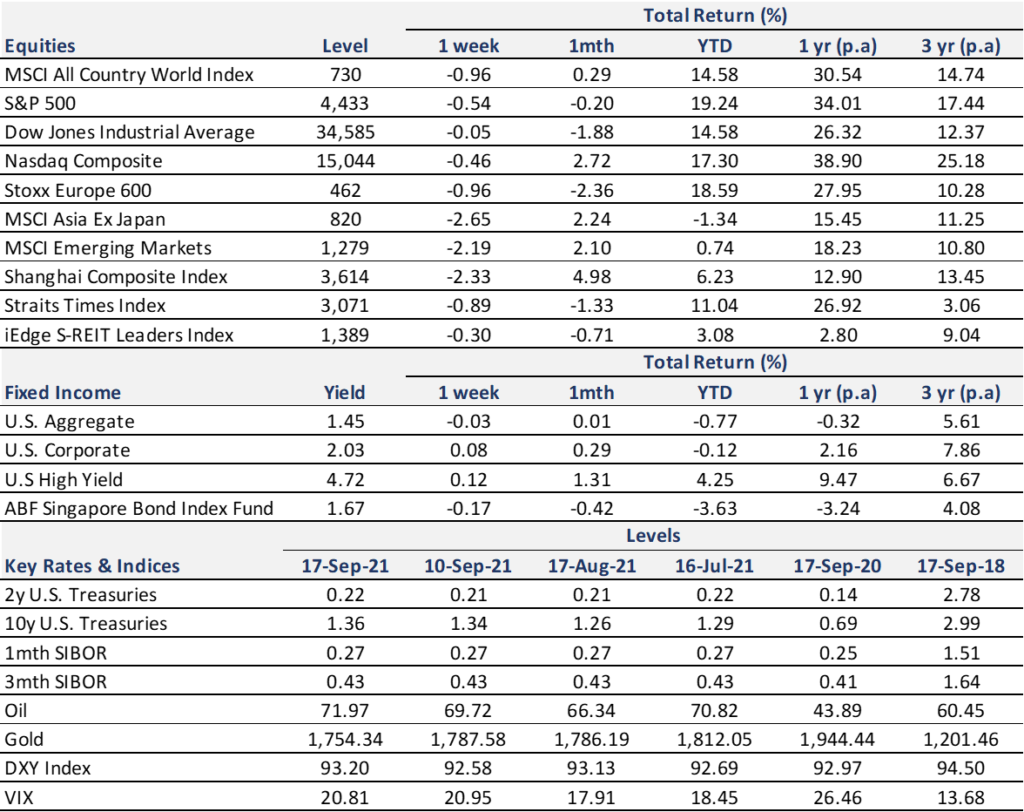

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.