Thought Of The Week

When the Lights Come on At the End of the Night

The FOMC minutes released on Wednesday caused many investors to take flight as it was more hawkish than expected. The actual monetary policy meeting happened in mid-December, but minutes were released at 2pm (EST) three weeks after the day of the policy decision. Firstly, the Fed doubled the pace of taper, allowing it to end asset purchases earlier, March rather than June. Secondly, the dot plot in the December FOMC meeting featured three median hikes (from just a half a hike in the September FOMC projections), signalling a shift in the Fed’s views on risks around inflation. Lastly, the FOMC revised its statement to drop its previous intention to maintain an accommodative policy stance to keep inflation above 2 percent for some time. 10-year Treasury yields rose to as high as 1.71%, a level last seen in April while the S&P 500 extended declines following the release. This means that we could have lift-off (the first rate hike) as early as March 2022.

Same Same but Different

In Chair Powell’s press conference post FOMC, he said “ the inflation that we got was not at all the inflation we were looking for” in response to a question whether the Fed might let inflation run hotter than preferred for a while in order to reach maximum employment. He is making a distinction between demand pull inflation and cost push inflation; the former seems inevitable given pent-up demand and economic activity in 2021 as the country re-opened, coupled with quantitative easing along with unprecedented fiscal spending while the latter is now unavoidable with sustained supply chain disruptions. The Fed was hoping for the first sort of inflation, where 2% was seen as a signal that meant that things were in order.

The US added 199,000 jobs in December, a weaker showing than the consensus estimate of 425,000. Data is released every first Friday of the subsequent month and collected up until the middle of the previous month. This means that the new payroll print released on Friday was collected before the Omnicron variant caused the sharp increase in cases later in December.

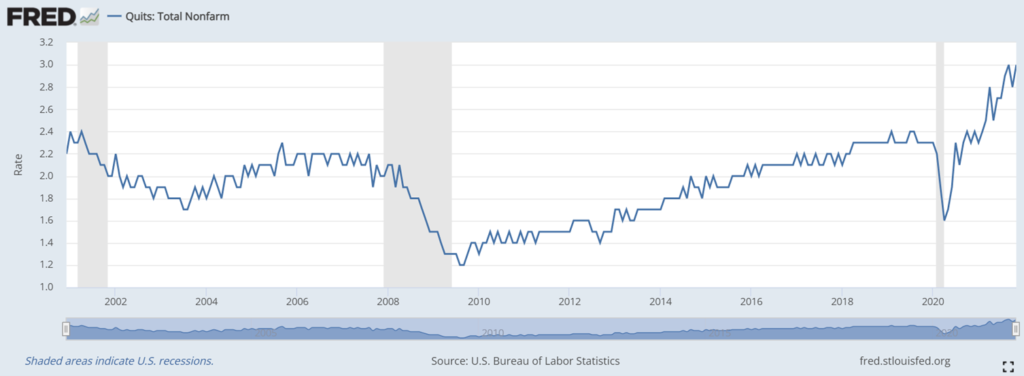

Now, the Fed has a choice to make – take the disappointing December jobs print in stride, putting it in context along with the JOLTS (Jobs Opening and Labor Turnover Survey) data showing a record 4.5 million American quit their jobs in November and keep on the path of tapering and lift-off, or run the risk of having inflation figures increase further from 6-7% to high single digits.

China Tech Selloff Deepens

Unprecedented regulatory tightening targeting the private economy and lingering risks about forced delisting of Chinese ADRs from US exchanges have resulted in the worst ever correction (-50%) in China Internet/Tech stocks last year, with US1.5tn of market cap lost and raising concerns about the investability of Chinese assets. China’s tech stocks fell once again on Wednesday as firms backed by Tencent Holdings Ltd. came under pressure after it pared investment in the cohort for a second time in two weeks.

Chart Of The Week

Important Information and Disclosure

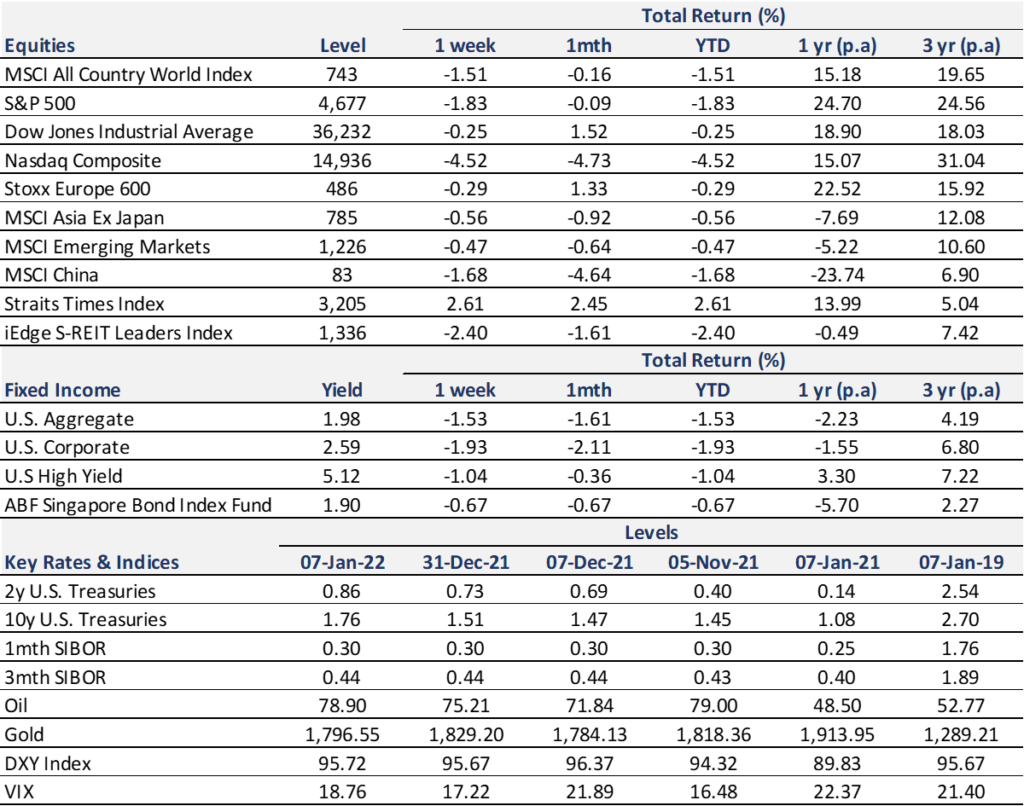

Equity Price Level and Returns: All returns represent the total return for stated period. MSCI ACWI: Global equity index provided by Morgan Stanley Capital International (MSCI). S&P 500: Market capitalization index of U.S stocks provided by Standard & Poor’s (S&P). Dow Jones: Price-weighted index of U.S stocks provided by S&P. NASDAQ: Market capitalization index of U.S stocks provided by NASDAQ. Stoxx 600: Market capitalization index of stocks listed in European region. MSCI Asia Ex Japan: Asia excluding Japan equity index provided by MSCI. MSCI EM: Emerging markets equity index provided by MSCI. SSE: Capitalization weighted index of all A-shares and B-shares listed on Shanghai Stock Exchange. STI: Market capitalization index of stocks listed on Singapore Exchange. SREITLSP: Market capitalization index of the most liquid real estate investment trusts in Singapore.

Fixed Income Yield and Returns: All returns represent total

return for stated period. Global Aggregate: Global investment grade debt from both developed and emerging markets issuers. U.S. Aggregate, U.S Corporate, High Yield provided by Bloomberg Barclays Indices, ICE Data Services & WSJ. SBIF: ABF Singapore bond index fund provided by Nikko AM.

Key Interest Rates: 2-Year U.S Treasuries, 10 Year Treasuries, Bloomberg. 1-month, 3-month SIBOR: Singapore Interbank Offered Rates provided by Association of Banks in Singapore (ABS). Oil (WTI): Global oil benchmark, Bloomberg. Gold: Gold Spot USD/Oz, Bloomberg. DXY Index: U.S. Dollar Index, Bloomberg. VIX: Expectation of volatility based on S&P index options provided by Chicago Board Options Exchange (CBOE).

The information provided herein is intended for general circulation and/or discussion purposes only. It does not account for the specific investment objectives, financial situation or needs of any individual. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

This does not constitute an offer or solicitation to buy/sell any financial instrument or to participate any investment strategy. No representation or warranty whatsoever (without limiting to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (without limiting to any statement, figures, opinion, view or estimate). Syfe does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. Syfe shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly as a result of any person acting on any information provided herein.

The information provided herein may contain projections or other forward-looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future of likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation. Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment. The contents hereof are considered proprietary information and may not be produced or disseminated in whole or in part without Syfe’s written consent.

You must be logged in to post a comment.