The new year is the ideal time to review your personal finances, rebalance your investment portfolios, and strengthen passive income streams. From optimising CPF and SRS contributions to building diversified portfolios, income strategies, and emergency funds, this financial check-up helps you reset your money strategy and start the year on stronger financial footing.

The start of the year is where many people take stock of their finances. You’ve taken a look at your whole-year income, discussed or negotiated for your bonuses, and market movements have revealed which parts of your portfolio are doing the heavy lifting and which aren’t.

Rather than reacting to short-term market noise, a start-of-year review allows you to take a step back and ask a more important question: Is my money structured in a way that supports the life I want in the years ahead?

For Singaporeans, this is also when tax planning, retirement planning, and portfolio optimisation intersect most clearly, making it the most effective time to recalibrate.

Step 1: Re-anchor Your Financial Goals Before Making Changes

Before adjusting any numbers, revisit your goals.

Many investors continue investing out of habit rather than intention. Over the past year, your circumstances may have changed—career progression, higher income, family commitments, or simply a different appetite for risk.

Some questions worth asking:

- Am I investing primarily for long-term growth, passive income, or a balance of both?

- Has my time horizon shortened or lengthened?

- Do I want my portfolio to feel more stable, or am I comfortable with higher volatility?

Your answers will shape everything from asset allocation to product choice. For example, someone focused on long-term wealth accumulation may lean towards globally diversified growth portfolios (such as Syfe’s Core portfolios), while someone prioritising cash flow may tilt more towards income-generating strategies.

Step 2: Clean Up Your Cash Flow and Improve Financial Hygiene

Strong investing outcomes often start with unglamorous basics: expense tracking and cash flow management.

Looking back at your spending over the past 6–12 months can reveal patterns you no longer notice day-to-day. Subscriptions, convenience spending, and lifestyle inflation tend to creep in quietly, especially as income rises.

Instead of aggressive cost-cutting, aim for intentional spending:

- Keep expenses that genuinely improve your quality of life

- Reduce or remove those that don’t

- Redirect the difference automatically into savings or investments

This redirection is crucial. Without it, savings tend to disappear elsewhere. Automating transfers into investment portfolios or savings accounts ensures improvements in cash flow translate into long-term progress.

Step 3: Optimise Your Emergency Fund (Without Letting Cash Sit Idle)

An emergency fund protects your investments more than most people realise. Without one, unexpected expenses may force you to sell assets at the wrong time.

For most Singaporeans, holding three to six months of essential expenses in low-risk, liquid instruments is a sensible benchmark. However, leaving this cash in a low-interest account may no longer be optimal.

Some investors choose flexible cash management solutions like Syfe Cash+ Flexi, which aim to provide liquidity while offering a higher return potential than traditional savings accounts. While emergency funds should always prioritise safety and access, earning a reasonable return on idle cash can improve overall portfolio efficiency.

Step 4: Review and Rebalance Your Investment Portfolio

Portfolios drift over time. Market movements can leave you unintentionally overexposed to certain asset classes or regions. A strong equity rally, for instance, may increase your portfolio’s risk beyond what you originally planned.

Now is a good time to rebalance, bringing your asset allocation back in line with your goals and risk tolerance. This doesn’t require frequent trading or market timing. Instead, it’s about maintaining discipline and diversification.

For investors who prefer a structured, hands-off approach, diversified portfolios like Syfe Core Growth, Core Balanced, and Core Defensive are designed to provide global exposure across equities, bonds, and commodities with automatic rebalancing to keep allocations aligned over time.

Step 5: Build and Strengthen Passive Income Streams

As portfolios grow, many investors start thinking less about pure capital appreciation and more about sustainable passive income.

Income-generating assets can help:

- Smooth portfolio volatility

- Provide regular cash flow

- Reduce the need to sell investments during market downturns

In Singapore, common income sources include dividends, bonds, and REITs. Rather than selecting individual securities, some investors prefer diversified income strategies that spread risk across issuers, sectors, and geographies.

Examples include:

- Income-focused portfolios like Syfe Income+, which aim to generate regular income through a diversified mix of bonds

- REIT-focused strategies such as Syfe REIT+, offering exposure to a basket of global REITs rather than relying on a single property or sector

The objective isn’t to chase the highest yield, but to build a resilient income engine that complements long-term growth assets.

Step 6: Automate Your Investments for Consistency

One of the biggest enemies of long-term investing success is emotion.

Automating investments—such as setting up regular monthly contributions into diversified portfolios—helps remove behavioural biases like fear and greed. It ensures you continue investing during market volatility and benefit from dollar-cost averaging over time.

Whether you’re investing through cash savings or SRS funds, automated portfolios can help maintain discipline while reducing decision fatigue.

Set up recurring investments into Syfe’s managed portfolios, cash management accounts, or brokerage with our auto-invest with eGIRO feature and enjoy a hands-off experience in growing your funds.

Step 7: Review Insurance and Protection Coverage

A holistic financial check-up goes beyond investments. Insurance coverage should evolve as your responsibilities change.

Now is a good time to review whether your health, life, and critical illness coverage remains appropriate, and whether you’re overpaying for policies that no longer fit your needs.

Adequate protection ensures that your long-term financial plan isn’t derailed by unexpected events.

Step 8: Increase Your Income, Not Just Your Savings Rate

While expense management is important, income growth often has a bigger impact on long-term wealth.

As companies start determining budgets and performance reviews, the start of the year is an ideal time to have conversations around salary adjustments, bonuses, or promotions. Even modest income increases, when invested consistently, can significantly accelerate portfolio growth.

Step 9: Position Your Portfolio for the Year Ahead

Looking ahead, many investors are keeping an eye on:

- Equities for long-term growth, with a focus on quality and diversification

- Bonds as both a stabiliser and income source

- REITs for diversified property exposure and income

- Thematic investments tied to long-term structural trends

Rather than making bold predictions, a balanced portfolio that includes growth, income, and defensive elements is often better positioned for a range of outcomes.

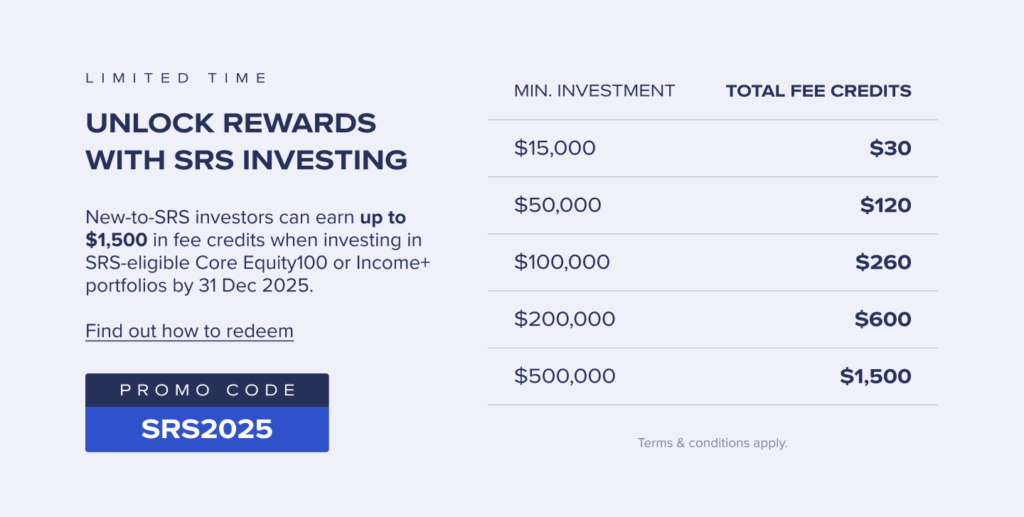

[Bonus] Step 10: Optimise CPF and SRS Contributions at Year-End

In a year-end checklist, be sure to include tax planning.

Voluntary contributions to CPF and SRS can reduce taxable income while strengthening retirement savings. SRS is especially flexible, as funds can be invested in a range of instruments rather than left idle.

Some investors choose to deploy SRS funds into diversified portfolios aligned with their retirement timeline—such as Core portfolios for long-term growth or income-oriented strategies depending on age and risk tolerance.

The key is balance: tax optimisation should support your financial plan, not strain your liquidity.

Start the New Year with a Clearer Financial Plan

A financial check-up isn’t about overhauling everything. It’s about making sure your money is intentional, diversified, and aligned with your goals.

By cleaning up cash flow, optimising CPF and SRS contributions, strengthening passive income through tools like Income+ or REIT+, and maintaining diversified Core portfolios for long-term growth, you set yourself up for a calmer, more confident year ahead.

As you review your finances this year, exploring diversified growth portfolios, income strategies, and flexible cash solutions can help support different parts of your financial plan—whether you’re investing through cash, CPF, or SRS.

Explore Syfe’s offerings today.

Read More:

- Top SRS Investment Options to Grow Your Retirement Savings

- Guide to Supplementary Retirement Scheme (SRS) in Singapore: What It Is and How to Maximise It

- Income Tax Relief: 5 Ways to Lower Your Payable Tax in Singapore

- Passive Income Streams That Work for Singaporeans (and How to Start Earning)

- How to Position Your Investment Portfolio When the US Dollar is Weak

You must be logged in to post a comment.